Press release

Australia Waste Management Market Projected to Reach USD 5.5 Billion by 2034

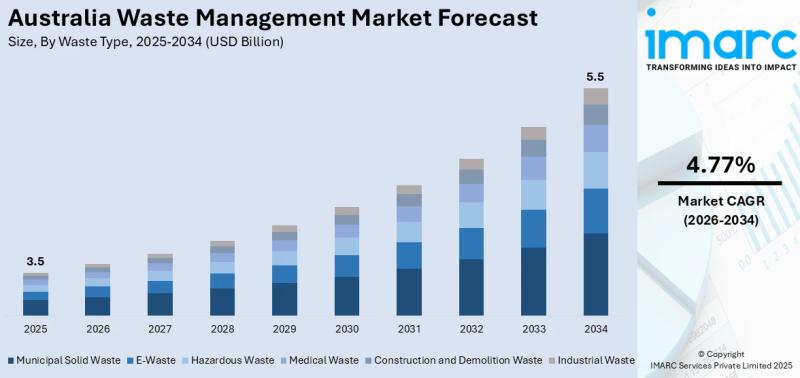

Australia's waste management industry is at a genuine turning point. The market reached USD 3.5 Billion in 2025 and is projected to grow to USD 5.5 Billion by 2034, expanding at a CAGR of 4.77% from 2026 to 2034. Behind that steady growth curve lies a sector undergoing real structural change - moving away from a landfill-heavy, collection-and-dump model toward one built around resource recovery, circular economy principles, and increasingly, energy generation from waste that can't be recycled.

Australia generates waste across every category - municipal solid waste, e-waste, hazardous and medical waste, construction and demolition debris, and industrial refuse - and the pressure to manage all of it more responsibly is coming from multiple directions simultaneously. The country's population reached nearly 27 million by end of 2023, according to the Australian Bureau of Statistics, and continues to grow, pushing up waste volumes across residential, commercial, and industrial sources. Environmental regulations are tightening. Landfill levies are rising across states, making disposal progressively more expensive and alternative approaches more economically attractive. And a growing cohort of businesses, councils, and consumers are actively looking for sustainable waste solutions - not just compliant ones. The market spans collection and disposal services, across industrial, residential, and commercial source segments, across all five major Australian regions.

Read more information about Australia Waste Management Market

https://www.imarcgroup.com/australia-waste-management-market/

Australia Waste Management Market Summary

• Population growth and urbanisation creating sustained volume pressure: With Australia's population growing consistently and urban areas expanding, the volume of residential, commercial, and industrial waste generated keeps rising - straining existing landfill capacity, recycling facilities, and collection infrastructure. Managing concentrated waste volumes in densely populated cities requires increasingly sophisticated systems, and the investment demand this creates is one of the core demand drivers running consistently through the forecast period.

• Kwinana energy recovery facility marks a landmark for waste-to-energy in Australia: On 25 July 2024, Australia's first large-scale energy recovery facility in Kwinana, Western Australia, received its first waste delivery. Once fully operational, the Kwinana facility will convert 460,000 tonnes of residential waste annually into energy - material that would otherwise have ended up in landfills. Veolia has been engaged to run and maintain the facility long-term, making it a major reference point for waste-to-energy investment in Australia. In July 2025, Acciona proposed to acquire the adjacent East Rockingham Waste-to-Energy Project, which would further expand Western Australia's WtE capacity.

• Cleanaway-Tadweer-Parkes Energy Recovery deal targets 700,000 tonnes annually: In January 2026, Tadweer Group signed a Joint Development Agreement with Cleanaway Waste Management and Parkes Energy Recovery Company to build a world-class waste-to-energy facility in Parkes, NSW. The facility is planned to divert 700,000 tonnes of waste annually from landfill and generate 70 megawatts of electricity - a scale that would make it one of the country's largest WtE projects upon completion.

