Press release

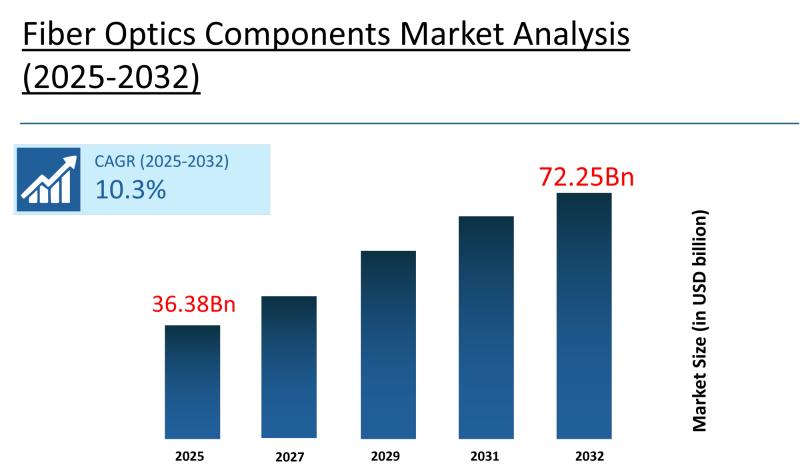

Fiber Optic Components Market to Reach USD 72.25 Billion by 2032, Says Stratview Research

Stratview Research

This driver is structurally compounding. As AI model training and inference workloads demand 400G and 800G networking speeds within hyperscale data centers, and as 5G network densification drives parallel demand for high-capacity fronthaul and backhaul infrastructure, fiber optic components - including transceivers, active optical cables, and amplifiers - become non-substitutable at every layer of the network stack. Each new data center built, each 5G cell site deployed, and each cloud region expanded adds incremental and durable demand for these components.

Stratview Research, a global market research firm, has launched a report on the global market, which provides a comprehensive outlook of the global and regional industry forecast, current & emerging market trends, segment analysis, competitive landscape, & more.

The report covers the fiber optic components market across a study period of 2019-2032, with 2024 as the base year and 2025-2032 as the forecast period. It segments the market across four dimensions - type, data rate type, application type, and region - providing demand visibility across component categories from cables and transceivers to amplifiers and circulators, and across data rate tiers from sub-10 Gbps through 100+ Gbps applications. For component manufacturers, telecom OEMs, data center operators, investors in digital infrastructure, and technology procurement teams evaluating supply chain positioning, this report delivers the structured intelligence needed to identify high-value segments and anticipate demand shifts.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4294/fiber-optic-components-market.html#form

Market Statistics

• Market size in 2024: USD 32.80 billion

• Forecast value by 2032: USD 72.25 billion

• CAGR (2025-2032): 10.3%

• Forecast period: 2025-2032

• Base year: 2024

• Total number of segments: 4

• Tables & figures: 100+

• Country-level market assessment: 20

Market Segmentation

Fiber Optic Components Market, by Type

• Cables

• Active Optical Cables

• Amplifiers

• Splitters

• Connectors

• Circulators

• Transceivers

• Others

Fiber Optic Components Market, by Data Rate Type

• Less Than 10 Gbps

• 10 Gbps to 40 Gbps

• 41 Gbps to 100 Gbps

• More Than 100 Gbps

Fiber Optic Components Market, by Application Type

• Analytical & Medical Equipment

• Communications

• Distributed Sensing

• Lighting

Fiber Optic Components Market, by Region

• North America (Country Analysis: The USA, Canada, and Mexico)

• Europe (Country Analysis: Germany, France, Italy, The UK, and Rest of Europe)

• Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

• Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others

Segment Analysis

Within the type segmentation, the Active Optical Cables (AOC) segment accounted for the largest market share in 2024. This dominance is a direct consequence of the data center industry's transition to high-density, high-speed computing environments: AOCs combine the signal integrity advantages of fiber optics - longer transmission distance, low signal loss, and immunity to electromagnetic interference - with the operational simplicity of a plug-and-play connector form factor. This combination makes them the preferred interconnect solution in hyperscale data centers and high-performance computing clusters, where rack density is increasing and copper-based solutions cannot reliably meet the bandwidth-per-watt requirements of modern AI and cloud infrastructure. For component manufacturers, the AOC segment's structural alignment with hyperscale data center investment cycles makes it the most volume-critical product category to serve over the forecast horizon.

