Press release

Battery Grade Lithium Compounds Market to Add US$34.85 Billion by 2033 as Carbonate, Hydroxide and Specialty Lithium Chemistries Move to the Core of Battery Supply Chains

Battery Grade Lithium Compounds Market

That scale of growth is not happening in isolation. The International Energy Agency says battery demand for the energy sector reached the 1 TWh milestone in 2024, electric-vehicle battery demand rose to more than 950 GWh, and global battery manufacturing capacity reached 3 TWh in 2024, with potential to triple again within five years if announced projects materialize. At the same time, lithium prices have fallen by more than 85% from their 2022 peak, changing the competitive equation from simple scarcity toward conversion efficiency, cost control, product qualification and geographic diversification.

Download Exclusive Sample Report: https://www.datamintelligence.com/download-sample/battery-grade-lithium-compounds-market?kailas

Battery-grade lithium compounds are no longer just upstream chemicals tied to mining cycles. They are becoming a strategic layer in battery performance, cathode qualification, electrolyte design, supply-chain localization, ESG positioning and capital allocation. The companies now shaping the market are not only expanding lithium output. They are building customer-certified carbonate and hydroxide flows, improving emissions intensity, commercializing specialty compounds, scaling recycling and investing in technology platforms that move them closer to the battery cell itself.

1. Why this market now carries strategic weight

The most important change in this market is where value is being captured. In earlier cycles, investors and industrial buyers focused heavily on resource ownership. That still matters, but current company disclosures show that the premium is shifting toward battery-ready conversion. Producers that can reliably deliver qualified lithium carbonate, lithium hydroxide and specialty compounds into cathode, electrolyte and next-generation battery programs are now in a stronger position than those relying on resource narratives alone. SQM's first shipment of lithium hydroxide from Australia, Tianqi's customer-certified Kwinana output, Albemarle's portfolio rebalancing and Rio Tinto's project financing all point in that direction.

A second shift is the growing technical breadth of the category. The market does not stop at lithium carbonate and lithium hydroxide. Specialty compounds such as lithium chloride, bromide, iodide, oxide, metal and emerging electrolyte-related products are becoming more relevant as solid-state programs, lithium metal anodes and advanced inorganic materials move from laboratory work toward pilot and early commercialization. Ganfeng's disclosures around lithium sulfide, solid electrolytes and lithium metal-linked battery pathways show why this wider compounds basket deserves attention from technology and strategy teams, not only procurement functions.

2. Market segmentation

2.1 By type

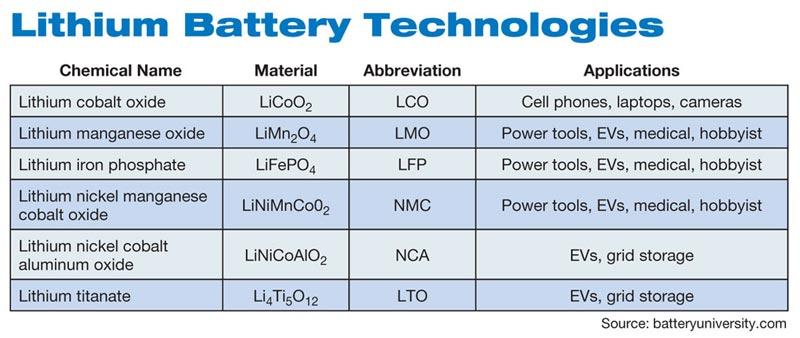

The market is segmented into Lithium Carbonate, Lithium Hydroxide, Lithium Concentrate, Lithium Metal, Butyl Lithium, Lithium Chloride, Lithium Bromide, Lithium Iodide, Lithium Oxide, Others Nitride and Others.

Commercially, lithium carbonate and lithium hydroxide remain the center of gravity because they sit directly inside today's battery manufacturing and cathode conversion chains. Recent official disclosures from SQM, Tianqi, Albemarle and Rio Tinto's lithium projects are overwhelmingly concentrated on those two molecules, which is a strong indication of where scale demand currently resides. At the same time, lithium metal and specialty inorganic compounds are gaining strategic relevance through next-generation batteries, electrolyte systems and advanced materials programs.

