Press release

Automotive Camera Market, CAGR of 9.54% during the Forecast Period (2026-2032)

Automotive Camera

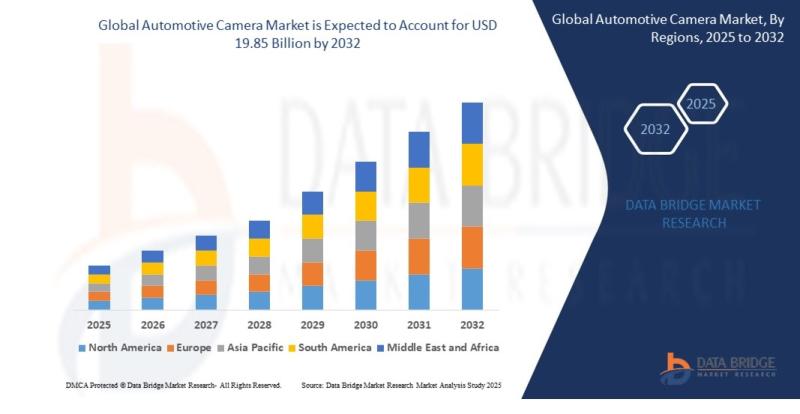

As per Data Bridge Market Research analysis, the Automotive Camera Market was estimated at USD 10.48 billion in 2025. The market is expected to grow from **USD 11.48 billion in 2026 to USD 19.85 billion in 2032, at a CAGR of 9.54% during the forecast period with driven by the rising demand for advanced driver assistance systems (ADAS), increasing vehicle safety regulations, and growing integration of autonomous driving technologies.

The market growth is primarily supported by rapid advancements in imaging technologies, increasing adoption of electric and autonomous vehicles, and stringent safety mandates across developed economies. Additionally, rising consumer preference for enhanced in-vehicle safety features and OEM investments in smart mobility solutions continue to accelerate market expansion globally.

Market Size & Forecast

2025 Market Size: USD 10.48 Billion

2026 Projected Market Size: USD 11.48 Billion

2032 Projected Market Size: USD 19.85 Billion

CAGR (2026-2032): 9.54%

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs):https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-automotive-camera-market

Key Market Report Takeaways

North America holds the largest market share, accounting for approximately 35-38%, driven by early ADAS adoption and strong regulatory frameworks

Asia-Pacific is the fastest-growing region due to rapid automotive production and increasing safety feature penetration

Rear-view and surround-view camera systems dominate the product segment due to mandatory safety regulations

ADAS applications account for the largest share owing to integration in passenger and commercial vehicles

Passenger vehicles remain the leading end-use segment, supported by rising consumer safety awareness and premium feature adoption

Market Trends & Highlights

North America leads the global market due to strong OEM presence, regulatory mandates, and early adoption of ADAS technologies

Asia-Pacific is the fastest-growing region driven by high vehicle production in China, India, and Japan and rising demand for safety features

ADAS remains the dominant application segment, supported by increasing integration of lane departure warning, parking assistance, and collision avoidance systems

Key growth drivers include regulatory mandates, increasing vehicle electrification, and rising consumer demand for enhanced safety and automation

Emerging technologies such as AI-based image processing, thermal imaging cameras, and 360-degree surround view systems are reshaping the market

Increasing partnerships between automotive OEMs and technology providers, along with government safety initiatives, are accelerating innovation and deployment

Details about the report and current availability can be viewed :https://www.databridgemarketresearch.com/reports/global-automotive-camera-market

Market Dynamics

Market Drivers

Rising Adoption of Advanced Driver Assistance Systems (ADAS)

The growing integration of ADAS features such as lane-keeping assist, adaptive cruise control, and automatic emergency braking is a primary driver for automotive cameras. These systems rely heavily on camera-based vision technologies for real-time data processing. Developed regions like North America and Europe have seen widespread adoption due to safety awareness and regulatory mandates. Increasing OEM focus on semi-autonomous capabilities further strengthens demand.

Stringent Vehicle Safety Regulations

Governments across North America and Europe have implemented mandatory regulations requiring rear-view cameras and other safety systems in vehicles. For instance, regulations mandating backup cameras in passenger vehicles have significantly increased camera penetration rates. Emerging economies are also adopting similar safety norms, contributing to global market expansion.

Growth in Electric and Autonomous Vehicles

The rapid growth of electric vehicles (EVs) and autonomous driving technologies is fueling demand for high-performance camera systems. Autonomous vehicles require multiple cameras for perception, navigation, and safety. Asia-Pacific, particularly China, is witnessing strong EV adoption, which directly supports the expansion of automotive camera integration.