Within the data rate type segmentation, the 10 Gbps to 40 Gbps segment is expected to be the fastest-growing during the forecast period. The driver is the ongoing network modernization cycle in enterprise and mid-tier telecom markets, where operators are upgrading legacy sub-10 Gbps infrastructure to meet rising bandwidth demand from cloud services, video streaming, and enterprise connectivity without yet requiring the investment levels associated with 100+ Gbps deployments. This segment sits at the intersection of accessibility and performance - it addresses a broad installed base of upgrade-eligible infrastructure while remaining cost-effective enough for wide-scale deployment across enterprise, regional carrier, and developing market network operators. Component suppliers with strong positioning in this speed tier are well-placed to capture the large-scale refresh cycle playing out across both mature and emerging markets.

Within the application type segmentation, the Communications segment accounted for the largest market share in 2024. This position reflects an irreducible structural reality: every unit of global data traffic - whether from 5G mobile networks, cloud computing platforms, submarine cable systems, or enterprise wide-area networks - requires fiber optic components at multiple transmission stages. The simultaneous expansion of 5G network deployment, hyperscale data center construction, and video content consumption is compounding demand across all layers of communications infrastructure. For fiber optic component suppliers, the communications segment provides the most structurally stable and highest-volume procurement channel, anchored by both telecom operator capital expenditure cycles and the continuous capacity expansions of cloud service providers including Microsoft, Amazon, and Google

Regional Insights

North America held the largest share of the fiber optic components market in 2024. The region's structural leadership is anchored by the concentration of the world's largest hyperscale data center operators - including Amazon Web Services, Microsoft Azure, and Google Cloud - whose continuous infrastructure expansion generates sustained, large-scale demand for advanced fiber optic components at all data rate tiers. The region also benefits from one of the most advanced and densely deployed 5G networks globally, supported by ongoing capital expenditure from major carriers including AT&T, Verizon, and T-Mobile, whose network densification programs require high-volume optical fronthaul and backhaul component procurement. Investments in smart city initiatives, enterprise network modernization, and government-backed broadband expansion programs further reinforce North America's position as the dominant and most structurally active region in the global fiber optic components market

Market Drivers

• Rapid global deployment of hyperscale data centers by cloud providers including Amazon, Microsoft, and Google is directly driving demand for high-speed fiber optic transceivers, active optical cables, and amplifiers, as each new data center facility requires dense optical interconnects at 400G and 800G speeds to support AI training, inference, and cloud service delivery at scale.

• 5G network rollout by major carriers across North America, Asia Pacific, and Europe requires dense optical fronthaul and backhaul infrastructure - including transceivers, splitters, and amplifiers - at every distributed antenna system and cell site, creating a sustained procurement pipeline for fiber optic components that scales directly with network densification activity.

• Drivelets-Cisco Acacia integration of 400G ZR/ZR+ optical modules into disaggregated network platforms, announced in January 2024, reflects a broader industry trend toward open optical networking that is expanding the addressable market for advanced fiber optic transceivers beyond traditional OEM-bundled deployments into independently procured optical component channels.

• Accelerating digital infrastructure investment in emerging economies - including government-backed 5G, IoT, and smart city programs across India, Southeast Asia, and Latin America - is broadening the global addressable market for fiber optic components by bringing new geographies into the high-bandwidth connectivity ecosystem and generating demand for mid-tier (10-40 Gbps) component categories.

• The AI compute build-out requiring ultra-high-density intra-data-center interconnects at 800G and beyond is creating a new product cycle for advanced optical transceiver and AOC suppliers, as GPU cluster interconnect requirements exceed what copper-based alternatives can support at the distances and densities involved in large-scale AI infrastructure deployments

Top Companies in the Market

• Lumentum

• Finisar

• Accelink Technologies

• Fujitsu Optical Components

• Broadcom

• Sumitomo Electric

• EMCORE

• Acacia Communications

• Furukawa Electric

• Oclaro

FAQs

1. What is the current size of the fiber optic components market and what is the growth outlook through 2032 ?

The fiber optic components market was valued at USD 32.80 billion in 2024 and is projected to reach USD 72.25 billion by 2032, growing at a CAGR of 10.3% during the 2025-2032 forecast period. The cumulative sales opportunity over this period is estimated at USD 421.86 billion, driven by simultaneous demand expansion from 5G deployment, hyperscale data center construction, and AI infrastructure build-out.

2. What is driving demand for fiber optic components at the industry level ?

The two primary structural drivers are surging demand for high-speed connectivity - powered by 5G, cloud computing, and AI - and the rapid global deployment of data centers requiring 400G and 800G optical interconnects. Both forces are increasing the volume of fiber optic components required per network node deployed and per data center rack installed, creating a compounding demand base across multiple end-use verticals simultaneously.