2.2 By battery technology

The market is segmented by Cathode Material, Anode Material and Electrolyte.

Cathode-material demand remains the clearest commercial driver today because battery-grade lithium carbonate and hydroxide feed directly into mainstream battery chemistries. However, the market is broadening. Ganfeng has disclosed battery-grade lithium sulfide mass production and multiple solid electrolyte materials, while also advancing lithium metal-related battery development with energy density potential above 500 Wh/kg. That means anode and electrolyte-linked compounds are becoming more relevant to future value creation, even if cathode-related demand still leads current volume.

2.3 By application

The market is segmented into Li-ion Batteries, Cement & Concrete, Metallurgy, Lubricants, Glass & Ceramics, Polymers, Specialty Inorganics, Medicines and Others.

Despite the broad application list, Li-ion batteries remain the core strategic growth engine. The IEA's battery-demand data and the current capital programs of lithium producers both make that clear. Non-battery applications continue to provide diversification and baseline demand, but the scale-up in battery-grade lithium compounds is being set primarily by mobility and stationary storage economics rather than traditional industrial uses.

2.4 By end-user

The market spans Aerospace and Defense, Automotive, Oil and Gas, Energy, Building, Chemical Processing and Others.

Among these, automotive and energy are the most strategically important growth anchors because they map directly to EV batteries and stationary storage systems. Aerospace and defense, chemical processing and specialty industrial uses remain important qualified niches, particularly where purity, safety and advanced electrochemistry matter. The broader point is that end-user demand is becoming more diversified, but it is still being repriced by battery-led infrastructure spending.

3. Recent developments shaping the market

3.1 Albemarle idled part of Kemerton to protect economics

On February 11, 2026, Albemarle announced that it would idle the remaining operating train at its Kemerton lithium hydroxide conversion plant in Western Australia. The company said the decision would improve financial flexibility and preserve optionality, while having no impact on projected 2026 sales volumes. This is a clear example of producers prioritizing margin quality and disciplined deployment over headline conversion capacity.

3.2 Albemarle advanced Kings Mountain as a U.S. supply-chain option

On March 12, 2026, Albemarle completed dewatering of the Kings Mountain open pit in North Carolina, a key milestone for one of North America's largest hard-rock lithium deposits. The company said the site has the potential to produce and process nearly 3.1 million tons of lithium-bearing spodumene ore annually and that more than 1.57 billion gallons of water were safely treated and discharged during the dewatering program.

3.3 Rio Tinto secured major project financing for Rincon

On March 11, 2026, Rio Tinto announced a US$1.175 billion financing package for the Rincon lithium project in Argentina from IFC, IDB Invest, Export Finance Australia and JBIC. The project is being developed as a US$2.5 billion investment targeting about 60,000 tonnes per year of battery-grade lithium carbonate capacity, with first production expected in 2028.

3.4 Rio Tinto took direct control of Nemaska Lithium

On February 18, 2026, Rio Tinto said it had increased its ownership in Nemaska Lithium to 53.9% and would assume direct management of the business. The company also said the Bécancour lithium hydroxide plant was 60% complete at the end of 2025, Quebec would invest up to US$200 million, and Rio Tinto planned to invest more than US$300 million in 2026.

3.5 SQM reported stronger demand signals and lower-footprint hydroxide output

In its fourth-quarter 2025 results released in early 2026, SQM said it saw early signs of a better lithium supply-demand balance beginning in November 2025, estimated the lithium market could grow around 25% in 2026, and said it was operating at full capacity. The company also noted that in January 2026 it celebrated the first shipment of lithium hydroxide produced in Australia at the Kwinana refinery, with certification under the International Lithium Association LCA methodology showing a 37% lower emissions footprint than traditional hard-rock production refined in China.

3.6 Tianqi moved on market infrastructure and recycling

On January 24, 2026, Tianqi said its branded lithium carbonate had been approved as the first registered brand for lithium carbonate futures on the Guangzhou Futures Exchange, effective February 2, 2026. Less than two weeks later, on February 4, 2026, Tianqi announced a strategic cooperation agreement with Envision Greenwise focused on end-of-life lithium battery recycling, joint R&D, black mass supply and industrial collaboration in Hong Kong.