• Circular economy models gaining real commercial traction: Australia's transition toward circular economy principles is moving beyond policy statements into operational practice. In April 2025, Cleanaway and Viva Energy completed a pre-feasibility study for an advanced soft plastics recycling facility - part of a broader effort to transform hard-to-recycle plastics back into feedstock for food-grade plastic resin. Separately, the February 2025 launch of Australia's first large bag recycling plant in Toowoomba - established by Big Bag Recovery and Circular Communities Australia - is expected to divert 4,000 tonnes of woven polypropylene and LDPE bags annually from landfill.

• E-waste recycling evolving from compliance to value recovery: Australia's growing appetite for electronics is generating a corresponding growth in e-waste - materials that contain recoverable gold, copper, and rare earth elements alongside hazardous components that can't go to landfill. In March 2025, UNSW launched its Plastics Filament MICROfactorie in Sydney, recycling hard plastics from electronic waste into 3D printing filament - a practical demonstration of how e-waste can become a resource input rather than a disposal problem.

• Hydrogen-powered waste collection making its debut: In February 2025, Pure Hydrogen delivered Australia's first hydrogen fuel cell rear loader garbage truck to Solo Resource Recovery. The truck, approved under Australian Design Rules, began operations in Adelaide - generating significant interest from local councils exploring hydrogen-powered collection as part of broader fleet decarbonisation efforts. It's a small data point, but it signals that clean energy is beginning to reshape even the most operationally traditional parts of waste management.

• Private sector investment building next-generation infrastructure at pace: In May 2024, Turmec, in collaboration with Rino Recycling, completed a €95 million recycling facility in Pinkenba, Brisbane - one of Australia's most advanced facilities, capable of sorting and processing both wet and dry waste streams under a single roof. This level of private capital commitment demonstrates genuine commercial confidence in the long-term economics of Australian waste infrastructure investment.

• National Waste Policy driving regulatory alignment across jurisdictions: The National Waste Policy's emphasis on waste reduction, increased recycling rates, reduced landfill use, and circular economy principles is creating consistent regulatory direction across state and federal levels. Businesses and municipalities are responding not just by complying, but by getting ahead of requirements - investing in resource recovery and sustainable waste solutions before regulations mandate them.

Request a Business Sample Report for Procurement & Investment Evaluation: https://www.imarcgroup.com/australia-waste-management-market/requestsample

Key Trends Shaping the Australia Waste Management Market

• Waste-to-energy moving from niche to mainstream infrastructure: The Kwinana facility's commencement of operations in 2024 changed the conversation around WtE in Australia from "is it viable here?" to "how do we build more of them?" The Parkes WtE project in NSW and Acciona's interest in East Rockingham confirm that the development pipeline is real and growing. Technologies including incineration, gasification, and anaerobic digestion are all being evaluated and deployed, with different configurations suited to different waste streams and regional contexts. As landfill capacity shrinks and levies rise across states, WtE's dual value proposition - waste diversion plus renewable energy generation - becomes increasingly compelling for councils, private investors, and state governments.

• Smart technology transforming collection and sorting operations: AI-driven sorting systems, sensor-equipped smart bins, and automated collection routing are progressively replacing manual and schedule-based approaches to waste management. Real-time monitoring reduces contamination in recycling streams - one of the persistent problems that has undermined recycling economics in Australia. Smart routing optimises collection runs, cuts fuel consumption, and reduces operational costs. These technologies are becoming standard in new contract specifications for municipal collection services, and they're creating demand for the digital platforms and data infrastructure that underpin them.

• Organic waste processing scaling rapidly across states: Composting facilities and anaerobic digestion plants are being built across Australia in response to both regulatory pressure to divert organic material from landfill and genuine commercial demand for compost and biogas. Methane from organic waste decomposing in landfills is a potent greenhouse gas, and reducing it is a priority under both state and federal environmental frameworks. Businesses and municipalities are increasingly investing in organic waste diversion programs - both to meet sustainability targets and to capture the value that compost and renewable gas represent.

• Market consolidation reshaping competitive dynamics: The Australian waste management sector has experienced significant M&A activity over recent years, most notably through Veolia's global acquisition of Suez and the ACCC-mandated divestitures that followed - resulting in Cleanaway and Remondis both acquiring significant assets and strengthening their competitive positions. This consolidation has created a market anchored by a small number of large, vertically integrated operators with broad geographic coverage and diversified service portfolios, competing alongside a long tail of regional and specialist providers.