3. Which component type and data rate tier offer the strongest near-term commercial opportunity ?

The Active Optical Cables segment holds the largest current market share, driven by hyperscale data center demand for high-density, plug-and-play optical interconnects. The 10 Gbps to 40 Gbps data rate tier is the fastest-growing segment, capturing the large-scale enterprise and carrier network modernization cycle where operators are upgrading legacy infrastructure to meet rising bandwidth demand without the full capital requirements of 100+ Gbps deployments.

4. Which region leads the fiber optic components market and what structural factors underpin that leadership ?

North America held the largest market share in 2024, supported by the concentration of hyperscale cloud operators including Amazon, Microsoft, and Google, an advanced 5G network with ongoing densification investment by major carriers, and sustained government and enterprise investment in broadband and smart infrastructure. These structural advantages make North America the highest-volume and most technically demanding market for fiber optic component suppliers globally.

5. What is the key challenge constraining wider fiber optic component deployment ?

The primary technical challenge is the vulnerability of fiber optic components to physical damage and signal degradation. Their fragility under mechanical stress - from bending, installation errors, and environmental factors - combined with performance sensitivity to connector quality and dispersion effects, raises reliability concerns and lifecycle costs for large-scale, long-term network deployments, particularly in physically demanding environments such as underground infrastructure, industrial facilities, and outdoor telecommunications installations.

Related Links:

Aerospace Milled Parts Market:

https://steemit.com/aerospacemilledpartmkt/@ingnews/aerospace-milled-parts-features-and-applications

Aerospace Plates Market:

https://bresdel.com/blogs/1367740/Aerospace-Plates-Market-Growth-Opportunities-and-Strategic-Outlook

Aerospace Rolled Products Market:

https://joyrulez.com/blogs/251568/Aerospace-Rolled-Products-Market-Overview-and-Industry-Forecast-2028

Aerospace Tube Materials Market:

https://www.exoltech.net/blogs/241745/Aerospace-Tube-Materials-Market-Insights-and-Future-Prospects

Aerospace Tubes Market:

https://payrchat.com/blogs/47972/aerospace-tubes-market-stratview-research

Wind Energy Bearings Market:

https://tiktiktalk.com/blogs/45932/Future-Outlook-for-Wind-Turbine-Bearings

Energized Seals Market:

https://logcla.com/blogs/1135904/Energized-Seals-Driving-Reliability

Energy And Power Seals Market:

https://community.wongcw.com/blogs/1193708/Energy-and-Power-Seals-Market-Outlook-2025-2031

European Corrugated Pp Sheets Market:

https://www.exoltech.net/blogs/239302/European-Corrugated-PP-Sheets-Market-Set-for-Steady-Expansion

Aircraft Machining Market:

https://www.bundas24.com/blogs/203589/Aircraft-Machining-Market-Set-for-Steady-Growth-Through-2032

400 Renaissance Center, Suite 2600,

Detroit, Michigan, MI 48243

United States of America

Website: www.stratviewresearch.com

Mail Us: sales@stratviewresearch.com

Press: media@stratviewresearch.com

Stratview Research is a global market research firm that highly specializes in aerospace & defense, chemicals, and a few other industries.

It launches a limited number of reports annually on the above-mentioned specializations. Thorough analysis and accurate forecasts in this report enable the readers to take convincing business decisions.

Stratview Research has been helping companies meet their global and regional growth objectives by offering customized research services. These include market assessment, due diligence, opportunity screening, voice of customer analysis, market entry strategies, and more.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Fiber Optic Components Market to Reach USD 72.25 Billion by 2032, Says Stratview Research here

News-ID: 4456031 • Views: …

More Releases from Stratview Research

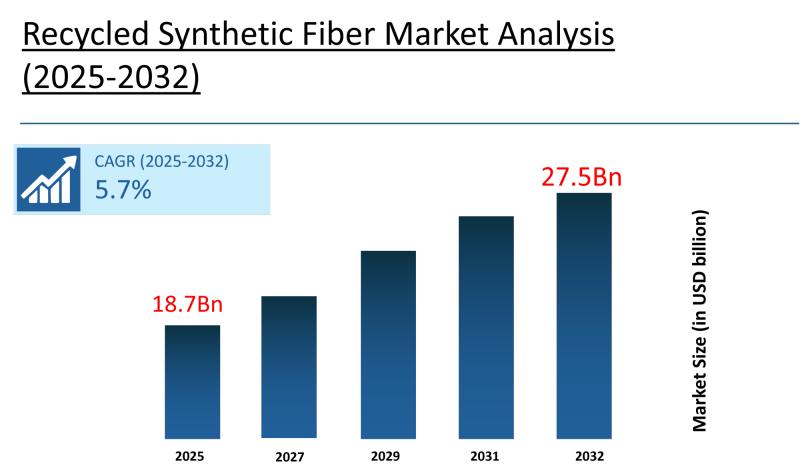

Recycled Synthetic Fiber Market to Reach USD 27.5 Billion by 2032, Says Stratvie …