Purchase This Exclusive Report: https://www.datamintelligence.com/buy-now-page?report=battery-grade-lithium-compounds-market?kailas

4. Company profiles

4.1 Albemarle Corporation

Albemarle remains one of the market's most important reference points because it is showing what disciplined lithium leadership looks like in a lower-price but still structurally attractive environment. In its full-year 2025 results, the company reported US$1.3 billion in operating cash flow, US$692 million in free cash flow and approximately US$450 million in cost and productivity improvements. It also disclosed asset-optimization actions including the sale of Eurecat for US$123 million in January 2026 and the expected sale of a controlling stake in Ketjen in the first quarter of 2026. Those moves matter because they show Albemarle using capital discipline and portfolio simplification to protect strategic flexibility.

On the operating side, Albemarle's February 2026 Kemerton decision was significant. The plant processes spodumene from Greenbushes, but the company chose to idle the remaining train to improve financial outcomes rather than push volume into a less favorable pricing environment. That is a commercially rational signal for the broader market: future winners in battery-grade lithium compounds will not be measured by conversion capacity alone, but by how efficiently and profitably that capacity is deployed.

Albemarle is also keeping U.S. optionality alive. Its March 2026 Kings Mountain milestone positions the company with a potentially strategic domestic source of spodumene feed for future North American supply-chain needs. For senior decision-makers, Albemarle's profile now combines cash discipline, portfolio pruning, downstream flexibility and regional supply optionality in a single operating model.

4.2 SQM

SQM's recent profile is defined by scale, process innovation and commercial execution. In its fourth-quarter 2025 results, the company said it delivered record-high sales volumes across both lithium businesses, was operating at full capacity and saw improving supply-demand balance from late 2025 onward. It also said it was increasing refining of lithium carbonate from lithium sulfate in China through tolling agreements, which shows the company's willingness to use multiple conversion pathways to keep qualified lithium flowing into end markets.

What stands out most, however, is the combination of new product flow and lower-footprint production. SQM said the first shipment of lithium hydroxide produced in Australia at Kwinana was celebrated in January 2026, and that the operation had been certified under the International Lithium Association's life-cycle methodology with a 37% lower emissions footprint than traditional hard-rock lithium refined in China. That is commercially meaningful because ESG performance is increasingly part of customer qualification, especially for global cathode and battery programs.

SQM's longer-term position also benefits from its public-private partnership with Codelco. The companies have structured a collaboration for refined lithium production in the Salar de Atacama through 2060, with targeted additional production of 300,000 tonnes of LCE in 2025-2030 and 280,000 to 300,000 tonnes annually in 2031-2060, while incorporating new technologies aimed at better water balance, higher recovery and minimized freshwater use. The companion Salar Futuro program also highlights mechanical evaporation, direct lithium extraction and desalinated seawater rather than continental freshwater, reinforcing SQM's positioning around sustainable, high-value lithium output.

4.3 Ganfeng Lithium Group Co., Ltd.

Ganfeng is one of the most technically diversified companies in the market. The company says it operates across upstream lithium resources, midstream refining and lithium metal, downstream batteries and recycling, and is the only company with commercial-scale technologies to extract lithium from brine, ore and recycled materials. It also says its lithium compounds capacity ranks among the largest globally and that it offers more than 40 lithium compounds and metal products. That breadth matters because the future of battery-grade lithium compounds is expanding beyond a two-product market.

Its project execution has also been visible. Ganfeng disclosed that the Mariana project officially commenced operations in 2025, and its annual report states that Phase I of the project's production line, with planned annual capacity of 20,000 tonnes of lithium chloride, entered operation in February 2025, supporting stable supply from the second half of 2025 onward. The company also said the first shipment from the Goulamina project in Mali had been dispatched to China, reinforcing its multi-region raw-material base.

The more strategic story, though, is Ganfeng's work in specialty lithium chemistries. The company disclosed mass-production expansion of battery-grade lithium sulfide in 2024, supply to more than 20 downstream customers, sulfide electrolyte conductivity of 3 mS/cm, LLZO conductivity of 1.7 mS/cm, LATP conductivity of 1.4 mS/cm, and polymer electrolyte membranes with conductivity above 0.5 mS/cm and thickness below 30 μm. It also said its lithium metal-related battery development can support energy density above 500 Wh/kg. For technology leaders, that makes Ganfeng more than a volume producer. It is a company trying to bridge mainstream lithium compounds and next-generation electrochemistry.