Technological Advancements in Imaging and Sensors

Continuous innovation in camera resolution, low-light performance, and AI-based image processing is enhancing system capabilities. Integration with LiDAR and radar systems improves overall vehicle perception accuracy. These advancements are encouraging OEMs to adopt advanced camera solutions, particularly in premium and mid-range vehicle segments.

Increasing Consumer Demand for Safety and Convenience Features

Consumers are increasingly prioritizing safety features such as parking assistance, blind-spot detection, and 360-degree view systems. This shift in consumer preference is driving OEMs to integrate multiple camera systems into vehicles. The trend is particularly strong in urban markets where parking and traffic conditions demand enhanced visibility solutions.

Market Restraints

High Cost of Advanced Camera Systems

The integration of high-resolution cameras, sensors, and AI-enabled processing units significantly increases vehicle costs. This limits adoption in low-cost and entry-level vehicle segments, particularly in price-sensitive markets such as Latin America and parts of Asia. Cost pressures also impact OEM profit margins.

Complex Integration and System Compatibility Issues

Automotive camera systems require seamless integration with other vehicle components such as radar, LiDAR, and onboard computing systems. Compatibility issues and system complexity can lead to increased development time and costs. These challenges are more prominent in legacy vehicle platforms.

Supply Chain Disruptions and Semiconductor Shortages

The automotive camera market heavily depends on semiconductor components and imaging sensors. Global supply chain disruptions and chip shortages have impacted production timelines and increased costs. These challenges have been particularly evident in North America and Europe.

Data Privacy and Cybersecurity Concerns

Camera-based systems collect and process large volumes of visual data, raising concerns regarding data privacy and cybersecurity. Regulatory compliance requirements in regions such as Europe (GDPR) add complexity to deployment. These concerns may slow adoption in certain markets.

Intense Market Competition and Pricing Pressure

The presence of multiple global and regional players has intensified competition, leading to pricing pressures. OEMs often demand cost-effective solutions, forcing suppliers to balance innovation with affordability. This dynamic impacts profitability and limits differentiation.

Market Opportunities

Expansion of Autonomous Driving Technologies

The transition toward higher levels of vehicle autonomy presents significant growth opportunities. Advanced camera systems are essential for perception and decision-making in autonomous vehicles. Increasing investments in autonomous mobility across North America, Europe, and Asia-Pacific are expected to drive demand.

Growing Demand in Emerging Markets

Emerging economies such as India, Brazil, and Southeast Asian countries present untapped growth potential. Rising vehicle ownership, improving infrastructure, and increasing awareness of safety features are supporting market expansion. OEMs are focusing on affordable camera solutions to penetrate these markets.

Integration of AI and Machine Learning

The adoption of AI-powered image recognition and processing technologies is transforming automotive camera capabilities. These technologies enable real-time object detection, driver monitoring, and predictive safety features. Continued innovation in AI presents strong revenue opportunities for market players.

Strategic Partnerships and Collaborations

Collaborations between automotive OEMs, semiconductor companies, and technology providers are accelerating innovation. Partnerships enable the development of integrated solutions combining cameras with advanced analytics. This trend is particularly strong in North America and Europe.

Government Incentives for Vehicle Safety and Electrification

Government initiatives promoting vehicle safety and electric mobility are creating favorable market conditions. Subsidies, tax benefits, and regulatory mandates are encouraging OEMs to integrate advanced safety systems, including cameras. Asia-Pacific is witnessing strong policy-driven growth.

Market Challenges

Operational Complexity in Multi-Camera Systems

Modern vehicles often require multiple cameras for different applications, increasing system complexity. Managing synchronization, calibration, and data processing across multiple cameras presents operational challenges for OEMs and suppliers.

Regulatory Variations Across Regions

Different regions have varying safety and data regulations, making it challenging for manufacturers to standardize products globally. Compliance with diverse regulatory frameworks increases development costs and delays market entry.

Technological Limitations in Adverse Conditions

Camera performance can be affected by environmental conditions such as fog, rain, and low light. Despite advancements, these limitations impact reliability and require additional sensor integration, increasing system costs and complexity.

Supply Chain Dependency on Key Components

The market's reliance on specialized components such as image sensors and semiconductors creates vulnerability to supply disruptions. Geopolitical tensions and trade restrictions further exacerbate these risks, particularly in global supply chains.

