Press release

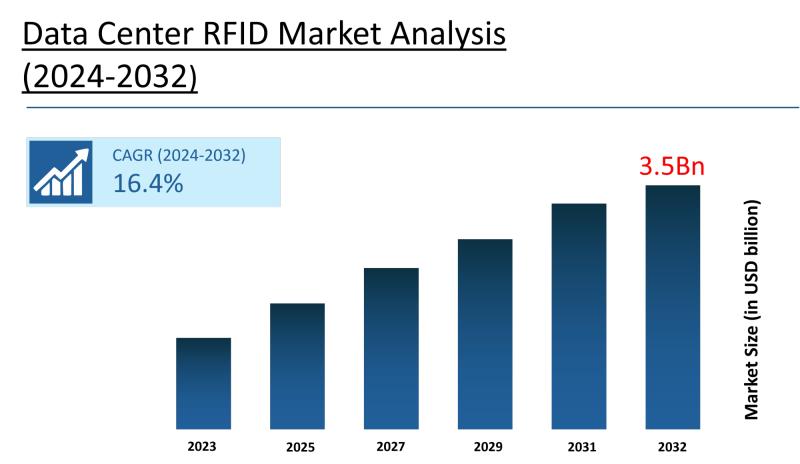

Data Center RFID Market to Reach US$ 3.5 Billion by 2032, Says Stratview Research

Stratview Research

The single most important structural growth driver is the rapid expansion of hyperscale and colocation data center facilities, which is compounding the complexity of asset management at a scale that renders manual tracking operationally untenable. As data centers grow to house tens of thousands of individual infrastructure components across dense, multi-zone environments, the demand for automated inventory control, audit readiness, and real-time visibility becomes a non-negotiable operational requirement rather than an optional efficiency improvement. The data center RFID market is projected to grow at a CAGR of 16.4% through 2032, driven by hyperscale infrastructure expansion, rising compliance mandates, and the integration of RFID with data center infrastructure management (DCIM) and building management systems (BMS) platforms.

Stratview Research, a global market research firm, has launched a report on the global market, which provides a comprehensive outlook of the global and regional industry forecast, current & emerging market trends, segment analysis, competitive landscape, & more.

The report covers the data center RFID market across six segmentation dimensions - application type, tag type, reader type, frequency type, data center type, and region - with country-level analysis across 20 markets. It provides actionable intelligence on dominant and fastest-growing segments, the competitive landscape among leading RFID hardware and platform providers, and the technology and regulatory forces reshaping procurement and deployment strategies. For RFID manufacturers, data center operators, technology integrators, investors, and strategy teams, the report delivers the market intelligence necessary to evaluate product development priorities, regional expansion decisions, and partnership opportunities with precision.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4595/data-center-rfid-market.html#form

Market Statistics

• Market Size (2023): US$ 1.0 billion

• Forecast Value (2032): US$ 3.5 billion

• CAGR: 16.4%

• Forecast Period: 2024-2032

• Base Year: 2023

• Total Number of Segments: 6

• Tables & Figures: 100+

• Country-Level Market Assessment: 20

Market Segmentation

Data Center RFID Market, by Application Type IT Asset & Infrastructure Tracking, Security Access & Compliance Management, and Environmental & Operational Monitoring

Data Center RFID Market, by Tag Type Passive Tag, Semi-Passive Tag, and Active Tag

Data Center RFID Market, by Reader Type Fixed Reader and Handheld Reader

Data Center RFID Market, by Frequency Type Low Frequency, High Frequency, and Ultra High Frequency

Data Center RFID Market, by Data Center Type Hyperscale, Colocation, Enterprise, and Edge

Data Center RFID Market, by Region North America (The USA, Canada, and Mexico), Europe (The UK, Germany, France, and Rest of Europe), Asia-Pacific (China, Australia, Japan, India, and Rest of Asia-Pacific), and Rest of the World (Brazil, Africa, and Others)

Segment Analysis

Within the application type segmentation, IT Asset and Infrastructure Tracking leads the data center RFID market as the dominant application, anchored by its role in providing automated inventory controls, lifecycle management tools, and auditable records across both hyperscale and colocation facilities. As infrastructure complexity scales, manual tracking introduces unacceptable error rates and audit exposure, making automated RFID-based asset management a procurement necessity rather than an operational luxury.

