Press release

Solid-State Battery Market: From Lab Breakthroughs to Pre-Committed Demand in Next-Gen Energy Systems

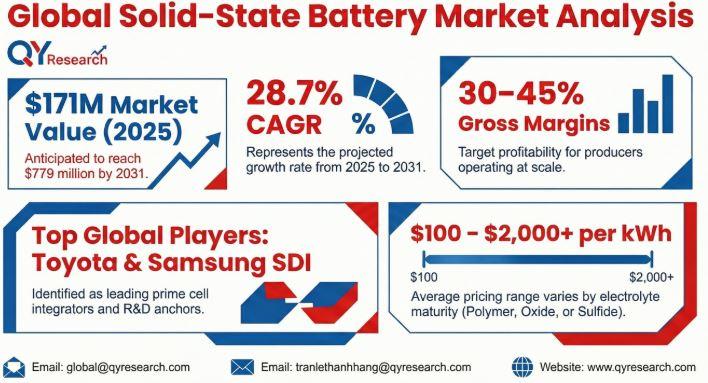

The global solid‐state battery (SSB) market is transitioning from laboratory‐scale experimentation to pre‐commercial deployment, marking a critical inflection point in next‐generation energy storage. The market is projected to grow from USD 171M in 2025 to USD 779M in 2031, at a CAGR of ~28.7%. However, headline growth significantly understates the opportunity, as value is not driven by volume today, but by future capacity reservation and strategic OEM alignment. The investment thesis is shifting from incremental battery improvement toward architectural transformation of energy systems, with value concentrated in solid electrolyte interfaces, lithium‐metal or silicon anodes, and manufacturing process innovation. A key insight is that solid‐state batteries are not yet a mass‐market product; they are a pre‐committed future revenue stream, where demand is being secured years ahead of commercialization.

Why This Market Is at an Inflection Point

This market is at an inflection point because several structural forces are converging. Lithium‐ion batteries are nearing their physical limits, with a practical plateau around 250-300 Wh/kg, while EV OEMs are aggressively targeting 1,000 km range and 10‐minute charging. First commercial SSB platforms are expected between 2028 and 2030. At the same time, OEMs are entering multi‐year co‐development agreements, governments are funding sovereign battery strategies, and supply chains are being restructured for next‐generation chemistries. The implication is that the market is shifting from technology validation toward pre‐commercial demand formation, where contractual commitments and capacity reservations increasingly define the landscape.

What the Market Gets Wrong About Solid-State Batteries (SSB)

The idea that "SSBs will rapidly replace lithium‐ion" is misleading; the reality is coexistence, with SSBs initially targeting premium and high‐performance segments rather than displacing incumbent technology overnight. The notion that "technology readiness is the main risk" also oversimplifies the challenge; in practice, manufacturing scalability and yield are the true bottlenecks. Furthermore, the assumption that "all electrolyte types will compete equally" overlooks the emerging leadership of sulfide‐based systems as the early frontrunner for EV applications. The overarching implication is that the real opportunity lies not simply in the technology itself, but in which players can scale it reliably, secure OEM partnerships, and master the manufacturing and materials supply chain.

A. CONSUMPTION MARKET DYNAMICS

The solid-state battery market is fundamentally driven by the "Safety and Density" imperative. Consumption is anchored by premium EV manufacturers, aerospace firms, and defense agencies where energy density and fire suppression are mission-critical rather than cost-optimized variables.

Core Demand Drivers:

• High-Performance Electric Mobility: Automakers are prioritizing SSBs to unlock "1,000 km+ range" vehicles and 10-minute ultra-fast charging. This has accelerated procurement of sulfide-based electrolytes and silicon-composite anodes.

• Electric Aviation (eVTOL): Hypersonic and subsonic electric flight programs require power-to-weight ratios that liquid Li-ion cannot meet. Demand is rising for cells exceeding 400-500 Wh/kg.

• Critical Infrastructure & Robotics: Solid-state's thermal stability makes it the preferred choice for humanoid robots and mission-critical medical devices where battery failure is not an option.

From an investor's perspective: EVs are the most attractive segment because they offer the largest long term revenue potential, driven by OEM demand for higher range, safety, and faster charging. Consumer electronics provide early monetization with quicker product cycles and lower integration barriers, enabling near term revenue even at smaller volumes. Aerospace offers validation and premium pricing power, while energy storage systems represent a long term optionality bet as SSBs could eventually displace lithium ion in grid scale applications once costs and scale improve.