• Rural and regional infrastructure emerging as a distinct investment opportunity: Australia's vast geography creates real service gaps in waste management - particularly in regional and remote communities where landfill dependency persists due to a lack of viable alternatives. State government initiatives targeting regional sustainability and waste equity are creating funding channels and partnership opportunities for companies willing to develop decentralised facilities, mobile recycling units, and adapted collection networks for remote areas. For operators able to solve the logistics challenges, this represents a genuinely underserved segment with long-term contracted revenue potential.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/australia-waste-management-market

Market Growth Factors

Population Growth, Urbanisation, and Rising Waste Volumes

The relationship between population growth and waste volumes in Australia is direct and consistent. With the country's population approaching 27 million and continuing to grow through both natural increase and immigration, the quantum of residential, commercial, and industrial waste generated rises every year. Urban expansion creates concentrations of waste that existing landfill and processing infrastructure was not designed to handle at current volumes. Densely populated metropolitan areas - Sydney, Melbourne, Brisbane, Perth - are already experiencing capacity pressures that are making alternative waste management approaches economically necessary rather than merely aspirational. This isn't a temporary pressure; it's a structural demand driver that runs through the entire forecast period and underpins investment decisions in collection capacity, processing facilities, and disposal infrastructure across all five Australian regions. The combination of population growth and rising per-capita consumption in an increasingly urbanised economy means the volume challenge is only going to intensify.

Environmental Regulations, Climate Policy, and the National Waste Policy Framework

Australia's regulatory environment for waste management has tightened materially, and the direction of travel is clear. The National Waste Policy sets explicit targets for waste reduction, recycling rates, and landfill diversion. State-level landfill levies - which vary significantly across jurisdictions but have been trending upward - are progressively making landfill disposal more expensive relative to alternatives, shifting the economics in favour of recycling and resource recovery. Greenhouse gas reduction commitments have made landfill methane - a product of organic waste decomposition - a target for regulatory intervention, driving investment in composting, anaerobic digestion, and organic waste diversion programs. Corporate sustainability commitments and ESG reporting requirements are independently pushing businesses to invest in waste reduction and recycling initiatives, separate from regulatory mandates. For waste management companies, this regulatory environment translates into multi-year contracted revenue streams from councils and businesses investing in compliant and sustainable waste solutions.

Private Sector Investment and Public-Private Partnerships Scaling Infrastructure

The scale of infrastructure required to meaningfully shift Australia's waste management model - from the Kwinana WtE facility to the Pinkenba multi-stream recycling plant to the Parkes energy recovery project - is beyond what public funding alone can finance. Private sector capital, combined with public-private partnership structures, is filling that gap. Companies like Cleanaway, Veolia, and Remondis are actively investing in advanced infrastructure alongside their operational services businesses. International operators are bringing capital, technology, and operational expertise to Australian projects. The Tadweer Group's involvement in the Parkes WtE project alongside Cleanaway is one example of international strategic capital entering the Australian market specifically because of its long-term infrastructure fundamentals. Veolia's contract to operate and maintain the Kwinana facility is another - a long-term, performance-based commercial structure that provides revenue visibility for the operator and operational certainty for the project developer. These models are becoming templates for future investment across the sector.

Market Segmentation

IMARC Group provides analysis of key trends in each segment of the Australia waste management market, along with forecasts at the country level from 2026-2034. The market has been categorized based on waste type, service, and source.

By Waste Type:

• Municipal Solid Waste

• E-Waste

• Hazardous Waste

• Medical Waste

• Construction and Demolition Waste

• Industrial Waste

By Service:

• Collection

• Disposal

By Source:

• Industrial

• Residential

• Commercial

By Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Key Players

The Australia waste management market features a moderately consolidated competitive structure anchored by large, vertically integrated operators with national coverage, competing alongside regional specialists, domestic recyclers, and emerging clean-technology players. Market consolidation has accelerated following Veolia's global acquisition of Suez and the subsequent ACCC-mandated asset divestitures that reshaped competitive positions across putrescible waste, medical waste, and C&I collection.