Environmental and Operational Monitoring is the fastest-growing application segment, propelled by the proliferation of sensor-enabled RFID tags capable of delivering real-time temperature, humidity, and vibration data in high-density computing environments - capabilities that directly support predictive maintenance programs and reduce unplanned downtime risk. Security Access and Compliance Management grows steadily in parallel, driven by RFID-based access control integration and the audit trail requirements of frameworks such as SOC 2 and ISO 27001. For RFID solution providers, the fastest near-term product development and revenue growth opportunity lies in delivering integrated environmental monitoring solutions that combine asset tracking with condition sensing in a single deployment architecture.

In the tag type segmentation, passive tags hold the largest market share, driven by their combination of low per-unit cost, battery-free operation, long service life, and compatibility with standardized EPC Gen2 protocols that enable cost-effective large-scale deployment across servers, racks, and cables. Their sufficient read ranges for the majority of inventory and zone-level tracking applications make them the default choice for bulk asset tagging in both new builds and retrofit deployments. Active tags are the fastest-growing segment, reflecting the rising operational demand for real-time location tracking and sensor-enabled environmental monitoring at extended read ranges - capabilities that passive tags alone cannot deliver in large, complex data hall environments. Semi-passive tags occupy a niche position, offering battery-assisted sensing with reader-dependent communication, suitable for specialized applications requiring environmental sensing without full active-tag power overhead. For tag manufacturers, investment in active tag product lines with integrated sensor capabilities represents the segment with the highest unit value and fastest volume growth trajectory through 2032.

Fixed readers constitute the dominant reader type in the data center RFID market, installed at facility entry points, cage boundaries, aisle positions, and storage areas to enable continuous automated asset tracking, movement detection, and integration with access control and audit systems. Their architectural role as the backbone of zone-level visibility and compliance documentation makes them a standard component in any meaningful RFID deployment. Handheld readers are the fastest-growing segment, driven by the practical requirements of periodic manual audits, exception investigations, distributed site management, and field operations in enterprise, colocation, and edge environments where full fixed-reader coverage is not economically justifiable for every location. Their ability to enable rapid bulk scanning and real-time database synchronization without requiring permanent infrastructure investment is accelerating adoption across operators managing multiple facilities or locations with variable asset density. For reader manufacturers, the growing base of distributed edge and enterprise facilities represents a particularly high-growth channel for handheld reader solutions that prioritize portability, software integration, and ease of use.

Within the frequency type segmentation, Ultra-High Frequency systems hold both the dominant share and the highest growth rate in the data center RFID market - a dual position grounded in UHF's technical superiority for large-scale data center applications. UHF delivers the longest read ranges, the fastest multi-tag simultaneous scanning speeds, and the broadest compatibility with low-cost passive tag manufacturing, making it the optimal frequency for zone-level inventory monitoring and bulk asset tracking across large data halls. Its alignment with global EPC Gen2 standardization further reduces tag production costs and simplifies cross-vendor deployments, enabling cost-effective rollouts at the scale hyperscale and large colocation facilities require.

High Frequency occupies a niche position in applications requiring short-range precision reading or access control integration, while Low Frequency remains the smallest segment, confined to legacy or specialty applications with inherently limited read ranges. For suppliers and system integrators, UHF-based product portfolios and deployment expertise represent the broadest and most commercially durable market opportunity.

Colocation facilities currently drive substantial RFID adoption across the data center type segmentation, reflecting the multi-tenant asset segregation imperatives, SLA compliance tracking requirements, and automated inventory audit needs that are structurally inherent to the colocation business model. When multiple customers' assets coexist within shared physical infrastructure, accurate, automated, and continuously auditable asset visibility is both a contractual obligation and a competitive differentiator. Hyperscale data centers are the fastest-growing segment, propelled by the massive scale of infrastructure requiring full automation, high-speed bulk scanning, real-time location visibility, and integration with advanced deployment and DCIM systems. Enterprise data centers are progressively adopting RFID to meet audit requirements and lifecycle management efficiency targets, while edge facilities represent an emerging high-growth subsegment where RFID enables remote asset visibility and management of distributed sites where on-site staffing and manual control are constrained. For RFID solution providers, hyperscale contract volumes represent the highest-growth revenue opportunity, while colocation channels offer the most structurally recurring and compliance-driven demand base.