4.4 Rio Tinto Lithium

Rio Tinto has become a more important player in this market because it is combining acquisition-led scale, project financing and downstream buildout. In March 2025, the company completed its US$6.7 billion acquisition of Arcadium Lithium, bringing those assets into the Rio Tinto Lithium platform. Rio Tinto said the acquisition would help it grow its Tier 1 lithium assets to more than 200,000 tonnes per year of LCE by 2028. That is one of the clearest large-scale strategic bets currently visible in the market.

The company has backed that acquisition with project capital. In March 2026, Rio Tinto secured US$1.175 billion for the Rincon project in Argentina, supporting a US$2.5 billion development designed to produce about 60,000 tonnes per year of battery-grade lithium carbonate with first production expected in 2028 and a mine life of around 40 years. That financing matters because it signals third-party confidence in long-duration battery-grade lithium capacity even after the sector's price correction.

Rio Tinto is also moving deeper into North American downstream lithium. In February 2026, it increased its stake in Nemaska Lithium to 53.9%, took direct management control, and disclosed that the Bécancour lithium hydroxide plant was 60% complete at year-end 2025. With Quebec planning up to US$200 million in additional equity investment and Rio Tinto committing more than US$300 million in 2026, the company is clearly positioning itself across resource extraction, refined lithium carbonate and battery-grade hydroxide manufacturing.

5. Strategic takeaway for decision-makers

The Battery Grade Lithium Compounds Market is no longer a narrow raw-material story. It is becoming a strategic market defined by who can deliver the right molecule, at the right purity, in the right region, with the right cost and emissions profile, into increasingly demanding battery supply chains. Current industry signals point to a market where customer-certified hydroxide and carbonate matter more, specialty compounds are gaining strategic relevance, recycling and DLE are moving closer to mainstream commercialization, and capital is flowing toward vertically integrated platforms rather than isolated upstream positions.

That is why the move from US$8.43 billion in 2025 to US$43.28 billion by 2033 deserves board-level attention. A market adding US$34.85 billion in new value at a 22.7% CAGR is not just growing. It is being restructured. The companies most likely to win over the next cycle are the ones that combine conversion discipline, technology depth, recycling or recovery optionality, and regional supply assurance with the ability to meet increasingly strict battery-customer qualification standards

Contact:

Fabian

DataM Intelligence 4market Research LLP

6th Floor, M2 Tech Hub, DataM Intelligence 4market Research LLP, Lalitha Nagar, Habsiguda, Secunderabad, Hyderabad, Telangana 500039

USA: +1 877-441-4866

UK: +44 161-870-5507

Email: fabian@datamintelligence.com

About DataM Intelligence

DataM Intelligence is a renowned provider of market research, delivering deep insights through pricing analysis, market share breakdowns, and competitive intelligence. The company specializes in strategic reports that guide businesses in high-growth sectors such as nutraceuticals and AI-driven health innovations.

To find out more, visit https://www.datamintelligence.com/ or follow us on Twitter, LinkedIn and Facebook.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Battery Grade Lithium Compounds Market to Add US$34.85 Billion by 2033 as Carbonate, Hydroxide and Specialty Lithium Chemistries Move to the Core of Battery Supply Chains here

News-ID: 4466051 • Views: …

More Releases from DataM intelligence 4 Market Research LLP

Next-Generation Anode Materials Market Size to Reach USD 7.0 Billion by 2033 as …

Next-Generation Anode Materials Market

April 11, 2026 - The next-generation anode materials market is witnessing robust growth, with the market size reaching USD 3.1 billion in 2025 and projected to expand to USD 7.0 billion by 2033, registering a strong CAGR of 10.6% during 2026-2033.