Key players active in the Australian market include Cleanaway Waste Management (Australia's largest publicly listed waste company, with dominant positions in solid waste collection and growing WtE exposure through the Parkes JDA), Veolia Australia (operating the Kwinana WtE facility and managing long-term municipal and industrial waste contracts), REMONDIS Australia (significantly strengthened through ACCC-mandated Suez asset acquisitions), J.J. Richards & Sons (JJ's Waste & Recycling, a major independent operator with national coverage), SUEZ (continuing as a market presence through remaining Australian operations), Visy Industries (Australia's largest private recycling and packaging company), Bingo Industries, Solo Resource Recovery, Sims Metal Management (Sims Limited), Re.Group, Nationwide Waste Solutions, WM Waste Management Services, Close the Loop, Goterra, Blue Phoenix Australia, Eco Waste Solutions, Waster, Australian Waste Management, and Grasshopper Environmental, among others.

Key Aspects Required for the Australia Waste Management Market

• Landfill levies and capacity constraints are the underlying economic engine of market change: Rising landfill levies across Australian states - combined with physical capacity limits at existing disposal sites - are steadily shifting the economics of waste management. As landfill becomes more expensive, recycling, resource recovery, and WtE become relatively more attractive. This isn't a sudden disruption; it's a gradual, policy-driven repricing of waste disposal that is playing out across the market over the forecast period and systematically improving the economics of alternative approaches.

• Soft plastics remain a major unresolved waste stream requiring new infrastructure: The collapse of the REDcycle soft plastics collection program in 2022 exposed a significant gap in Australia's recycling infrastructure. Cleanaway's pre-feasibility work with Viva Energy on advanced soft plastics processing, combined with the February 2025 opening of Australia's first large bag recycling plant in Toowoomba, reflects the sector's effort to rebuild this capability at industrial scale. Soft plastics represent a large volume of hard-to-recycle waste from households and food manufacturers, and solving it creates both regulatory compliance value and commercial feedstock opportunity.

• E-waste represents a growing and valuable recycling opportunity: As consumer electronics proliferate and product replacement cycles shorten, e-waste volumes in Australia are growing consistently. The material recovery value embedded in e-waste - gold, copper, aluminium, and rare earth elements - creates genuine economics for specialist recycling beyond compliance. UNSW's Plastics Filament MICROfactorie in Sydney, which converts hard plastics from e-waste into 3D printing filament, illustrates how innovative processing approaches can create commercial value from material streams that conventional recycling struggles to handle.

• Construction and demolition waste is a large and largely undertapped recovery opportunity: Construction, renovation, and demolition activity generates substantial volumes of concrete, timber, metal, glass, and mixed materials. With Australia's urban construction pipeline remaining active, C&D waste volumes are sustained at significant levels. Diverting C&D material from landfill through processing, crushing, and reuse in new construction creates both waste diversion value and secondary material supply - an opportunity that is drawing increasing attention from both operators and policymakers as virgin material costs rise.

• Medical and hazardous waste require specialist handling and represent premium-margin segments: Medical waste from hospitals, clinics, and aged care facilities, along with industrial hazardous waste from manufacturing and resources sectors, commands specialised treatment and disposal that significantly exceeds standard collection and disposal margins. The ACCC's careful management of competition in Adelaide's medical waste market during the Veolia-Suez integration - specifically requiring Remondis to acquire Adelaide medical assets to maintain three competing operators - demonstrates how commercially sensitive these specialist segments are.

• Hydrogen and electric vehicles are beginning to reshape collection fleet economics: Pure Hydrogen's delivery of Australia's first hydrogen fuel cell garbage truck to Solo Resource Recovery in February 2025 signals the beginning of fleet decarbonisation across waste collection. As council contracts increasingly incorporate sustainability performance criteria, and as fleet operators face rising diesel costs and emissions reporting obligations, the economic case for clean-energy collection vehicles is strengthening. Electric and hydrogen options are still early in their adoption curve for waste collection specifically, but the direction is established.