Market Fragmentation and Competitive Pressure

The presence of numerous suppliers offering similar products leads to market fragmentation. Intense competition reduces pricing power and forces continuous innovation, increasing R&D expenditure and impacting profitability.

Market Segmentation & Analysis

By Product Type

The market is segmented into rear-view cameras, front-view cameras, side-view cameras, and surround-view systems. Rear-view cameras dominate the segment due to regulatory mandates and widespread adoption in passenger vehicles. Surround-view systems are the fastest-growing segment, driven by increasing demand for 360-degree visibility and enhanced parking assistance. Growth is supported by rising integration in mid- and high-end vehicles.

By Application

Applications include ADAS, parking assistance, and autonomous driving systems. ADAS holds the largest market share due to widespread adoption across vehicle segments. Autonomous driving applications are expected to grow at the highest CAGR, supported by technological advancements and increasing investments in self-driving technologies.

By End-User

The market is segmented into passenger vehicles and commercial vehicles. Passenger vehicles dominate due to higher production volumes and increasing consumer demand for safety features. Commercial vehicles are witnessing steady growth driven by fleet safety regulations and logistics optimization requirements.

By Technology

Technologies include digital cameras, infrared cameras, and thermal imaging systems. Digital cameras account for the largest share due to cost-effectiveness and widespread adoption. Thermal imaging cameras are the fastest-growing segment, particularly in advanced safety and night vision applications.

Analytical Insights

Largest Segment: ADAS applications due to regulatory support and high adoption rates

Fastest-Growing Segment: Autonomous driving applications driven by technological advancements

Dominance is influenced by safety regulations, OEM integration strategies, and increasing demand for intelligent mobility solutions

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America is the largest market, contributing approximately 35-38% of global revenue. The region benefits from advanced automotive technologies, strong regulatory frameworks, and high adoption of ADAS systems. The U.S. leads the market due to the presence of major OEMs and technology providers. High consumer awareness and demand for safety features further support growth.

Europe

Europe represents a mature market with steady growth driven by stringent safety regulations and strong R&D investments. Countries such as Germany, the U.K., and France are key contributors. The region's focus on vehicle safety, environmental standards, and innovation in automotive technologies supports sustained demand.

Asia Pacific

Asia Pacific is the fastest-growing region, driven by rapid industrialization and high vehicle production in China, India, and Japan. Government initiatives promoting vehicle safety and electric mobility are key growth drivers. Increasing middle-class population and rising disposable income further boost demand for advanced automotive features.

Latin America

Latin America is an emerging market with gradual growth supported by improving infrastructure and increasing vehicle adoption. Brazil and Mexico are the primary contributors. However, economic constraints and price sensitivity limit rapid adoption of advanced camera systems.

Middle East & Africa

The Middle East & Africa region shows steady but slower growth. Investments in infrastructure and growing automotive demand support market expansion. However, limited technological adoption and infrastructure challenges restrict rapid growth.

Key Insights:

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Competitive Landscape

Market Structure Overview

The automotive camera market is moderately consolidated, with a mix of global leaders and regional players. Competition is driven by technological innovation, product differentiation, and strategic partnerships. Leading companies focus on advanced imaging solutions and integrated safety systems. Competitive analysis provides insights into market positioning and strategic direction.

Key Industry Players

Major players operate globally with strong product portfolios and technological capabilities. These companies focus on innovation, geographic expansion, and partnerships to strengthen their market position.

List of Key Industry Players:

Robert Bosch GmbH

Continental AG

Magna International Inc.

Valeo SA

Denso Corporation

Aptiv PLC

OmniVision Technologies

Sony Semiconductor Solutions

ZF Friedrichshafen AG

Competitive Strategies

Companies are focusing on product innovation, including AI-enabled camera systems and high-resolution imaging solutions. Strategic partnerships with OEMs and technology providers are common. Mergers and acquisitions help expand capabilities and market reach. Geographic expansion and supply chain optimization are also key strategies.

Emerging Players & Market Dynamics

Startups and niche players are introducing cost-effective and specialized solutions, increasing market competition. These companies focus on innovation in AI, imaging, and sensor fusion technologies. Rising investment and digital transformation trends are reshaping the competitive landscape.

Latest Developments

January 2025 - Bosch: Launched next-generation AI-enabled automotive camera systems to enhance ADAS capabilities, strengthening its leadership in intelligent mobility solutions.

October 2024 - Continental AG: Introduced high-resolution surround-view camera technology for autonomous vehicles, improving real-time perception and safety performance.