The global recycled synthetic fiber market covers the recovery and reprocessing of synthetic materials - including polyester, nylon, polyolefins, and acrylics - from post-consumer waste and post-industrial into usable fibers for applications across textiles, automotive, packaging, and industrial sectors. The market pwas valued at USD 17.6 billion in 2024 and is projected to reach USD 27.5 billion by 2032, growing at a CAGR of 5.7% during the forecast period of…

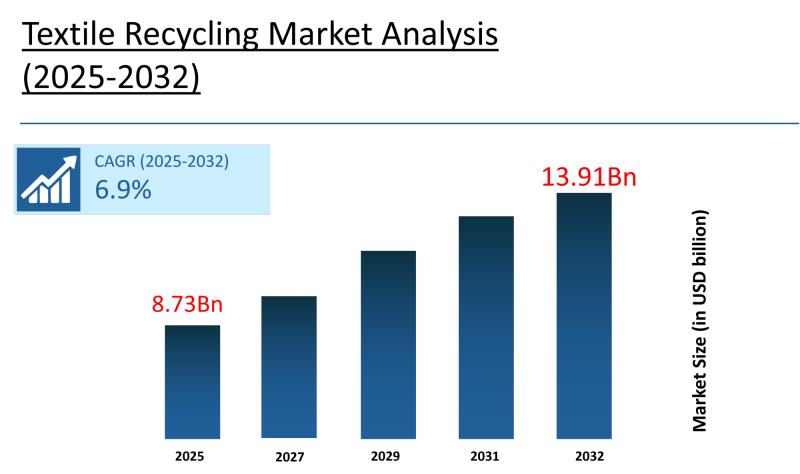

Textile Recycling Market to Reach USD 13.91 Billion by 2032, Says Stratview Rese …

The global textile recycling market encompasses the recovery of fibers, yarns, and fabrics from used clothing, manufacturing scraps, and other textile waste for reuse in new products. The market was valued at USD 8.14 billion in 2024 and is projected to reach USD 13.91 billion by 2032, growing at a CAGR of 6.9% during the forecast period of 2025-2032. The single most important growth driver is the rising global push…

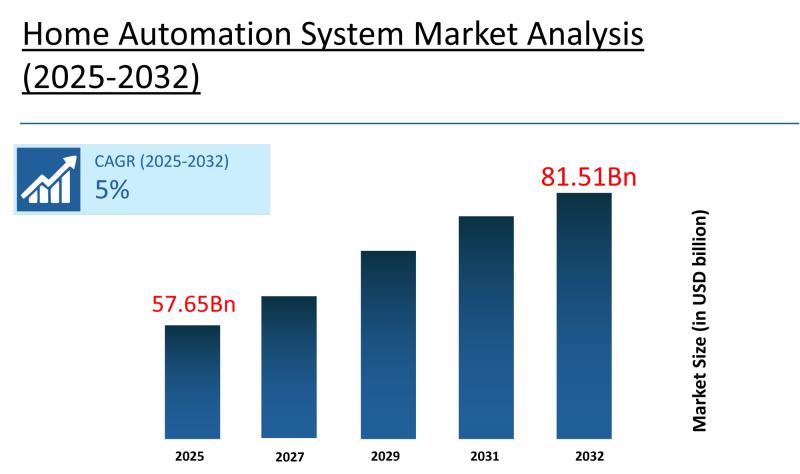

Home Automation System Market to Reach USD 81.51 Billion by 2032, Says Stratview …

The global home automation system market is a rapidly expanding industry encompassing interconnected devices that enable automated and remote control of residential functions - including lighting, heating, security, and entertainment. The market was valued at USD 54.70 billion in 2024 and is projected to reach USD 81.51 billion by 2032, growing at a CAGR of 5% during the forecast period of 2025-2032. The single most important growth driver is the…

