Press release

Film Adhesive Production Plant DPR & Unit Setup - 2026: Demand Analysis and Project Cost

Market Overview and Growth Potential

The global adhesive film market demonstrates steady growth trajectory, valued at USD 39.08 Billion in 2025. According to IMARC Group's comprehensive market analysis, the market is projected to reach USD 56.59 Billion by 2034, exhibiting a CAGR of 4.2% from 2026-2034. This sustained expansion is driven by increasing demand for adhesive films in electronics and semiconductor manufacturing where miniaturization requires ultra-precise, solvent-free bonding solutions, growing adoption in automotive lightweighting programs replacing mechanical fasteners with structural adhesive film assemblies, rapid growth in flexible packaging solutions utilizing heat-sealable and peelable adhesive film constructions, expanding aerospace composite bonding applications requiring high-temperature-resistant epoxy and modified bismaleimide film adhesives, and rising healthcare and medical device manufacturing demand for biocompatible pressure-sensitive and thermal-cure adhesive films.

Request for a Sample Report: https://www.imarcgroup.com/film-adhesive-manufacturing-plant-project-report/requestsample

Film adhesives are precision-manufactured solid-state adhesive systems supplied in a thin uniform film format-typically between 0.025 mm and 0.5 mm thickness-on release liner backing, enabling clean, controlled, and void-free application to substrates that is not achievable with liquid or paste adhesive systems. The product range encompasses pressure-sensitive adhesive films using acrylic, rubber, or silicone adhesive systems on polyester, polyolefin, or polyimide carrier films; heat-activated and thermal-cure structural film adhesives based on epoxy, polyurethane, phenolic, or cyanate ester chemistry for aerospace and defense composite bonding; electrically conductive and anisotropic conductive film adhesives for electronic interconnect applications; optically clear adhesive films for display lamination and optical bonding; and specialty films for pipe corrosion protection, architectural glazing, and graphic arts applications. The choice of adhesive chemistry, carrier film substrate, liner system, and processing parameters collectively define the performance envelope for temperature resistance, bond strength, chemical resistance, electrical properties, and shelf life.

The film adhesive market is witnessing robust demand due to the structural shift in advanced manufacturing toward cleaner, more precise, and more material-efficient bonding solutions across every sector, the rapid growth of the electric vehicle industry creating new demand for battery cell stack bonding, thermal interface, and structural adhesive film applications, and the electronics industry's accelerating miniaturization driving adoption of ultra-thin die-attach, anisotropic conductive, and optical clear adhesive films. Government-led PLI scheme electronics manufacturing incentives and semiconductor fabrication investments further strengthen market prospects.

Plant Capacity and Production Scale

The proposed film adhesive production facility is designed with an annual production capacity ranging between 1,000 - 5,000 MT, enabling economies of scale while maintaining operational flexibility. This capacity range allows manufacturers to cater to diverse market segments-from pressure-sensitive adhesive films on polypropylene and polyester carriers for packaging, labeling, and graphics applications to structural epoxy film adhesives for aerospace composite bonding, anisotropic conductive films for electronics interconnect, optical clear adhesive films for display and touch panel lamination, specialty thermal interface and die-attach films for semiconductor packaging, and architectural and industrial protective film adhesive constructions-ensuring steady demand and consistent revenue streams across multiple high-value industrial verticals.

Ask Analyst for Customization:

https://www.imarcgroup.com/request?type=report&id=12448&flag=C

Financial Viability and Profitability Analysis

The film adhesive production business demonstrates healthy profitability potential under normal operating conditions.The financial projections reveal:

• Gross Profit Margins: 30-40%

• Net Profit Margins: 15-22%

These margins are supported by stable and growing demand across electronics, automotive, aerospace, packaging, and healthcare sectors, value-added specialty chemistry formulation, precision coating technology, and application-specific qualification positioning enabling significant pricing premiums above commodity pressure-sensitive tape economics, and the proprietary formulation know-how, coating process expertise, and application qualification investments that create meaningful technical and commercial entry barriers sustaining established producers' competitive positioning. The project demonstrates strong return on investment (ROI) potential, making it an attractive proposition for specialty chemical manufacturers and advanced material investors seeking to establish or expand film adhesive production capacity serving the global high-performance bonding solutions market.