This growth trajectory reflects an absolute market expansion of approximately USD 3.9 billion over the forecast period. On an annual basis, the market is expected to add…

Semiconductor and IC Packaging Materials Market Size to Reach USD 93.7 Billion b …

April 11, 2026 - The global Semiconductor and IC Packaging Materials Market reached USD 43.1 billion in 2023 and is expected to reach USD 93.7 billion by 2031, growing at a CAGR of 10.2% during the forecast period of 2024-2031. The market is gaining strong commercial momentum as semiconductor manufacturers move toward more advanced package architectures that require better thermal performance, higher interconnect density, lower warpage, and greater mechanical reliability…

Printing Inks Market to Add USD 5.27 Billion by 2033 as Packaging-Grade, Regulat …

April 11, 2026 - The global Printing Inks Market was valued at USD 22.05 billion in 2025 and is projected to reach USD 27.32 billion by 2033, growing at a CAGR of 2.8% from 2026 to 2033. That translates into roughly USD 5.27 billion in incremental market value and about 23.9% total expansion over the period.

That growth rate may look moderate on paper, but for senior decision-makers it should not…

Battery Material Market to Add US$35.1 Billion by 2033 as Safer Chemistries, Loc …

April 11, 2026 - The global Battery Material Market reached US$59.1 billion in 2026 and is expected to reach US$94.2 billion by 2033, growing at a CAGR of 6.0% during 2026-2033. That implies an incremental value opportunity of US$35.1 billion and a total market expansion of roughly 59.4% over the forecast period. The timing is not accidental. The International Energy Agency says battery demand for the energy sector reached the…

More Releases for Lithium

Lithium Compounds Market To Witness Massive Growth | Competitive Outlook Albemar …

Lithium compounds market is expected to gain market growth in the forecast period of 2020 to 2027. Data Bridge Market Research analyses the market to account 20.04 billion by 2027 growing with the CAGR of 20.90% in the above-mentioned forecast period. Huge investments in infrastructure developments is a vital factor driving the growth of lithium compounds market swiftly.

The Lithium Compounds Market research report assesses the ongoing as well as future…

Lithium Compounds Market 2020-2025 Global Analysis & Opportunity Assessment | Li …

The global Lithium Compound market size is projected to reach over USD 9 billion by 2025. Lithium is an alkali metal that is generally present among the soil, human body, animals, and plants. It is a light weight metal with less density when compared to other elements. The lithium compounds, primarily find its application in rechargeable and non-rechargeable batteries. The lithium is primarily used across glass & ceramics, Li-ion batteries,…

Lithium Compounds Market Analysis & Industry Outlook 2019-2025| Livent Corporati …

The global Lithium Compound market size is projected to reach over USD 9 billion by 2025. Lithium is an alkali metal that is generally present among the soil, human body, animals, and plants. It is a light weight metal with less density when compared to other elements. The lithium compounds, primarily find its application in rechargeable and non-rechargeable batteries. The lithium is primarily used across glass & ceramics, Li-ion batteries,…

Lithium Compounds Market Scenario & Industry Outlook 2019-2025| Livent Corporati …

The global lithium compound market size is projected to reach over USD 9 billion by 2025.The report on lithium compound market is aimed to equip report readers with versatile understanding on diverse marketing opportunities that are rampantly available across regional hubs. A thorough assessment and evaluation of these factors are likely to influence incremental growth prospects in the lithium compound market.

Request sample copy of this report at: https://www.adroitmarketresearch.com/contacts/request-sample/1445

Additionally, in this…

Lithium Fluoride Market players Jiangxu Ganfeng Lithium, Harshil Fluoride Brivo …

The developing in the glass, optics and electronic and electrical industries has initiated a high demand for Lithium and related compounds. Lithium and lithium based compounds are one the key substances that have dynamic usage, either as a feedstock or as product. One of the most commercially important compound is Lithium fluoride. Lithium fluoride is an odorless, crystalline lithium salt manufactured by the reaction of lithium hydroxide with hydrogen fluoride.…

Lithium Hydroxide Market | Key Players are FMC Corporation, Sociedad Quimica Min …

Lithium Hydroxide (LiOH) is an inorganic compound that is insoluble in water and partially soluble in ethanol. It is commercially available as a monohydrate (LiOH.H2O) and in anhydrous form, both of which are strong bases. On the basis of purity level, it is also available in battery grade and technical grade. Lithium hydroxide is manufactured by means of a metathesis reaction between calcium hydroxide and lithium carbonate and it finds…