Regional Consumption Dynamics

• North America and Europe are currently the primary sources of early‐stage demand for solid‐state batteries, fueled by premium EV OEMs seeking high‐performance, long‐range platforms and by defense‐funded programs that prioritize safety, energy density, and reliability over cost. These regions act as incubators for technology validation and pilot deployments, where policy‐driven electrification targets and strategic innovation funding help de‐risk first‐commercial systems.

• Asia‐Pacific remains the strategic demand center, anchored by sovereign battery roadmaps in Japan, Korea, and China that treat next‐generation energy storage as a national security and industrial‐policy priority. Vertically integrated EV ecosystems across the region-spanning raw materials, cell manufacturing, and vehicle assembly-enable faster scale‐up and tighter co‐development between battery makers and OEMs, reinforcing the region's centrality in global SSB deployment.

• Within Asia‐Pacific, Southeast Asia, and particularly Vietnam, Thailand, Indonesia is emerging as a localized demand engine, driven by rapid EV adoption, supportive industrial policies, and projections that battery demand could reach about 46.9 GWh by 2030. The broader implication is that SSB demand is evolving from small, pilot‐driven projects toward regionally anchored, policy‐supported ecosystems, where long‐term capacity reservation and sovereign‐backed supply chains increasingly define competitive advantage.

B. PRODUCTION AND SUPPLY CHAIN

The SSB supply chain is transitioning from bespoke R&D to highly specialized, capital-intensive production ecosystems. Producers operating at scale target gross margins of 30-45%, protected by proprietary material IP and high certification barriers.

Where Value Is Captured:

• Upstream Material Kingmakers: Companies controlling the production of lithium sulfide and ceramic separators (e.g., Idemitsu Kosan) hold the highest-margin positions.

• Specialized Manufacturing Equipment: The shift to "dry-room" environments and stack-press assembly creates a high-moat sector for equipment providers like LiCAP Technologies.

• Tier-1 Cell Integrators: Primes like Samsung SDI and Toyota who manage the complex interface between solid electrolytes and high-capacity electrodes.

Southeast Asia and Vietnam are emerging as force multipliers for global SSB primes, moving beyond simple assembly into high-value manufacturing nodes.

• Vietnam as a Mineral & Processing Node: Vietnam holds 3.7 million tons of nickel reserves and untapped graphite, critical precursors for advanced battery chemistries. By moving from raw ore exports to localized lithium and nickel processing, Vietnam is capturing a larger share of the battery value chain.

• SEA's Role in "Circular" Supply Chains: Vietnam is positioning itself as a regional hub for battery "Reverse Supply Chain Management" (RSCM), focusing on second-life applications and material recovery-a critical component for the long-term sustainability of the SSB market.

• Production Integration: With over USD 2 billion in battery-related FDI as of 2023, Vietnam is leveraging its cost-competitive labor and free trade agreements (FTAs) to become a primary export platform for the next generation of energy storage systems.

Latest Technological Developments:

• Anode-Free Architectures: Pure-play developers are moving toward "anode-less" designs where the lithium-metal anode forms during the first charge, drastically reducing weight and manufacturing steps.

• Sulfide-Based Electrolytes: These are emerging as the industry standard due to ionic conductivity that rivals liquid electrolytes, enabling superior performance at room temperature.

• Dry-Electrode Processing: Eliminating toxic solvents and massive drying ovens reduces the factory footprint by 30-40% and lowers the overall cost per kWh..

Solid-State Battery (SSB) Technology by Electrolyte Type

• Sulfide-Based Electrolytes: The frontrunner for high-performance EV applications; offers the highest ionic conductivity (rivalling liquid electrolytes) and excellent contact with electrodes.

• Oxide-Based Electrolytes (Ceramics): Known for exceptional thermal stability and mechanical strength; virtually non-flammable. Common types include LLZO and LATP. Primarily targeted for high-safety aerospace and medical applications due to processing brittleness.

• Polymer-Based Electrolytes: Utilize a solid polymer matrix (like PEO) often infused with lithium salts. These are the easiest to manufacture using existing lithium-ion equipment but typically require elevated operating temperatures to achieve sufficient conductivity.

• Halide-Based Electrolytes: Emerging class focused on high-voltage stability and moisture resistance. Often used as a coating or integrated into cathode composites to enable high-nickel chemistries without degradation.

• Composite/Hybrid Systems: Formulations blending polymers with ceramic fillers to balance mechanical flexibility (from polymers) with high ionic transport (from ceramics), aiming for a "best of both worlds" solution for mass-market EVs.

Solid-State Batteries by Critical Components

• Solid Electrolyte (SE) Powder: The defining "separator" and ion-conductor; its purity and particle size distribution determine the internal resistance and charge rate of the cell.