• Container Deposit Schemes are expanding consumer recycling engagement significantly: TOMRA Cleanaway recently marked eight years since the launch of Australia's Container Deposit Scheme - a deposit-refund mechanism that has demonstrably improved beverage container recovery rates in states where it operates. The progressive rollout of CDS across remaining jurisdictions is creating growing volumes of clean, sorted recyclable material entering the resource recovery stream - improving economics for downstream processors and demonstrating that well-designed incentive schemes can meaningfully shift consumer recycling behaviour at scale.

• Rural and regional markets need purpose-built solutions, not scaled-down urban models: Waste management in remote and regional Australia operates under fundamentally different economics to urban markets - longer transport distances, lower population density, limited processing infrastructure nearby, and a mix of Aboriginal and Torres Strait Islander community needs that require culturally appropriate approaches. The opportunity here is real, but it requires operators willing to design from first principles for remote contexts rather than adapting urban service models. Government funding programs and community partnerships are the typical path to market for this segment.

Recent News and Developments

January 2026: Tadweer Group signed a Joint Development Agreement with Cleanaway Waste Management and Parkes Energy Recovery Company to build a world-class waste-to-energy facility in Parkes, New South Wales. The project is planned to divert 700,000 tonnes of waste annually from landfill and generate 70 megawatts of electricity - positioning it as one of the largest waste-to-energy developments in Australian history and representing a major vote of confidence from an international strategic investor in Australia's long-term WtE opportunity.

March 2025: UNSW launched Australia's Plastics Filament MICROfactorie in Sydney - a facility that recycles hard plastics recovered from electronic waste into valuable 3D printing filament. Developed as part of UNSW's broader MICROfactorie suite, the project promotes circular economy principles, reduces e-waste landfill volumes, creates skilled jobs, and demonstrates a commercially viable model for turning e-waste streams into manufacturing inputs.

February 2025: Pure Hydrogen delivered Australia's first hydrogen fuel cell rear loader garbage truck to Solo Resource Recovery. The vehicle, compliant with Australian Design Rules, commenced operations in Adelaide and generated immediate interest from local councils exploring hydrogen-powered waste collection as part of their fleet sustainability strategies. The milestone marks the beginning of what could be a significant shift in collection fleet technology over the coming decade.

February 2025: Australia's first large bag recycling plant opened in Toowoomba, Queensland, established through a partnership between Big Bag Recovery and Circular Communities Australia. The facility processes woven polypropylene and low-density polyethylene bags - materials previously sent to landfill for lack of processing options - and is expected to divert 4,000 tonnes of waste annually while generating local employment in regional Queensland.

July 2025: Acciona proposed to acquire the East Rockingham Waste-to-Energy Project in Western Australia - a move that would complement Acciona's existing Kwinana WtE facility and further concentrate advanced waste treatment capability in WA's industrial southwest corridor. The proposal reflects the growing commercial appetite for WtE assets in a state where landfill alternatives are becoming both a regulatory priority and an economic imperative.

April 2025: Cleanaway and Viva Energy completed a pre-feasibility study for an advanced soft plastics recycling facility in Australia - exploring a circular solution that would transform collected soft plastics and other hard-to-recycle materials back into feedstock for food-grade plastic resin. The study represents a concrete step toward rebuilding Australia's soft plastics recycling infrastructure at industrial scale following the REDcycle collapse.

May 2024: Turmec, in collaboration with Rino Recycling, completed the installation of a €95 million advanced recycling facility at Pinkenba, Brisbane. The facility - one of the most sophisticated in Australia - features a state-of-the-art plant capable of sorting and processing both wet and dry waste streams under a single roof, significantly expanding Queensland's material recovery capacity.

April 2024: Cleanaway and Viva Energy announced their agreement to undertake a pre-feasibility assessment of a circular solution for soft plastics and other hard-to-recycle plastics, with the goal of transforming landfill-bound materials back into feedstock for food-grade plastic resin - targeting food manufacturers, packaging specialists, and households seeking sustainable disposal alternatives.