Regional Insights

North America leads the global data center RFID market and is expected to maintain its dominant position through 2032. The region's leadership is built on the world's highest concentration of hyperscale data center facilities - with the United States anchoring the largest installed base of large-scale computing infrastructure globally - combined with mature colocation ecosystems, advanced DCIM platform adoption, and stringent compliance environments that create structural and non-discretionary demand for automated asset management. The region benefits from early and deep technology sector maturity, continuous data center modernization and replacement cycles, and the presence of leading RFID hardware and platform providers actively investing in AI-enabled asset analytics and integrated DCIM solutions. These factors collectively reinforce North America's structural advantage in both current deployment volumes and ongoing procurement activity across all data center types.

Asia-Pacific is the fastest-growing regional market for data center RFID and is expected to sustain that momentum through the forecast period. The primary growth drivers are aggressive digital transformation programs, rapidly expanding data center construction capacity, and data localization policies that are compelling enterprises and hyperscalers to build substantial in-region infrastructure across China, India, Japan, and emerging Southeast Asian markets. China's data localization regulatory framework is directly driving large-scale domestic data center investment with corresponding RFID adoption requirements. Japan's operational discipline and high infrastructure quality standards are supporting systematic RFID integration in new and modernized facilities. India's rapidly expanding hyperscale capacity is generating a growing base of new data center deployments that require automated asset management from initial commissioning. For RFID manufacturers and solution providers, Asia-Pacific represents the highest-priority regional expansion opportunity over the forecast horizon.

Market Drivers

• Hyperscale and colocation facility expansion increasing asset management complexity beyond manual control thresholds: As hyperscale operators including major cloud providers continue to build out large-scale data centers housing tens of thousands of individual servers, racks, and networking components, the operational impossibility of accurate manual tracking is driving systematic procurement of RFID-based automated inventory, lifecycle management, and audit systems.

• SOC 2, ISO 27001, and related compliance frameworks mandating automated asset audit trails: Regulatory and industry compliance requirements that govern data center operations - including SOC 2 Type II certification processes and ISO 27001 information security management standards - impose documentation and audit trail requirements for IT asset movement, access, and lifecycle events that RFID systems satisfy more reliably, cost-effectively, and continuously than manual processes.

• Integration of RFID with DCIM and BMS platforms enabling predictive maintenance and real-time operational intelligence: Technology investments by leading RFID providers - including Impinj's partnership with ServiceNow to integrate RAIN RFID directly into IT Asset Management workflows, and Honeywell's acquisition of AssetPulse Technologies to combine asset tracking with environmental sensing - are extending RFID value beyond basic inventory into predictive maintenance and operational resilience applications that justify broader facility-wide deployments.

• Zebra Technologies' acquisition of RF Controls and AI-enabled reader product development accelerating centimeter-level location visibility: Zebra Technologies' November 2024 acquisition of RF Controls - combining RFID with ultra-wideband positioning for centimeter-level asset tracking - and the launch of its FX9600 fixed RFID reader with integrated AI edge processing represent product capability advances that expand RFID applicability into high-precision location use cases that previously required separate and more expensive technology stacks.

• Edge data center proliferation creating distributed asset management requirements that mandate remote RFID monitoring: The growing deployment of edge data centers across geographically distributed locations - where on-site staffing is limited or impractical - is generating demand for RFID systems that enable remote real-time asset visibility, automated exception detection, and inventory management without requiring physical on-site auditing, expanding the addressable RFID market well beyond traditional centralized facility deployments.

Top Companies in the Market

• Avery Dennison Corporation

• Impinj, Inc.

• Zebra Technologies Corporation

• Honeywell International Inc.

• HID Global Corporation

• Eaton Corporation Plc.

• Fujitsu Limited

• Invengo Information Technology Co., Ltd.

• RF Code, Inc.

• NXP Semiconductors N.V.

FAQs

1. How large is the data center RFID market today and what is the growth trajectory through 2032?

The global data center RFID market was valued at US$ 1.0 billion in 2023 and is projected to reach US$ 3.5 billion by 2032, growing at a CAGR of 16.4% over the 2024-2032 forecast period. Growth is driven by hyperscale and colocation infrastructure expansion, rising compliance audit requirements, and the progressive integration of RFID with DCIM and predictive maintenance platforms.