Production Cost Structure Analysis

Understanding the operating expenditure (OpEx) is crucial for effective financial planning and cost management. The production cost structure for a film adhesive manufacturing plant is primarily driven by:

• Raw Materials: 65-75% of total OpEx

• Utilities: 15-20% of OpEx

Raw materials constitute the dominant portion of production costs, with adhesive polymer systems-including acrylic emulsions or solvent acrylic polymers, epoxy resins and hardeners, polyurethane prepolymers, rubber-based adhesive compounds, and silicone polymers-being the primary inputs alongside carrier film substrates including biaxially oriented polyester, polyimide, polypropylene, and polyethylene films, release liners including siliconized paper and polyester, crosslinking agents, tackifiers, plasticizers, and functional additives. Utilities reflect the energy requirements for coating line drying ovens, solvent recovery systems, and lamination and slitting equipment operations. Establishing reliable specialty polymer and carrier film supply agreements with qualified raw material suppliers, and investing in proprietary adhesive formulation development that achieves differentiated performance specifications, are the most critical strategies for sustainable production cost management.

Capital Investment Requirements

Setting up a film adhesive production plant requires substantial capital investment across several critical categories:

Land and Site Development: Selection of an optimal location within an established specialty chemical or advanced materials manufacturing zone with access to specialty polymer and carrier film raw material supply chains, and logistics connectivity to electronics assembly, automotive, aerospace, and packaging customer manufacturing facilities. The site must have reliable utilities including high-quality electrical supply and industrial steam or gas for coating oven operations, compliant solvent storage and emission control infrastructure for solvent-borne adhesive coating lines, and clean manufacturing environments for optical and electronic grade adhesive film production.

Machinery and Equipment: The largest portion of capital expenditure (CapEx) covers specialized adhesive compounding, precision coating, lamination, and slitting equipment essential for production.

Key machinery includes:

• Adhesive formulation reactors, dissolvers, and mixing systems for preparing acrylic, epoxy, rubber, and silicone adhesive compounds

• Precision slot-die, comma bar, gravure, or reverse-gravure coating heads for applying uniform adhesive layers onto carrier films

• Multi-zone drying ovens with precise temperature profiling for solvent evaporation and adhesive crosslinking or drying

• Solvent recovery systems for capturing and recycling solvent vapors from coating oven exhaust streams

• Lamination stations for combining adhesive-coated film with release liner and carrier film substrates in multi-layer constructions

• Precision slitting and rewinding machines for converting coated master rolls into customer-specification widths and lengths

• Die-cutting and sheeting equipment for producing sheet and custom-shape adhesive film formats for electronics and aerospace customers

• Quality control laboratory with peel adhesion, shear, tack, optical, and electrical measurement equipment for adhesive film performance qualification

Civil Works: Building construction, factory layout optimization, and cleanroom and controlled-environment manufacturing infrastructure development appropriate to the grade of adhesive film being produced. The layout should incorporate raw material storage and polymer compounding section, precision coating hall with temperature and humidity control, multi-zone drying ovens and solvent recovery systems, lamination and construction zone, slitting and rewinding hall, die-cutting and sheeting section, quality control laboratory, cleanroom finishing area for optical and electronic grade films, refrigerated cold storage for heat-activated film products, finished goods warehouse, utility block, and administrative offices.

Buy now: https://www.imarcgroup.com/checkout?id=12448&method=2175

Other Capital Costs: Pre-operative expenses, coating line installation and commissioning costs, ISO 9001 quality management system certification, IATF 16949 for automotive application qualification, AS9100 for aerospace application certification, RoHS and REACH chemical compliance documentation, clean-room classification for optical grade film production, initial polymer and film working capital requirements, and contingency provisions for unforeseen process development and coating optimization challenges during plant establishment.

Major Applications and Market Segments

Film adhesive products find extensive applications across diverse high-value industrial and technology market segments, demonstrating their critical enabling role across advanced manufacturing globally:

Electronics and Semiconductor Manufacturing: Primary and highest-growth application segment where optical clear adhesive films for touch panel and display lamination, anisotropic conductive films for chip-on-flex and chip-on-glass interconnects, die-attach films for semiconductor packaging, and electrically insulating polyimide-based adhesive films for flexible printed circuit assembly represent critical functional materials enabling the miniaturization and performance improvement of smartphones, tablets, wearables, and advanced semiconductor packages globally.

