Press release

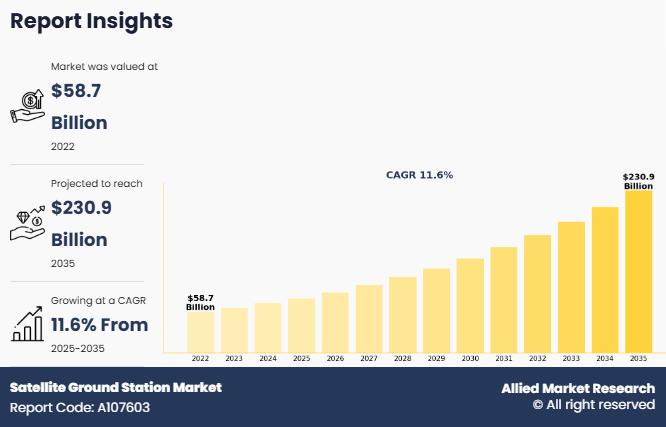

Satellite Ground Station Market to Reach $230.9 Billion by 2035 : Sustained Growth with a 11.6% CAGR

Satellite Ground Station Market

A satellite ground station is a terrestrial facility equipped with antennas, radio-frequency transmitters and receivers, tracking systems, and control software that enables two-way communication with orbiting satellites such as those operated by ISRO. It functions as the primary interface between space-based assets and users on Earth by transmitting command and control signals to manage satellite operations (telemetry, tracking, and command), receiving payload data such as imagery or communication traffic, processing and routing this information to end users, and supporting mission planning, health monitoring, and orbit management, thereby ensuring reliable satellite operations across applications including telecommunications, navigation, Earth observation, weather monitoring, and scientific research.

Download Sample Pages - https://www.alliedmarketresearch.com/request-sample/A107603

The satellite ground station market trends include strong growth driven by the rapid deployment of LEO and multi-orbit satellite constellations, rising demand for high-throughput data connectivity, and the increasing adoption of cloud-based, software-defined architectures and Ground Station-as-a-Service (GSaaS) models that enable scalable, automated, and real-time data processing capabilities. Rise in demand for satellite-based communication services drives satellite ground station market growth, as the rapid expansion of broadband connectivity, mobile backhaul, maritime and aviation communications, and remote-area coverage increases the need for reliable ground infrastructure to manage satellite links. The rollout of large LEO constellations by operators such as SpaceX through its Starlink network and Amazon's Project Kuiper is significantly increasing the volume of satellite traffic, that requires geographically distributed and automated ground stations for telemetry, tracking, command (TT&C), data downlink, and network control. In parallel, rise in adoption of satellite communications by enterprises, government agencies, and defense organizations for secure connectivity, disaster response, and mission-critical operations is boosting investments in advanced ground station networks with higher throughput, low latency, and cloud-integrated architectures and drive the satellite ground station market size.

High capital investment and infrastructure costs significantly hamper the satellite ground station market growth, as establishing and operating ground stations requires substantial upfront spending on land acquisition, antenna systems, RF equipment, control software, secure data links, and ongoing maintenance. The need for geographically distributed stations to ensure continuous satellite visibility further increases costs related to site selection, regulatory approvals, power supply, and network integration. Smaller operators and emerging space startups often struggle to justify these investments, especially when competing with large-scale networks operated by players such as SpaceX and Amazon, which benefit from economies of scale and in-house infrastructure. In addition, high operational expenses for skilled personnel, spectrum licensing, cybersecurity, and system upgrades create financial barriers to entry, slowing new deployments and limiting market expansion, particularly in developing regions.

The growing deployment of low earth orbit (LEO) satellite constellations is creating satellite ground station market opportunities, as LEO networks require a much denser and more geographically distributed ground infrastructure compared to traditional GEO and MEO systems. The high orbital velocity and shorter visibility windows of LEO satellites increase the frequency of handovers and data downlink sessions, driving demand for a larger number of automated, multi-mission ground stations capable of seamless telemetry, tracking, and command (TT&C) as well as high-throughput data reception. This is accelerating investments in scalable ground station networks, virtualized control systems, and cloud-integrated architectures to efficiently manage the surge in satellite traffic.