July 2024 (Ongoing Operations): Veolia was engaged to run and maintain Australia's first large-scale waste-to-energy facility at Kwinana, Western Australia, on a long-term performance basis. The facility - which received its first waste delivery in July 2024 - is designed to convert 460,000 tonnes of residential waste annually into electricity, diverting that material entirely from landfill and generating renewable power for the WA grid. Veolia's operational mandate at Kwinana positions it as a central player in Australia's growing WtE sector.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=24682&flag=E

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel. No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers create lasting impact. The company provides a comprehensive suite of market entry and expansion services, including market assessments, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Waste Management Market Projected to Reach USD 5.5 Billion by 2034 here

News-ID: 4482123 • Views: …

More Releases from Imarc

Ethylene Glycol Production Plant DPR - 2026: Investment Cost, Market Growth and …

Setting up an ethylene glycol production plant positions investors in one of the world's most strategically important petrochemical intermediate categories - serving the automotive, textiles, packaging, pharmaceuticals, and industrial chemicals sectors across every major global market. Demand is driven by significant requirements for antifreeze and coolant applications in the automotive industry, robust growth in polyethylene terephthalate (PET) resin production for food and beverage packaging, expanding polyester fiber demand in global…

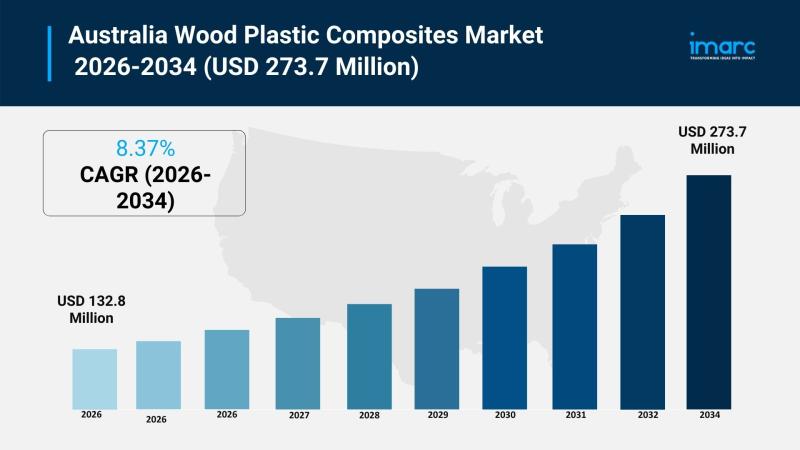

Australia Wood Plastic Composites Market Projected to Reach USD 273.7 Million by …

Market Overview

The Australia wood plastic composites market size was valued at USD 132.8 Million in 2025 and is projected to reach USD 273.7 Million by 2034. The market is expected to grow at a CAGR of 8.37% during the forecast period of 2026-2034. Key growth enablers include rising demand for sustainable building materials and eco-friendly construction practices, prompting builders and consumers to seek durable, low-maintenance, and environmentally responsible alternatives to…

Dimethylamine Production Plant DPR 2026: CapEx/OpEx Analysis with Profitability …

Setting up a dimethylamine production plant positions investors within a strategically important segment of the global chemical manufacturing industry, supported by rising demand across pharmaceuticals, agrochemicals, rubber processing, water treatment, and solvent applications. Dimethylamine serves as a key intermediate in the synthesis of pesticides, solvents, accelerators, and specialty chemicals, making it an essential building block in multiple downstream value chains. As industrial activity expands and demand for crop protection chemicals…

India Washing Machine Industry Insights: Market Share, Competition & Future Fore …

India Washing Machine Market Overview:

According to IMARC Group's report titled "India Washing Machine Market Size, Share, Trends and Forecast by Type, Capacity, Distribution Channel, End Use, and Region, 2026-2034" the report offers a comprehensive analysis of the industry, including market share, growth, trends, and regional insights.

How Big is the India Washing Machine Industry?

The India washing machine market size was valued at USD 1.96 Billion in 2025 and is projected to…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…