Press release

Data Center AI Servers Market to Reach US$ 196.8 Billion by 2032, Says Stratview Research

Stratview Research

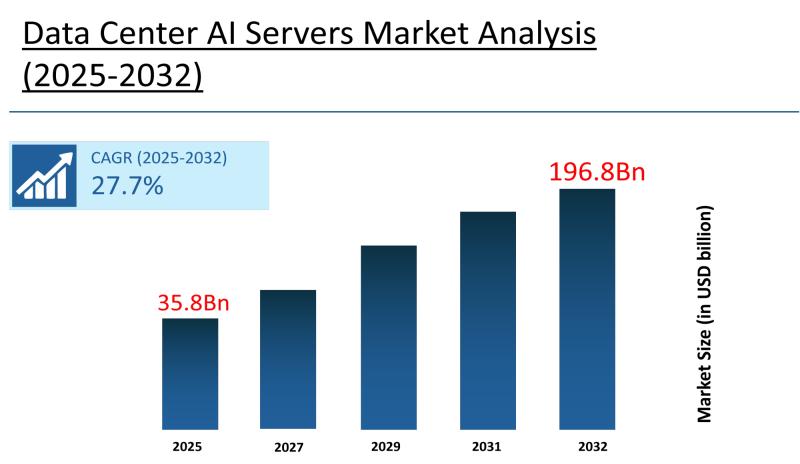

The single most important growth driver is the rapid and broad-based adoption of artificial intelligence across industries. Enterprises are deploying AI for automation, predictive analytics, customer personalization, and operational optimization - all of which require dedicated high-performance computing infrastructure. The surge in generative AI workloads, including large language models and recommendation engines, is compounding this demand by requiring immense computational power and low-latency processing that only purpose-built AI servers can reliably provide. The data center AI servers market is projected to grow at a CAGR of 27.7% from 2025 to 2032, driven by generative AI adoption, hyperscale data center expansion, and enterprise digital transformation.

Stratview Research, a global market research firm, has launched a report on the global market, which provides a comprehensive outlook of the global and regional industry forecast, current & emerging market trends, segment analysis, competitive landscape, & more.

The report covers the data center AI servers market across five segmentation categories - form factor type, GPU count type, cooling architecture type, data center type, and region - with granular country-level analysis across 20 markets. It provides actionable intelligence on the dominant and fastest-growing segments, competitive dynamics among more than 25 global players, and the technology and investment trends reshaping AI infrastructure procurement. For server manufacturers, cloud providers, data center operators, investors, and business development teams, the report delivers the strategic foundation necessary to evaluate market entry, capacity expansion, or technology partnership decisions.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4596/data-center-ai-servers-market.html#form

Market Statistics

• Market Size (2025): US$ 35.8 billion

• Forecast Value (2032): US$ 196.8 billion

• CAGR: 27.7%

• Forecast Period: 2025-2032

• Base Year: 2025

• Total Number of Segments: 5

• Tables & Figures: 100+

• Country-Level Market Assessment: 20

Market Segmentation

Data Center AI Servers Market, by Form Factor Type Rack Servers, Blade Servers, and Tower Servers

Data Center AI Servers Market, by GPU Count Type 1-2 GPUs, 2-4 GPUs, and 4-8 GPUs

Data Center AI Servers Market, by Cooling Architecture Type Air Cooling and Liquid Cooling

Data Center AI Servers Market, by Data Center Type Hyperscale, Colocation, Enterprise, and Edge

Data Center AI Servers Market, by Region North America (The USA, Canada, and Mexico), Europe (The UK, Germany, France, and Rest of Europe), Asia-Pacific (China, Australia, Japan, India, and Rest of Asia-Pacific), and Rest of the World (Brazil, Africa, and Others)

Segment Analysis

Within the form factor segmentation, rack servers dominate the data center AI servers market and are expected to maintain their leading position throughout the forecast period. Their dominance is structurally grounded in their superior scalability, modular design, and capacity to support high-power-density GPU configurations with advanced thermal management. Unlike blade servers - which face meaningful thermal constraints when handling high-end GPU setups - or tower servers, which lack the modularity required for multi-GPU configurations, rack servers can be seamlessly upgraded and integrated with PCIe expansion cards to accommodate evolving AI workload demands. For server manufacturers and data center operators, rack-optimized AI server product lines represent the most commercially critical investment category for the foreseeable future.

In the GPU count segmentation, servers equipped with 4-8 GPUs currently account for the largest share of the market. These configurations deliver the computational throughput required for intensive AI model training and large-scale inference at hyperscale and enterprise data centers, striking a balance between performance, scalability, and power efficiency that smaller configurations cannot match for complex AI workloads. At the same time, servers with 2-4 GPUs are projected to grow at a faster rate during the forecast period, as enterprise AI adoption expands into a broader range of use cases where full 4-8 GPU density is unnecessary. Organizations pursuing incremental AI scaling strategies - particularly those in early or mid-stage adoption - are gravitating toward 2-4 GPU configurations as cost-effective entry points. For suppliers, the fastest near-term volume growth opportunity lies in serving this mid-tier GPU count segment as enterprise AI deployments proliferate.