2. What is the primary business case driving data center operators to invest in RFID systems?

The primary business case is the operational impossibility of maintaining accurate, auditable, real-time asset visibility through manual processes as data center infrastructure scales to tens of thousands of individual components. RFID eliminates the human error, labor cost, and audit exposure associated with manual inventory management while simultaneously generating the continuous documentation trails required by compliance frameworks such as SOC 2 and ISO 27001.

3. Which RFID segment - passive, semi-passive, or active tags - offers the best near-term growth opportunity for tag manufacturers?

Active tags represent the highest near-term growth opportunity, driven by rising demand for real-time location tracking and sensor-enabled environmental monitoring capabilities that passive tags cannot deliver at the read ranges required in large data halls. The combination of longer read ranges, programmable sensor integration, and the expansion of environmental monitoring as the fastest-growing application segment positions active tags as the highest unit-value and fastest-volume-growth category for tag manufacturers through 2032.

4. How are hyperscale data center operators approaching RFID procurement differently from enterprise customers? Hyperscale operators prioritize high-speed bulk scanning, full-facility automation, and deep integration with advanced DCIM and deployment management systems - procurement decisions driven by the need to manage infrastructure at a scale and velocity that enterprise customers rarely encounter. Enterprise and colocation customers place greater emphasis on cost-effectiveness, audit trail generation, and compliance documentation, with handheld readers and modular deployments representing more common entry points than the comprehensive fixed-reader architectures typical of hyperscale implementations.

5. What are the supply-chain and investment implications of the consolidation trend among leading RFID vendors? Strategic acquisitions - including Zebra Technologies' purchase of RF Controls for ultra-wideband RFID positioning, Honeywell's acquisition of AssetPulse Technologies for sensor-integrated tracking, and Impinj's platform partnership with ServiceNow - are raising the integration complexity and technology breadth that data center operators expect from RFID vendors. This consolidation trend is compressing the competitive space for standalone point-solution providers while simultaneously creating stronger barriers to entry, signaling that scale, platform integration capability, and software ecosystem partnerships are becoming the primary competitive differentiators in the data center RFID market.

Related Links:

Glass Ionomer Filling Market:

https://community.wongcw.com/blogs/1157553/Growing-Dental-Care-Demand-Fuels-Expansion-of-the-Glass-Ionomer

Recreational Pressure Vessels Market:

https://www.friend007.com/read-blog/274312

Reinforced Compounds Market:

https://www.bundas24.com/blogs/190011/Rising-Industrial-Demand-Boosts-Reinforced-Compounds-Market

Restoration Anchors Market:

https://webyourself.eu/blogs/1689758/Restoration-Anchors-Market-Forecast-Key-Insights

Epdm Waterproofing Market:

https://joyrulez.com/blogs/214915/Strong-Infrastructure-Development-to-Fuel-EPDM-Waterproofing-Growth

Automotive Airbag Yarn Market:

https://joyrulez.com/blogs/233652/Automotive-Airbag-Yarn-Market-Insights

Automotive Ducts Market:

https://bresdel.com/blogs/1290493/Automotive-Ducts-Market-Opportunities-Emerging-Through-2030

Automotive Engineered Coated Fabric Market:

https://zekond.com/read-blog/229722

Aircraft Composite Blades Market:

https://payrchat.com/blogs/43748/aircraft-composite-blades-market-stratview-research

Aircraft Decorative Laminates Market:

https://tiktiktalk.com/blogs/49137/Aviation-Decorative-Laminates-Market-Positioned-for-Steady-Growth

400 Renaissance Center, Suite 2600,

Detroit, Michigan, MI 48243

United States of America

Website: www.stratviewresearch.com

Mail Us: sales@stratviewresearch.com

Press: media@stratviewresearch.com

Stratview Research is a global market research firm that highly specializes in aerospace & defense, chemicals, and a few other industries.

It launches a limited number of reports annually on the above-mentioned specializations. Thorough analysis and accurate forecasts in this report enable the readers to take convincing business decisions.