• Anode Host Materials: Focused on Lithium Metal (for maximum energy density) or Silicon-Anode composites. This component is the primary driver of the "500+ Wh/kg" energy density targets.

• Cathode Active Materials (CAM): High-nickel (NMC) or Cobalt-free chemistries modified with thin-film coatings to prevent side reactions with the solid electrolyte during high-voltage cycling.

• Conductive Binders & Additives: Specialized polymers that maintain the physical "triple-point" contact between the electrolyte, active material, and carbon black as the battery expands and contracts.

Solid-State Battery by Market Segment

• Electric Vehicles (EVs): The ultimate volume driver. Focus is on "Range Anxiety" elimination and 10-minute ultra-fast charging. Top-tier OEMs (Toyota, VW, BMW) are the primary R&D anchors.

• Consumer Electronics: High-margin, low-volume entry point. Focused on thin-profile batteries for wearables, smartphones, and foldable devices where volumetric energy density and safety are premium.

• Aerospace & Defense: Niche sector prioritizing non-flammability and wide temperature operating ranges. Solid-state's lack of liquid leakage makes it ideal for high-altitude and vacuum environments.

• Stationary Energy Storage (ESS): Long-term potential segment focused on non-combustible grid storage, though currently limited by the high cost per kWh compared to LFP (Lithium Iron Phosphate).

Program Costs and Pricing Variations

By Electrolyte Material Maturity

• Polymer SSBs (Commercialized): USD 100-150 per kWh. Currently used in niche bus fleets; cost-competitive but limited by energy density and heat requirements.

• Oxide/Ceramic SSBs (Prototyping): USD 400-800 per kWh. High costs driven by expensive sintering processes and brittle yield losses.

• Sulfide SSBs (Pre-Pilot): USD 800-2,000+ per kWh. Extremely high current cost due to the scarcity of high-purity Lithium precursors and specialized "dry room" CAPEX.

By Manufacturing Process Requirements

• Dry Electrode Coating: A cost-saving "holy grail" that eliminates toxic solvents (NMP) and massive drying ovens, potentially reducing floor space by 70%.

• High-Pressure Assembly: Specialized mechanical housing required to keep solid layers in constant contact; adds weight and cost compared to standard liquid cell "pouches."

Top Producers & Developers of Solid-State Battery

• Toyota Motor Corp. / Prime Planet Energy & Solutions (Japan, TYO: 7203)

• Samsung SDI Co., Ltd. (South Korea, KRX: 006400)

• LG Energy Solution, Ltd. (South Korea, KRX: 373220)

• CATL (China, SHE: 300750)

• SK On (South Korea, Private)

• Panasonic Holdings Corporation (Japan, TYO: 6752)

• BMW Group (Germany, ETR: BMW)

• Hyundai Motor Company (South Korea, KRX: 005380)

• Bosch Group (Germany, Private)

• Dyson Ltd. (UK, Private)

• Apple Inc. (USA, NASDAQ: AAPL)

• Ganfeng Lithium Group Co., Ltd. (China, SHE: 002460)

• WeLion New Energy Technology Co., Ltd. (China, Private)

• Murdock/Idemitsu Kosan Co., Ltd. (Japan, TYO: 5019)

• Murata Manufacturing Co., Ltd. (Japan, TYO: 6981)

• QuantumScape Corporation (USA, NYSE: QS)

• Solid Power, Inc. (USA, NASDAQ: SLDP)

• Bolloré SE / Blue Solutions (France, EPA: BLUE)

• ProLogium Technology Co., Ltd. (Taiwan, Private)

• Factorial Energy (USA, Private)

• Jiawei Technology (China, Private)

• Ilika plc (UK, LSE: IKA)

• Excellatron Solid State, LLC (USA, Private)

• Cymbet Corporation (USA, Private)

• Mitsui Mining & Smelting Co., Ltd. (Japan, TYO: 5706)

• Front Edge Technology, Inc. (USA, Private)

• SolidEdge (USA, Private)

Go-to-Market & Buyer Structure

The solid‐state battery (SSB) market is fundamentally shaped by vertical integration and strategic joint ventures, as the battery is no longer a simple "drop‐in" component but a core part of the system‐level architecture.

• Automotive OEMs act as primary co‐developers and demand anchors, driving procurement through pre‐commercial agreements, pilot production runs, and long‐term platform integration rather than traditional mass‐market purchasing, which creates a demand curve that is low‐volume today but sharply ramps up after commercialization.

• Upstream chemical players such as Idemitsu are moving downstream, transforming from commodity suppliers into high‐value electrolyte providers by capturing margin through proprietary material IP and long‐term supply contracts linked to specific OEM platforms.