July 2024 - Magna International: Partnered with a leading EV manufacturer to develop integrated camera-based driver assistance systems, expanding its footprint in the EV segment.

March 2024 - Valeo SA: Announced investment in thermal imaging camera technology to enhance night vision systems, supporting innovation in advanced safety solutions.

December 2023 - Denso Corporation: Expanded production capacity for automotive sensors and cameras in Asia-Pacific, addressing rising regional demand and supply chain resilience.

September 2023 - Sony Semiconductor Solutions: Developed advanced CMOS image sensors for automotive applications, improving image clarity and low-light performance.

June 2023 - ZF Friedrichshafen AG: Collaborated with a global OEM to integrate multi-camera systems into next-generation autonomous platforms, accelerating technology deployment.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/global-automotive-brake-valve-market

https://www.databridgemarketresearch.com/reports/global-automotive-interior-market

https://www.databridgemarketresearch.com/reports/global-automotive-on-board-ac-dc-power-inverters-market

https://www.databridgemarketresearch.com/reports/global-automotive-polyurea-greases-market

https://www.databridgemarketresearch.com/reports/global-automotive-supercharger-market

https://www.databridgemarketresearch.com/reports/global-automotive-terminal-market

https://www.databridgemarketresearch.com/reports/global-automotive-transmission-engineering-services-outsourcing-market

https://www.databridgemarketresearch.com/reports/global-automotive-valve-stem-seal-market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC: +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

Data Bridge Market Research follow a wide array of models that allow proactive collaboration with clients, categorize new sources of incremental revenues, deliver revenue planning, and first-mover advantage about innovations and disruptions through early market research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Automotive Camera Market, CAGR of 9.54% during the Forecast Period (2026-2032) here

News-ID: 4473724 • Views: …

More Releases from Data Bridge Market Research

Biosimilar Market Set for Exponential Surge at 32.00% CAGR, Projected to Reach U …

As per Data Bridge Market Research analysis, the Biosimilar Market was estimated at USD 85.71 billion in 2025. The market is expected to grow from USD 113.14 billion in 2026 to USD 598.55 billion in 2032, at a CAGR of 32.00% during the forecast period, driven by the rising demand for cost-effective biologic therapies, increasing patent expirations of blockbuster biologics, expanding regulatory support, and growing investments in biopharmaceutical innovation.

Get the…

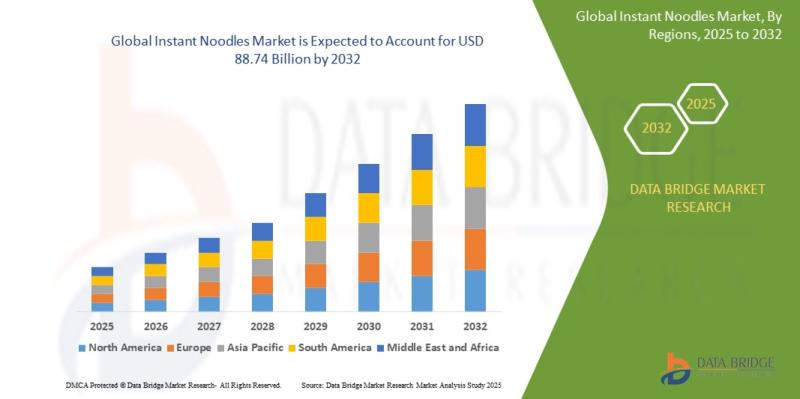

Instant Noodles Market to Hit USD 88.74 Billion by 2032 as Ready-to-Eat Food Con …

As per Data Bridge Market Research analysis, the Instant Noodles Market was estimated at USD 61.40 billion in 2025. The market is expected to grow from USD 64.72 billion in 2026 to USD 88.74 billion in 2032, at a CAGR of 5.40% during the forecast period, driven by the rising demand for convenient and affordable ready-to-eat food products, increasing urbanization, and evolving consumer lifestyles.

Get the full PDF sample copy of…

Kimchi Market Growth Analysis (2025-2032): Expanding at a CAGR of 5.5% Toward US …

Market Summary

As per Data Bridge Market Research analysis, the Market was estimated at USD 524.92 billion in 2025. The market is expected to grow from USD 553.79 billion in 2026 to USD 763.59 billion in 2032, at a CAGR of 5.5% during the forecast period with driven by the rising demand for advanced technologies, increasing global consumption patterns, and expanding investments across key industries.