Automotive and Electric Vehicles: Rapidly growing structural and functional application where adhesive films bond body panel assemblies and interior trim components replacing mechanical fasteners for weight reduction, seal and protect wire harnesses and battery cell stack assemblies in electric vehicles, provide sound damping and vibration absorption in vehicle cabins, and enable glass and window adhesive bonding in windshield and sunroof installation, with electric vehicle platform growth creating new specialized film adhesive demand for battery thermal management, cell stack bonding, and high-voltage insulation applications.

Flexible Packaging and Labeling: High-volume application where heat-sealable adhesive films provide the sealing layer in flexible pouch and tray packaging for food, pharmaceutical, and consumer products, pressure-sensitive adhesive films enable label stock construction for logistic, product, and promotional labeling, and specialty peelable adhesive films produce easy-open packaging solutions, with the global flexible packaging industry's rapid growth and sustainability-driven innovation in mono-material film constructions creating sustained demand expansion.

Aerospace and Defense: Specialized high-performance application where supported epoxy, modified epoxy, bismaleimide, and cyanate ester structural film adhesives provide the structural bonding layer in carbon fiber and glass fiber composite aerospace assemblies, helicopter rotor blade construction, honeycomb sandwich panel fabrication, and aerospace interior panel bonding where film adhesive's controlled and uniform bond line thickness, void-free application, and superior high-temperature structural performance are essential for airworthiness certification requirements.

Healthcare, Medical Devices, and Wearables: Growing premium segment where biocompatible pressure-sensitive adhesive films provide the skin contact adhesive layer in medical wearable devices, continuous glucose monitors, ECG patches, wound care products, and transdermal drug delivery patches, and where specialty adhesive films enable medical device component assembly with biocompatibility certifications under ISO 10993, creating a high-margin, quality-critical specialty segment for film adhesive producers with medical grade production capability.

Why Invest in Film Adhesive Production?

Electronics Miniaturization Megatrend: The persistent global consumer electronics trend toward thinner, lighter, and more integrated devices is structurally driving demand for ultra-thin and ultra-precise adhesive film bonding solutions that enable the sub-millimeter bonding accuracy and cleanliness required in advanced display lamination, semiconductor packaging, and flexible electronics manufacturing-applications where liquid adhesives cannot achieve the required dimensional control and void-free bonding performance.

EV Battery and Lightweight Automotive Growth: The global electric vehicle transition is creating a new and rapidly growing class of specialized automotive film adhesive applications including battery cell-to-cell bonding, battery module structural adhesive, thermal interface film management, and high-voltage electrical insulation films that were absent from the automotive market before EV adoption, providing film adhesive producers with premium-priced growth applications directly correlated with EV production volume expansion.

Aerospace Composite Manufacturing Expansion: The sustained increase in commercial aircraft production rates and the growing use of fiber-reinforced composite materials in next-generation aircraft structures is driving growing demand for structural film adhesives in composite bonding applications where film adhesives' controlled and reproducible bond line thickness is essential for achieving the structural performance and weight minimization targets required by aircraft certification authorities.

Specialty and Functional Film Premium: Film adhesive producers that develop and qualify proprietary specialty adhesive formulations-including optical clear adhesives meeting ASTM D1003 haze specifications, anisotropic conductive films with controlled particle size and distribution, and aerospace-grade film adhesives with qualified pedigree for specific airframe programs-achieve sustained premium pricing 5-20 times above commodity pressure-sensitive film economics, enabling superior margins through specialty application technology differentiation.

Government Support: Government-led PLI scheme incentives for electronics and specialty chemical manufacturing, semiconductor fabrication ecosystem development creating film adhesive demand, aerospace and defense manufacturing self-reliance programs, medical device manufacturing investment incentives, and specialty chemical export promotion programs further strengthen market prospects and directly support film adhesive production investment.

Import Substitution Opportunities: India's rapidly expanding electronics, automotive, and packaging manufacturing sectors currently import the substantial majority of their specialty adhesive film requirements from Japanese (Nitto Denko, Lintec), American (3M, Avery Dennison), and European manufacturers, creating significant import substitution opportunities for domestically established film adhesive producers that achieve customer application qualification and can supply consistent-quality specialty films with shorter lead times and competitive pricing to growing Indian manufacturing customers.