Stratview Research has been helping companies meet their global and regional growth objectives by offering customized research services. These include market assessment, due diligence, opportunity screening, voice of customer analysis, market entry strategies, and more.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Data Center RFID Market to Reach US$ 3.5 Billion by 2032, Says Stratview Research here

News-ID: 4446477 • Views: …

More Releases from Stratview Research

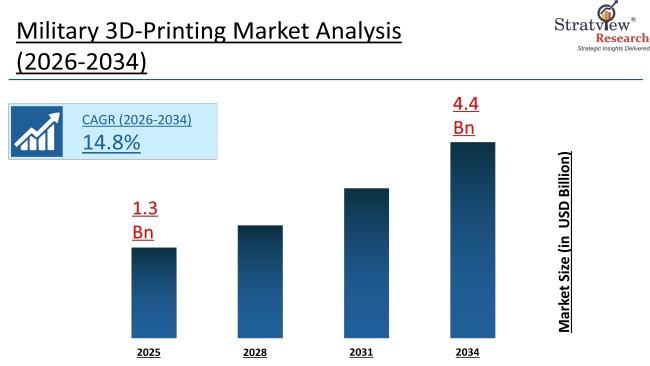

Military 3D Printing Market to Reach USD 4.4 Billion by 2034, says Stratview Res …

The military 3D printing market is expected to reach USD 4.4 billion by 2034, growing at a CAGR of 14.8% during the forecast period of 2026-2034. The market stood at USD 1.3 billion in 2025 and is projected to reach USD 1.4 billion in 2026, reflecting a year-over-year growth of 15.3%.

The primary growth driver is the increasing adoption of additive manufacturing by defense organizations for on-demand production and logistics optimization.…

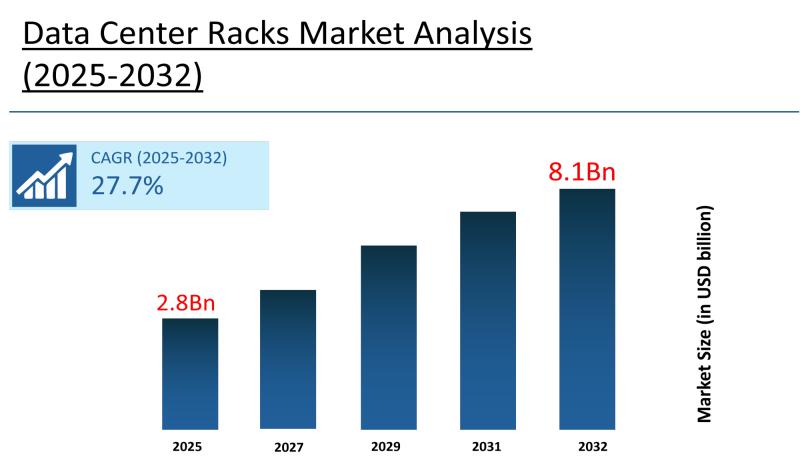

Data Center Rack Market to Reach USD 11.2 Billion by 2032, Says Stratview Resear …

The global data center rack market encompasses standardized metal cabinets and enclosures designed to securely house and organize IT infrastructure - including servers, storage systems, and networking equipment - while optimizing power distribution, cooling efficiency, and scalability within data center environments. The market was valued at USD 5.1 billion in 2025 and is projected to reach USD 11.2 billion by 2032, expanding at a CAGR of 11.7% over the 2026-2032…

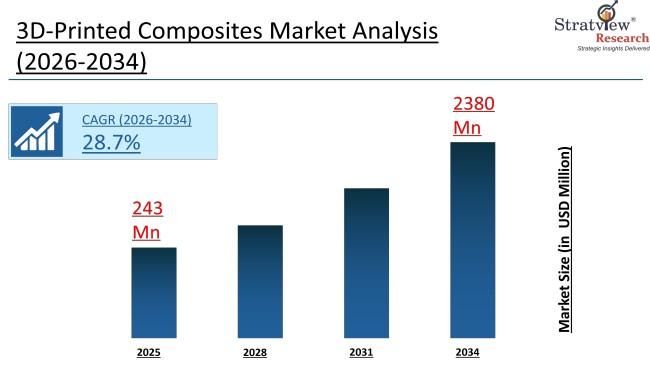

3D-Printed Composites Market to Reach USD 2380 Million by 2034, says Stratview R …

The 3D-printed composites market is expected to reach USD 2380 million by 2034, growing at a CAGR of 28.7% during the forecast period of 2026-2034. The market was valued at USD 243 million in 2025 and is projected to reach USD 317 million in 2026, reflecting a year-over-year growth of 30.4%.