LIMITED-TIME OFFER - Buy Now & Get Exclusive Discount on this Report @ https://www.alliedmarketresearch.com/checkout-final/22a41e2018870fc6b2293ee7318d8693

In addition, large-scale LEO programs led by operators such as SpaceX (Starlink) and Amazon (Project Kuiper) are encouraging partnerships with commercial ground station service providers to expand global coverage quickly without building all infrastructure in-house. This trend is opening new revenue streams for ground station-as-a-service models, shared infrastructure platforms, and edge data processing solutions. Moreover, the proliferation of small satellites and CubeSats within LEO constellations is fostering demand for cost-effective, modular, and software-defined ground stations, creating opportunities for technology providers to innovate in antenna design, automation, AI-driven scheduling, and network optimization.

The satellite ground station market segmentation include segmnets such as platform, function, orbit, end user, and region. On the basis of platform, it is divided into fixed, portable, and mobile. On the basis of function, it is classified into communication, earth observation, space research, navigation, and others. On the basis of orbit, it is categorized into LEO, MEO, and GEO. On the basis of end user, it is fragmented into commercial, government, and defense.

On the basis of platform, it is segmented into fixed, portable, mobile. The fixed segment dominated the market share in 2024. This is attributed to its critical role in supporting high-capacity, mission-critical satellite operations across communication, defense, earth observation, and space research applications. Fixed ground stations are typically equipped with large, high-gain antennas and advanced RF systems, enabling reliable and continuous connectivity with satellites in LEO, MEO, and GEO orbits. These installations are designed for long-term operations, offering superior performance, higher bandwidth capabilities, and enhanced signal stability compared to mobile or transportable ground stations.

However, the mobile segment is anticipated to grow at the fastest CAGR in the satellite ground station market driven by rise in demand for connectivity on the move across defense, maritime, aviation, and land mobility applications. Increase in deployment of LEO and multi-orbit constellations is enabling low-latency, high-throughput communications that support in-flight connectivity, connected naval fleets, unmanned systems, disaster response vehicles, and tactical military platforms.

For Purchase Enquiry: https://www.alliedmarketresearch.com/purchase-enquiry/A107603

On the basis of function, it is classified into communication, earth observation, space research, navigation, and others. The communication segment dominated the market in 2024, primarily driven by the surge in global data consumption, expansion of broadband connectivity, and the rapid deployment of high-throughput satellites and LEO constellations. Increasing satellite ground station market demand such as DTH broadcasting, enterprise VSAT networks, in-flight and maritime connectivity, and rural broadband significantly boost the need for advanced ground station infrastructure. The rise in investments by satellite operators and service providers, including companies such as SpaceX and OneWeb, further fosters the growth of the communication segment by expanding global gateway networks and enhancing real-time data transmission capabilities.

However, the navigation segment is anticipated to grow at the fastest CAGR during satellite ground station market analysis. This growth is primarily driven by the expanding reliance on global navigation satellite systems (GNSS) for precision timing, autonomous mobility, aviation management, maritime navigation, defense operations, and critical infrastructure synchronization.

On the basis of orbit, it is classified into LEO, MEO, and GEO. The LEO segment dominated the market in 2024. driven by the rapid deployment of large-scale low Earth orbit constellations aimed at delivering high-speed, low-latency connectivity worldwide. The surge in demand for broadband internet, real-time data services, IoT connectivity, and defense communications significantly increased the need for advanced ground station networks capable of tracking and communicating with a high volume of fast-moving LEO satellites.

However, the GEO segment is anticipated to grow at the fastest CAGR in the satellite ground station market. This is attributed to sustained demand for high-capacity broadcasting, broadband backhaul, enterprise VSAT networks, and secure government communications. Geostationary satellites remain critical for wide-area coverage and uninterrupted service, particularly in remote and underserved regions, making them indispensable for national connectivity strategies and defense communication architectures.

Connect to Analyst: https://www.alliedmarketresearch.com/connect-to-analyst/A107603

On the basis of end user, it is classified into commercial, government, and defense. The commercial segment dominated the market in 2024 driven by the rapid expansion of private satellite operators, telecom providers, broadcasting companies, and space-tech startups investing heavily in satellite communication and data services. The increase in deployment of LEO constellations by companies such as SpaceX and OneWeb significantly boosts the demand for commercial ground station infrastructure to support broadband connectivity, enterprise networks, IoT applications, and media broadcasting.