Get the full PDF sample copy of…

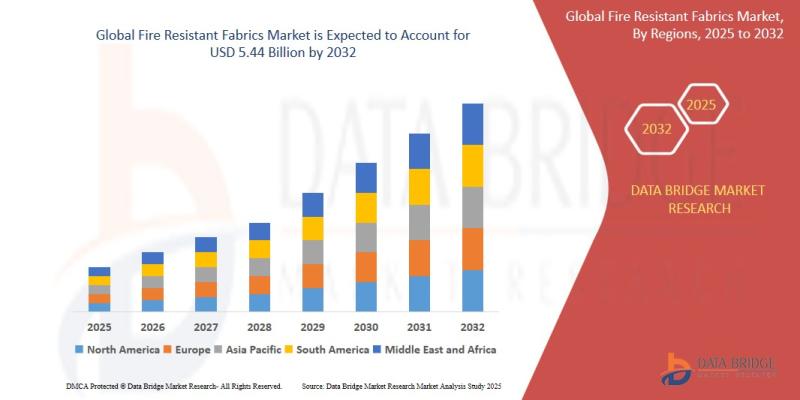

Fire Resistant Fabrics Market Forecast: Reaching USD 5.44 Billion by 2032

Fire resistant fabrics are engineered textiles designed to withstand high temperatures and prevent fire propagation, making them essential in protective clothing and industrial applications. The market is experiencing steady growth due to rising occupational safety awareness, regulatory enforcement, and advancements in fabric technologies such as inherently flame-resistant fibers and treated fabrics. Increasing industrialization in emerging economies and growing investments in worker safety solutions are further supporting market expansion.

Market Size &…

More Releases for OEM

OEM Partnership Guide: Working with a Touch-free Automatic Kitchen Garbage Can O …

With increasing global demand for smart home solutions, Sinoware International Ltd, a top provider in household products industry, is pleased to unveil expanded OEM partnership initiatives.

Sinoware has established itself in Jiangmen--China's premier stainless steel industry zone--as an indispensable touch-free automatic kitchen garbage can OEM manufacturer for global brands seeking to incorporate high-tech sanitation solutions into their portfolios.

By combining their decades-old tradition of metal craftsmanship with cutting-edge infrared and…

Revolutionizing OEM Coatings With Sustainable Solutions Trend: A Crucial Influen …

Which drivers are expected to have the greatest impact on the over the oem coatings market's growth?

The surge in requirements from final consumer industries is forecasted to boost the expansion of the OEM coatings market. These coatings, referred to as OEM, are utilized during the integration of other firms' products into the substrate process or application. They prove to be beneficial for a variety of end-user sectors, including automotive and…

OEM Technology Partnerships Launches Brokerage Specializing in 100+ OEM Technolo …

San Francisco, California, USA - February 13, 2025 - OEM Technology Partnerships is thrilled to announce the launch of its specialized brokerage focused on connecting businesses with a comprehensive portfolio of over 100 Original Equipment Manufacturer (OEM) technologies. This new venture is poised to revolutionize how companies access and implement cutting-edge solutions across diverse industries.

Leveraging deep industry expertise and a vast network of OEM partners, OEM Technology Partnerships offers a…

OEM or ODM Watches? What's the Difference?

When searching for a watch manufacturer for your store or watch brand, you may come across the terms OEM and ODM. But do you truly understand the difference between them? In this article, we will delve into the distinctions between OEM and ODM watches to help you better grasp and choose the manufacturing service that suits your needs.

Image: https://www.naviforce.com/uploads/15a6ba3911.png

What's OEM / ODM Watches [https://www.naviforce.com/products/]

OEM (Original Equipment Manufacturer) watches are produced…

OEM Partnership with Extreme Networks

ComputerVault announces an OEM partnership with Extreme Networks and has certified its switches for use with ComputerVault enterprise software to deliver virtual desktop infrastructure (VDI).

Extreme Networks industry leading switches deliver ComputerVault Virtual Desktops at faster than PC speeds in the LAN and WAN.

“ComputerVault is very excited to work with Extreme Networks. Not only are their switches very reliable, but their exceptional performance guarantees a great user experience”, said Marc…

Humidity Measurement Module for OEM Applications

The EE1900 humidity module from E+E Elektronik is optimised for the measurement of relative humidity (RH) or dew point temperature (Td) in climate and test chambers. With outstanding temperature compensation across the working range from -70 °C to 180 °C (-94 °F to 356 °F) and the choice of stainless steel and plastic probes, the module is suitable for a wide range of applications.

High Accuracy in Harsh Environment

The excellent…