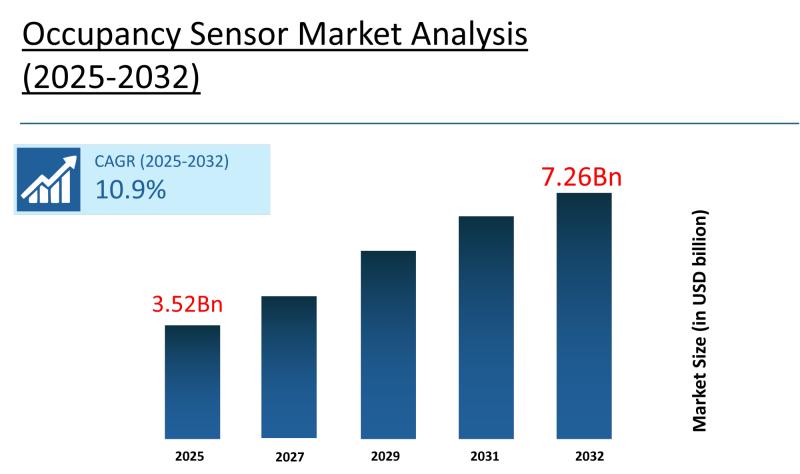

Occupancy Sensor Market to Reach USD 7.26 Billion by 2032, Says Stratview Resear …

The global occupancy sensor market was valued at USD 3.15 billion in 2024. It is projected to reach USD 7.26 billion by 2032, growing at a CAGR of 10.9% during the forecast period of 2025-2032. The single most important growth driver is the growing global demand for energy-efficient and automated building solutions - reinforced by rising energy costs and stringent sustainability regulations - which is making occupancy-based automation of lighting…

More Releases for Gbps

Japan 6G Market Growth Accelerates With Record-Breaking 1.02 Million GBPS Fiber …

Japan 6G Market reached US$ 338.1 million in 2023 and is expected to reach US$ 96.74 billion by 2031, growing with a CAGR of 102.80% during the forecast period 2024-2031.

Latest News:

✦ Japan Shatters Internet Speed Record: Achieved an unprecedented 1.02 million Gbps using next-gen optical fiber-fast enough to download 10,000 4K movies simultaneously!

✦ Breakthrough by NICT: Leveraging 19-core optical fiber and wavelength division multiplexing (WDM), researchers ensured ultra-fast, multi-channel transmission…

Network Monitoring Market Analysis by Key Players, Bandwidth (1&10 Gbps, 40 Gbps …

The network monitoring market is projected to grow from USD 2.2 billion in 2022 and is projected to reach USD 3.0 billion by 2027; it is expected to grow at a CAGR of 6.9 % from 2022 to 2027.

The rise in demand for cloud services, surging demand for resilient network monitoring systems to quickly resolve downtime issues along with need for continuous monitoring due to rise in network complexities and…

Massive Opportunities in 800 Gbps Transceiver Market 2021 to 2026

(Portland, United States): Big Market Research newly added a research report on the 800 Gbps Transceiver Market which represents a study for the period from 2021 to 2026. The research study provides a near look at the market scenario and dynamics impacting its growth. This report highlights the crucial developments along with other events happening in the market which are marking on the growth and opening doors for future growth…

Load Balancer Market Report 2018: Segmentation by Product (10 Gbps Type, 10~40 G …

Global Load Balancer market research report provides company profile for Kemp Technologies, Riverbed Technology, Sangfor, Fortinet, Barracuda, Array Networks, F5 Networks, Citrix, A10 Networks, Radware, Brocade and Others.

This market study includes data about consumer perspective, comprehensive analysis, statistics, market share, company performances (Stocks), historical analysis 2012 to 2017, market forecast 2018 to 2025 in terms of volume, revenue, YOY growth rate, and CAGR for the year 2018 to 2025,…

Advantech and 6WIND Pack 80 Gbps Throughput into Packetarium™

6WINDGate™ multi-core packet processing software maximizes performance on Advantech’s scalable Packetarium™ network processor platform

Advantech and 6WIND today announced the availability of the latest 6WINDGate™ multi-core packet processing software on Advantech’s award-winning Packetarium™ NCP-7560 network processor platform. Based on Cavium's 12-core OCTEON® Plus network processor, the NCP-7560 represents the high performance end of the Packetarium™ product line. It integrates up to eight powerful, multi-core Packetarium™ network processing boards for…

LeaseWeb Increases Bandwidth on Hosting Network from 500 to 750 Gbps

Amsterdam, June 23, 2009 – LeaseWeb (leaseweb.com), one of Europe’s largest business hosting providers based in Amsterdam, has in a six-month period increased the bandwidth capacity of its hosting network from 500 to 750 Gigabits per second. A large increase in new clients, and especially the increased use of videos on websites, are key drivers behind the strong growth in Internet traffic.

LeaseWeb’s clients use LeaseWeb’s hosting network as well…