SSB demand is not transactional; it is pre‐committed, co‐developed, and contractually locked‐in long before full‐scale production begins.

Key Market Risks

• The "LFP Wall": Massive cost reductions in liquid-electrolyte LFP batteries may make SSBs economically unviable for all but "Luxury/Performance" vehicles.

• Manufacturing Scalability: Moving from a lab-scale "multistack" cell to GWh-scale continuous production remains unproven.

• Supply Chain Bottlenecks: Sulfide-based SSBs require a massive scale-up of production, which currently lacks a global infrastructure.

Investment Implications

• High-Conviction Areas: Companies mastering Lithium Metal Anode stabilization and Sulfide Precursor production.

• Enabling Technologies: Manufacturers of High-Pressure Isostatic Presses (HIP) and Solvent-Free Coating lines.

• Strategic Themes: "Safe-by-Design" chemistry as a regulatory moat against cheaper, flammable liquid-ion imports.

Conclusion

Solid‐state batteries represent a structural shift from incremental battery improvement to next‐generation energy architecture, redefining how energy storage is integrated into vehicles and infrastructure. The winners will be defined not by who invents the best chemistry, but by who can scale that chemistry reliably, secure long‐term OEM partnerships, and control critical material bottlenecks across the supply chain. Over time, SSBs will evolve into a strategic layer in global energy and mobility systems, shaping the competitiveness of automakers, battery producers, and entire national industrial ecosystems.

Related Report Recommendations:

Global Solid State Batteries Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/5555927/solid-state-batteries

Global Solid State Batteries Market Size, Status and Forecast 2026-2032 https://www.qyresearch.com/reports/5554615/solid-state-batteries

Solid State Batteries - Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/5493891/solid-state-batteries

Global Solid State Batteries Market Research Report 2026 https://www.qyresearch.com/reports/5533501/solid-state-batteries

Global All-Solid-State Battery Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/5562313/all-solid-state-battery

Global All-Solid-State Battery Market Size, Status and Forecast 2026-2032 https://www.qyresearch.com/reports/5558545/all-solid-state-battery

All-Solid-State Battery - Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/5558539/all-solid-state-battery

Global All-Solid-State Battery Market Research Report 2026 https://www.qyresearch.com/reports/5532171/all-solid-state-battery

Solid State Bean Battery - Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/5911133/solid-state-bean-battery

Global Solid State Bean Battery Market Research Report 2026 https://www.qyresearch.com/reports/5906640/solid-state-bean-battery

Global Oxide Solid State Battery Market Outlook, In Depth Analysis & Forecast to 2032 https://www.qyresearch.com/reports/6396003/oxide-solid-state-battery

Global Oxide Solid State Battery Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6391670/oxide-solid-state-battery

Global Power Solid State Battery Market Outlook, In Depth Analysis & Forecast to 2032 https://www.qyresearch.com/reports/6386657/power-solid-state-battery

Global Power Solid State Battery Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6382059/power-solid-state-battery

Global SMD Solid-State Batteries Market Outlook, In Depth Analysis & Forecast to 2032 https://www.qyresearch.com/reports/6312779/smd-solid-state-batteries

Global SMD Solid-State Batteries Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6306927/smd-solid-state-batteries

Global eVTOL Solid-State Battery Market Outlook, In Depth Analysis & Forecast to 2032 https://www.qyresearch.com/reports/6243013/evtol-solid-state-battery

Contact Information:

Tel: +1 626 2952 442 (US); +86-1082945717 (China); +84 865 216594 (Vietnam)

Email: global@qyresearch.com; tranlethanhhang@qyresearch.com

Website: www.qyresearch.com

Address: Room 2905, Vili International, 167 Linhe West Road, Tianhe District, Guangzhou, Guangdong Province, China

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data. Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details. We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivery. More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Solid-State Battery Market: From Lab Breakthroughs to Pre-Committed Demand in Next-Gen Energy Systems here

News-ID: 4460595 • Views: …

More Releases from QY Research

Top 30 Indonesian Soft Drink Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

PT Mayora Indah Tbk (MYOR)

PT Indofood CBP Sukses Makmur Tbk (ICBP)

PT Indofood Sukses Makmur Tbk (INDF)

PT Ultrajaya Milk Industry & Trading Company Tbk (ULTJ)

PT Sariguna Primatirta Tbk (CLEO)

PT Akasha Wira International Tbk (ADES)

PT Multi Bintang Indonesia Tbk (MLBI)

PT Delta Djakarta Tbk (DLTA)

PT Kino Indonesia Tbk (KINO)

PT Garudafood Putra Putri Jaya Tbk (GOOD)