The most critical growth driver is the increasing demand for lightweight and high-performance materials across advanced industries. This structurally boosts…

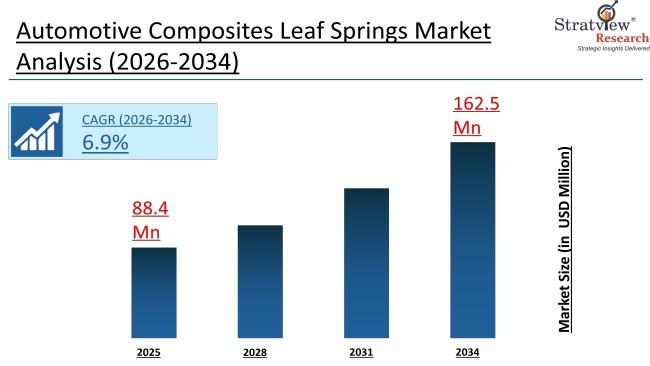

Automotive Composite Leaf Springs Market to Reach USD 162.5 Million by 2034, say …

The automotive composite leaf springs market is expected to reach USD 162.5 million by 2034, growing at a CAGR of 6.9% during the forecast period of 2026-2034. The market recorded annual demand of USD 88.4 million in 2025 and is projected to reach USD 95.3 million in 2026, reflecting a year-over-year growth of 7.8%.

The most significant growth driver is the rising production of commercial vehicles, particularly light commercial vehicles (LCVs).…

More Releases for RFID

RFID Tags For Asset Tracking Market Exceptional Business Performance | Vizinex R …

As the global economy recovers in 2021 and the supply of the industrial chain improves, the RFID Tags For Asset Tracking market will undergo major changes. The latest research shows that the RFID Tags For Asset Tracking industry market size will be million US dollars in 2021, and will grow to million US dollars in 2028, with an average annual growth rate of %.

The global RFID Tags For Asset Tracking…

RFID Readers Market Growth by 2027 | Fixed RFID Readers, Integrated RFID Readers …

Future Market Insights (FMI) has published a new research report titled “Radio Frequency Identification (RFID) Readers Market: Global Industry Analysis (2012-2016) and Opportunity Assessment (2017-2027).” The report states that the growing penetration of advanced technology along with increasing supply chain complexities are encouraging consumers to adopt RFID technology. Owing to this, players operating in the RFID readers market are incessantly upgrading their product portfolios in order to meet the demands…

Global RFID Tag Chips Market by Type, HF RFID Chip, UHF RFID Chip, LF RFID Chip, …

This study report Global RFID Tag Chips Market, the analyst provides growth estimates, forecasts, and an in-depth analysis of all key factors at play in the Market. The report takes into account the micro and macro factors that are likely to impact the growth trajectory of the Market. The study further presents details on the investments initiated by several organizations, institutions, government, and non-government bodies.

The report investigates and analyzes the…

RFID Equipment Market - The Rising Application of RFID In Healthcare RFID Techno …

The applications of Radio Frequency Identification (RFID) have widened in the healthcare industry, ranging from tracking medical equipment, patient identification and blood transfer monitoring to tracking the path of medication from pharmacy to the patient. Due to this, the RFID equipment market has witnessed a high growth rate over the years.

Providing clients with in-depth analysis and competitive intelligence, the research report evaluates the RFID equipment market and all…

RFID Tag Chip Market: By Applications - HF RFID Tags, UHF RFID Tags, LF RFID Tag …

Latest industry research report on: Global and United States RFID Tag Chip Market | Industry Size, Share, Research, Reviews, Analysis, Strategies, Demand, Growth, Segmentation, Parameters, Forecasts

Request For Sample Report @ https://www.marketresearchreports.biz/sample/sample/1227953

This report studies the RFID Tag Chip market status and outlook of global and United States, from angles of players, regions, product types and end industries; this report analyzes the top players in global and United States market, and splits…

rfid clear tag for rfid inventory (gyrfidstore)

RFID Disc Tags are widely used for inventory tracking system or Automatic production systems. The RFID Disc Tag can also work on metal surface with anti-metal layer on it, also can be attached to goods surface by adhesive layer. There are abundant size options from 12mm to 50mm. GYRFID presents several types with different material and size to suitable customer’s application.

DIP Series- PVC Disc Tag, PVC Laminated, thickness of 1.0-1.2mm

DIT…