However, the defense segment is anticipated to grow at the fastest CAGR in the satellite ground station market. This is due to rise in geopolitical tensions, modernization of military communication networks, and increasing investments in secure and resilient space-based infrastructure. Armed forces globally are prioritizing protected SATCOM, anti-jam capabilities, and multi-orbit interoperability to ensure uninterrupted command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) operations.

Region wise, North America was the largest shareholder in the satellite ground station market in 2024, supported by strong investments in space infrastructure, the presence of leading satellite operators, and advanced technological capabilities. The region benefits from a well-established ecosystem led by organizations such as NASA and private space companies such as SpaceX, which continuously expand satellite constellations and require extensive ground station networks for mission control, data processing, and communication.

However, the Asia-Pacific region is anticipated to grow at the fastest CAGR in the satellite ground station market. This growth is driven by increase in government investments in space programs across countries such as India, China, and Japan, along with the rise in participation of private space companies. Expanding satellite launches for communication, earth observation, and navigation services are creating strong demand for new ground infrastructure. Additionally, the rapid growth of broadband connectivity, defense modernization programs, and increasing adoption of satellite-based services in remote and rural areas are further accelerating market expansion across the region.

Key players in the satellite ground station market include Kratos Defense & Security Solutions, Inc, Comtech Telecommunications Corp, Viasat, Inc, SES S.A. EchoStar Corporation, GILAT SATELLITE NETWORKS, General Dynamics Corporation, Kongsberg Gruppen AS, ST Engineering, Communications & Power Industries LLC.

Key Findings of the Study

On the basis of platform, the fixed segment dominated the satellite ground station market share in 2024. However, mobile segment is anticipated to grow at the fastest CAGR during the forecast period.

On the basis of function, the communication segment dominated the satellite ground station industry in 2024. However, navigation segment is anticipated to grow at the fastest CAGR during the forecast period.

On the basis of orbit, the LEO segment dominated the satellite ground station industryin 2024. However GEO segment is anticipated to grow at the fastest CAGR during the forecast period.

On the basis of end user, the commercial segment dominated the market in 2024. However, defense segment anticipated to grow at the fastest CAGR during the forecast period.

The North America region accounted for the largest satellite ground station market share in 2024. However, Asia-Pacificis anticipated to grow at the fastest CAGR during the forecast period.

Access Full Summary: https://www.alliedmarketresearch.com/satellite-ground-station-market-A107603

David Correa

1209 Orange Street

Corporation Trust Center

Wilmington

New Castle

Delaware 19801

USA Int'l: +1-503-894-6022

Toll Free: +1-800-792-5285

Fax: +1-800-792-5285

help@alliedmarketresearch.com

Allied Market Research (AMR) is a full-service market research and business-consulting wing of Allied Analytics LLP based in Portland, Oregon. Allied Market Research provides global enterprises as well as medium and small businesses with unmatched quality of "Market Research Reports Insights" and "Business Intelligence Solutions." AMR has a targeted view to provide business insights and consulting to assist its clients to make strategic business decisions and achieve sustainable growth in their respective market domain.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Satellite Ground Station Market to Reach $230.9 Billion by 2035 : Sustained Growth with a 11.6% CAGR here

News-ID: 4472712 • Views: …

More Releases from Allied Market Research

Custom Shoes - Industry Analysis & Investment Outlook

This analysis focuses on the potential for investment in the global Custom Shoes Segment, due to a lack of offerings from traditional shoe manufacturers and soulless sneaker factory-stores; return rates soar with consumers today high street and online shopping like never before: It's primarily fueled by rapid consumer adoption, thanks to AI-fueled processes (including production on-demand), coupled with 3D printing. This is being spurred alongside floating VR/AR technology where we…

Fantasy Sports - Industry Analysis & Investment Outlook

A new industry analysis shows that the growing global Fantasy Sports market is expected to receive significant investment due to factors as diverse as the deepening penetration of smartphones and broadband, increased interest from younger demographics, sports betting legalization in major jurisdictions, unique vs. traditional formats for gaming engagement and AI/real time analytics - all redefining how platforms, investors and other key players interact with sports fans around the world:

The…

Electric Hair Brush Market 2026 | Industry Thriving Worldwide at a Significant G …

The latest strategic study by Allied Market Research on the Electric Hair Brush Market provides an in-depth analysis of emerging beauty appliance trends, growth drivers, consumer behavior, market restraints, and the competitive landscape shaping this fast-evolving industry. The report delivers detailed insights into market size, revenue performance, CAGR projections, distribution trends and future investment opportunities by using validated methodologies and industry-backed intelligence. .

➤ Request for a Sample Now https://www.alliedmarketresearch.com/request-sample/A06111

➤…

Mold Inhibitors Market Projected to Reach US$ 2.4 Billion by 2032

A recent report published by Allied Market Research, titled "Mold Inhibitor Market by Nature (Natural, Synthetic), by Type (Propionates, Sorbates, Benzoates, Parabens, Others), by Application (Food & Beverage, Animal Feed, Pharmaceuticals Cosmetics and Personal Care: Global Opportunity Analysis and Industry Forecast 2023-2032," provides a detailed overview of the global and regional dynamics influencing this fast-paced industry. The report provides an overview of the competitive landscape, key market segments and trends…

More Releases for LEO

"LEO Satellites: Revolutionizing Space Communication and Observation"

The LEO Satellite Market is expected to register a CAGR of 11.5% from 2025 to 2031, with a market size expanding from US$ XX million in 2024 to US$ XX Million by 2031.

Growing Demand for Global Connectivity: The increasing need for ubiquitous, high-speed internet access, particularly in remote and underserved regions, is a key driver for the LEO satellite market. LEO satellites, with their low latency and ability to provide…

LEO Antenna Market Size 2024 to 2031.

Market Overview and Report Coverage

A LEO antenna is a low earth orbit satellite antenna designed to communicate with satellites that operate in low earth orbit. These antennas are essential for various applications such as communication, navigation, and earth observation.

The LEO antenna market is expected to witness significant growth in the coming years, with a projected CAGR of 10.70% during the forecasted period. The increasing demand for satellite communication…

LEO Satellite Antenna Manufacturers in Korea | GTL

GTL is the best LEO satellite antenna manufacturers in Korea, with unique technology that allows an antenna to automatically track satellite signals.

The industry's accelerating rate of LEO launches is based on the low costs of developing and launching LEO satellites. And ground infrastructure is essential for the new generation of LEO satellite constellations. As such, GTL provides a cutting-edge infrastructure to support the expanding space industry.

GTL LEO satellite

A LEO satellite…

LEO Satellite Antenna Products | GTL

GTL provides LEO satellite antenna to enable the real-time and online checking of antenna status in a low-cost maintenance in Korea.

The industry's accelerating rate of LEO launches is based on the low costs of developing and launching LEO satellites. And ground infrastructure is essential for the new generation of LEO satellite constellations. As such, GTL provides a cutting-edge infrastructure to support the expanding space industry.

GTL LEO satellite Satellites need to…

LEO Satellite Market Size - Forecasts to 2027

According to a new market research report published by Global Market Estimates, the Global LEO Satellite Market is projected to grow from USD 9.8 Billion in 2022 to USD 20.1 billion in 2027 at a CAGR value of 15.8% from 2022 to 2027.

Browse 151 Market Data Tables and 111 Figures spread through 181 Pages and in-depth TOC on "Global LEO Satellite Market - Forecast to 2027" https://www.globalmarketestimates.com/market-report/leo-satellite-market-3743

By Satellite Type…

Leo Pharma - Cancer Drugs Clinical Pipeline Insight

“Leo Pharma - Cancer Drugs Clinical Pipeline Insight” offers in depth insight on ongoing clinical trials for the cancer drugs developed by Leo Pharma. This report highlights various clinical and non-clinical parameters involved in the development of cancer drugs in clinical pipeline. Currently there are “3” cancer drugs in clinical pipeline.

The report includes all the relevant information with respect to development of cancer drugs in the clinical pipeline. Report helps…