PT Tempo Scan…

Southeast Asia Emerges as the Strategic Manufacturing Hub for Plant-Based Shrink …

The global Plant Based Shrink Film market is entering a structural expansion phase driven by regulatory pressure, carbon-accounting mandates, and multinational packaging conversion programs. What was previously a niche sustainability segment tied to consumer branding has evolved into a capital-intensive materials platform involving bio-resin integration, advanced film orientation systems, and high-performance barrier engineering. The industry is increasingly transitioning away from commodity-driven volume competition toward technology-linked margin capture, particularly in biaxially…

Outdoor BBQ Grills Transition from Commodity Hardware to Premium Outdoor Living …

The global Outdoor BBQ Grills market is entering a structural inflection phase as value creation shifts away from pure shipment growth toward premiumized hardware systems, integrated smart controls, and vertically optimized manufacturing platforms. The market is projected to expand from approximately USD4.04 billion in 2025 to USD5.92 billion by 2032, representing a CAGR of 6.3%. Unit shipments are estimated at roughly 24.5 million units in 2025, supported by rising outdoor…

Reactive Power, Renewable Energy, and UHV Transmission: The Emerging Investment …

The global Oil Immersed Single Phase Shunt Reactor market is entering a structural investment cycle driven less by transmission line volume growth and increasingly by grid complexity, renewable intermittency, and ultra-high-voltage (UHV) infrastructure deployment. The market is valued at approximately USD 449 million in 2025 and is projected to reach nearly USD 653 million by 2032, expanding at a CAGR of 5.5%.

The investment profile of the industry has shifted…

More Releases for Solid

Solid-State Battery Market Share, Growth, Future outlook | Leading Companies 202 …

"Solid-State Battery Market is anticipated to grow at a high CAGR during the forecast peroid 2024-2031."

DataM Intelligence unveils exclusive insights into the Solid-State Battery Market 2026, highlighting emerging trends, growth drivers, and key regional opportunities worldwide. The report helps solve critical business challenges by identifying high-growth segments and reducing investment risks through actionable forecasts. With in-depth competitive benchmarking, it enables smarter strategies and confident decision-making.

Download your exclusive sample report today:…

Solid-State Battery Market to Witness Huge Growth by 2031 - Excellatron Solid St …

DataM Intelligence has published a new research report on "Solid-State Battery Market Size 2024". The report explores comprehensive and insightful Information about various key factors like Regional Growth, Segmentation, CAGR, Business Revenue Status of Top Key Players and Drivers. The purpose of this report is to provide a telescopic view of the current market size by value and volume, opportunities, and development status.

Get a Free Sample Research PDF -…

Polymer-Based Solid State Battery Market With In-Detailed Competitor Analysis, F …

WMR has released a report titled "Polymer-Based Solid State Battery Market: Industry Trends, Share, Size, Growth, Opportunity, and Forecast 2024-2031", which includes market percentage records and a thorough enterprise analysis. This report looks at the market's competition, geographic distribution, and growth potential. This comprehensive report encompasses industry performance, critical success factors, risk assessment, manufacturing prerequisites, project expenses, economic analysis, anticipated return on investment (ROI), and profit margins.

This comprehensive report delves…

Solid of Sodium Methylate Market Solid of Sodium Methylate Market Size and Forec …

𝐔𝐒𝐀, 𝐍𝐞𝐰 𝐉𝐞𝐫𝐬𝐞𝐲- The global Solid of Sodium Methylate Market is expected to record a CAGR of XX.X% from 2024 to 2031 In 2024, the market size is projected to reach a valuation of USD XX.X Billion. By 2031 the valuation is anticipated to reach USD XX.X Billion.

The Solid of Sodium Methylate market encompasses the production, distribution, and utilization of solid forms of sodium methylate, a versatile chemical compound with…

Solid State Battery Market Financial Insights, Business Growth Strategies | Robe …

Exactitude Consultancy, the market research has completed and published the final copy of the detailed research report on the Solid State Battery Market. The Solid State Battery Market is expected to register a CAGR of over 36.01% over the forecast period.

According to a recent report published by Exactitude Consultancy, titled, "Solid State Battery Market by Type (Thin Film Battery, Portable Battery) Capacity (Below 20mAh, 20mAh-500mAh, above 500mAh) Application Consumer Electronics,…

Thin Film Solid State Battery Market Size 2022 By Top Key Players -Solid Power, …

A solid state battery has a better energy density than a lithium-ion battery that uses a liquid electrolyte solution. There is no need for safety components because there is no threat of an explosion or fire, which frees up space. The battery's capacity can then be increased by adding more active materials because there is more room for them. A solid state battery increases energy density per unit area since…