Manufacturing Process Excellence

The film adhesive production process involves several precision-controlled stages:

• Adhesive Compounding and Preparation: Base polymer-acrylic, epoxy, rubber, polyurethane, or silicone-is dissolved, dispersed, or compounded with crosslinker, tackifier, filler, and functional additive systems in mixing reactors at controlled temperature and agitation to produce a homogeneous adhesive mass of target viscosity, solids content, and rheological properties

• Precision Coating: The prepared adhesive is metered through a precision slot-die, comma bar, or gravure coating head onto the moving carrier film or release liner substrate at controlled coat weight, thickness uniformity, and coating speed to achieve the target dry adhesive deposit weight with cross-web and machine-direction thickness variation below specifications

• Drying and Curing: The wet-coated film passes through a multi-zone drying oven where precisely profiled temperature zones progressively evaporate solvent, water, or reactive diluent carriers and initiate or complete adhesive crosslinking reactions to achieve the target adhesive modulus, tack, and peel strength at controlled residual solvent levels

• Lamination and Construction: Dried adhesive-coated film is laminated with the complementary construction element-release liner, carrier film, or second adhesive layer-in a lamination nip at controlled pressure and temperature to produce the final multi-layer adhesive film construction

• Slitting and Rewinding: Coated master rolls are slit on precision slitters to customer-specified widths using calibrated carbide or razor blade tooling, and rewound at controlled tension to produce finished rolls with uniform appearance, splice-free wind quality, and accurate width tolerances

• Die-Cutting and Sheeting:For electronics and aerospace applications, film is die-cut to precise custom shapes or sheeted to specification dimensions on flatbed or rotary die-cutting equipment for delivery in sheet formats meeting customer-specific handling and application requirements

• Quality Testing and Dispatch:Each production lot is tested for peel adhesion, tack, shear, coat weight, thickness, optical properties, and application-specific performance parameters including electrical conductivity, optical transmission, or thermal resistance before release and dispatch to electronics assembly, automotive, aerospace, and packaging customers with full certificate of analysis and REACH/RoHS compliance declaration

Industry Leadership

The global film adhesive production industry is led by established specialty chemical and advanced materials companies with extensive precision coating capabilities and strong electronics, automotive, and aerospace customer relationships. Key industry players include:

• 3M Company

• Henkel AG & Co. KGaA

• Avery Dennison Corporation

• Nitto Denko Corporation

• H.B. Fuller Company

These companies serve diverse end-use sectors including electronics and semiconductor manufacturing, automotive and electric vehicles, flexible packaging and labeling, aerospace and defense, and healthcare, medical devices and wearables, demonstrating the broad and strategically critical commercial applicability of film adhesive products across the full spectrum of global advanced manufacturing and technology applications.

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company excel in understanding its client's business priorities and delivering tailored solutions that drive meaningful outcomes. We provide a comprehensive suite of market entry and expansion services. Our offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape, and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: (+1-201971-6302)

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Film Adhesive Production Plant DPR & Unit Setup - 2026: Demand Analysis and Project Cost here

News-ID: 4456313 • Views: …

More Releases from IMARC Group

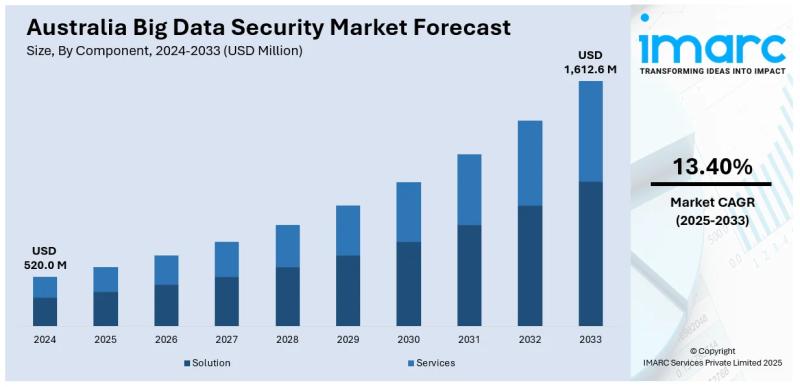

Australia Big Data Security Market Projected to Reach USD 1,612.6 Million by 203 …

Market Overview

The Australia big data security market size reached USD 520.0 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 1,612.6 Million by 2033, exhibiting a growth rate (CAGR) of 13.40% during 2025-2033. Rising cyberattacks, evolving privacy regulations, widespread cloud adoption, surging ransomware threats, stricter data breach laws, hybrid infrastructure growth, increased digital transformation, sector-specific compliance pressures, and growing demand for zero-trust frameworks across industries handling…

PLA Pellets Manufacturing Plant DPR & Unit Setup - 2026: Demand Analysis and Pro …

Setting up a PLA pellets manufacturing plant positions investors in one of the most strategically significant and rapidly expanding segments of the bio-based materials industry, backed by sustained global growth driven by the worldwide push toward sustainability, plastic waste reduction initiatives, and accelerating corporate and government adoption of biodegradable and compostable alternatives to conventional plastics. Governments along with businesses now choose biodegradable and compostable materials because of worsening environmental conditions…

Non-Woven Bag Manufacturing Plant DPR - 2026: Investment Cost, Market Growth and …

Setting up a non-woven bag manufacturing plant positions investors in one of the world's fastest-growing sustainable packaging categories - serving retail, food and beverage, corporate and promotional, events, and logistics secondary packaging markets across every major global market. Demand is driven by retail requirements for reusable carry solutions, government restrictions on thin single-use plastic carry bags, growth in organized retail and e-commerce packaging needs, increasing consumer awareness of plastic waste…

Agricultural Battery Sprayer Manufacturing Plant DPR 2026: Business Plan, Setup …

Setting up an agricultural battery sprayer manufacturing plant positions investors in one of the most dynamic and rapidly expanding segments of the agricultural equipment and precision farming value chain, backed by sustained global growth driven by the rising adoption of mechanized farming practices, increasing labor shortages in agriculture, growing focus on precision spraying, and the accelerating shift toward battery-powered and eco-friendly farm equipment. As farmers worldwide transition from manual and…

More Releases for Film

Introducing heat sealable bopp film: Cloud Film Unveils Revolutionary Heat Seala …

Qingdao Cloud Film Packaging Materials Co., Ltd., a leading innovator in the packaging industry, is thrilled to announce the launch of heat sealable bopp film, a breakthrough heat sealable BOPP film set to revolutionize flexible packaging and labeling applications globally. This exciting development represents a significant advancement in packaging technology and underscores Qingdao Cloud Film's commitment to delivering cutting-edge solutions to its customers worldwide.

In a world where packaging integrity and…

Film Marketing & Film Financing

Film Sales Agency TheMovieAgency.com is now offering extra assistance to filmmakers. If you are looking for raising funds for your next feature film or simply looking for assistance in marketing your completed feature film on the road to distribution, The Movie Agency might be able to help you with no upfront fee and no hidden fee!!!

We offer:

Free consultation.

Sourcing investors and future distributors, film buyers.

North American Distribution for the feature…

Winter Film Awards International Film Festival Returns for 10th Annual Celebrati …

New York City's Winter Film Awards showcases films from emerging filmmakers from around the world in all genres, with a special emphasis on highlighting the work of women and under-represented filmmakers. The 10th annual Festival runs September 23-October 2 in New York City. The lineup includes 91 fantastic films from 28 countries, 7 free education sessions and amazing parties.

Winter Film Awards International Film Festival, which was one of NYC's last…

Global Film Capacitors Market 2021 Applications, Leading Manufacturers, Analysis …

Syndicate Market Research recently launched a study report on the global Film Capacitors market project light on the significant drifts and vigorous cannon into the evolution of the trade, which includes the restraints, market drivers, and opportunities. The report talks about the competitive environment prevailing in the Film Capacitors market worldwide. The report lists the key players in the market and also provides insightful information about them such as their…

Biaxially Oriented Polyester (BoPET) Market Share: Key players, Application, Foc …

Biaxially Oriented Polyester (BoPET) Market report provides Six-Year forecast 2019-2025 with Overview, Classification, Industry Value, Price, Cost and Gross Profit. The prime objective of this report is to help the user understand the market in terms of its definition, segmentation, market potential, influential trends, and the challenges that the market is facing. It also covers types, enterprises and applications. To start with, analytical view to complete information of Biaxially Oriented Polyester (BoPET) market. It offers market view…

Global Polyester Film (PET Film) Market Growth 2017-2022 Mitsubishi Polyester Fi …

PET or polyethylene terephthalate film is a thermoplastic polymer commonly referred to as polyester film. Like most thermoplastics, PET films can be biaxially oriented or bubble extruded. Polyester film is one of the most common substrates used in the converting industry because of its balance of properties in relation to other thermoplastic polymers.

Ask For Sample Copy of Report : http://bit.ly/2toHtBg

This report provides detailed analysis of worldwide markets for Polyester Film…