On the cooling architecture dimension, air cooling currently holds the dominant share of AI server deployments, primarily because it is compatible with the installed base of existing data center infrastructure and requires no fundamental facility redesign. However, liquid cooling is anticipated to grow at a faster rate over the forecast period. As AI workloads drive GPU counts and rack power densities to levels that air cooling systems struggle to manage effectively, liquid cooling is becoming an operational necessity rather than a premium option. Data center operators and server OEMs investing in liquid-cooled AI server product development and facility retrofitting will be best positioned to capture the growing high-density AI deployment wave.

Across data center types, colocation facilities currently hold a significant share of AI server deployments, as enterprises prefer outsourcing high-performance infrastructure to third-party providers that offer scalable power, cooling, and connectivity without requiring in-house data center construction. Hyperscale data centers, however, are the fastest-growing segment, propelled by cloud providers rapidly expanding AI computing capacity to support generative AI, large language models, and other large-scale workloads. Enterprise data centers continue to adopt AI servers at a more measured pace for internal analytics and application development, while edge data centers are gradually emerging to support low-latency inferencing closer to end users. For AI server manufacturers, hyperscale contract volumes represent the highest-growth revenue opportunity through 2032, but enterprise and colocation channels offer durable and diversified demand.

Regional Insights

North America leads the global data center AI servers market and is expected to maintain its dominant position through 2032. The region's leadership is built on a combination of the world's most advanced cloud ecosystem, early and deep enterprise AI adoption, and the highest concentration of hyperscale data center investment globally. Major technology companies - including those operating the world's largest cloud platforms - are actively expanding AI-ready facilities to support generative AI, advanced analytics, and machine learning workloads at scale. Strong research and development capabilities, a dense enterprise digital transformation pipeline, and continuous innovation in AI hardware and software architectures collectively reinforce North America's structural advantage in attracting AI server deployment at the highest volumes and highest specifications globally.

Asia-Pacific is the fastest-growing regional market for data center AI servers and is expected to sustain that trajectory throughout the forecast period. Countries including China, Japan, and India are witnessing accelerated adoption of AI-driven applications, supported by government-backed technology initiatives, rapidly expanding cloud deployments, and surging internet penetration. Large-scale data center construction programs across the region are creating a sustained and high-volume demand for AI-optimized server infrastructure. The combination of digitally transforming enterprises, rising demand for real-time analytics, and national AI competitiveness programs is generating procurement momentum that is expected to grow faster than any other region through 2032, making Asia-Pacific the highest-priority expansion target for AI server manufacturers and suppliers seeking next-cycle growth.

Market Drivers

• Broad-based enterprise AI adoption across industries: Enterprises across sectors including finance, healthcare, manufacturing, and retail are deploying AI for automation, predictive analytics, and personalization at scale - each use case requiring dedicated high-performance AI server infrastructure that CPUs alone cannot support.

• Generative AI and large language model deployment by major cloud providers: Hyperscale cloud providers including those operating large-scale AI platforms are investing aggressively in AI server capacity to power large language models, recommendation engines, and multimodal AI applications, creating sustained and high-volume OEM procurement demand for GPU-dense server configurations.

• Government-backed AI and digital infrastructure programs in key growth markets: National AI strategies in countries such as China, India, Japan, and the United States are directing capital toward AI-ready data center infrastructure, incentivizing both domestic deployment and foreign investment in AI server capacity within their respective markets.

• Rising power and thermal density requirements driving liquid cooling infrastructure upgrades: As GPU-dense AI servers push rack power densities beyond what conventional air cooling can handle, data center operators are investing in liquid-cooled infrastructure - compelling both facility upgrades and new server procurement cycles that replace legacy air-cooled configurations with thermally optimized AI server systems.

• Strategic acquisitions and technology partnerships among major server OEMs: Significant M&A activity - including Hewlett Packard Enterprise's US$ 14 billion acquisition of Juniper Networks and Cisco's US$ 28 billion acquisition of Splunk - is enabling leading server manufacturers to deliver integrated AI data center solutions that span compute, networking, and infrastructure management, raising competitive barriers and accelerating enterprise procurement of full-stack AI server environments.

Top Companies in the Market

• Dell Technologies

• Hewlett Packard Enterprise

• Inspur Systems

• Super Micro Computer, Inc.

• Lenovo Group Limited

• Cisco Systems, Inc.

• International Business Machines Corporation (IBM)

• GIGA-BYTE Technology Co., Ltd.

• Quanta Cloud Technology

• Wiwynn Corporation

FAQs

1. How large is the data center AI servers market today and what is the growth outlook through 2032?

The global data center AI servers market was valued at US$ 35.8 billion in 2025 and is projected to reach approximately US$ 196.8 billion by 2032, growing at a CAGR of 27.7%. This growth is driven by widespread enterprise AI adoption, generative AI infrastructure buildout by cloud providers, and large-scale data center expansion programs across North America and Asia-Pacific.

2. What is driving such aggressive investment in AI server infrastructure by cloud providers and hyperscalers? Hyperscale cloud providers are scaling AI server capacity at an unprecedented rate to support generative AI applications, large language models, and real-time analytics workloads that require massive parallel processing power. The competitive pressure to deliver AI-enabled cloud services - and the recurring revenue those services generate - is creating a structurally sustained procurement cycle for GPU-dense AI servers that is expected to persist through the forecast horizon.

3. Which data center and server configuration segments offer the highest near-term growth opportunity for suppliers? Hyperscale data centers are the fastest-growing demand segment for AI server deployments, while 2-4 GPU server configurations are projected to grow at the highest rate within the GPU count segmentation as enterprise AI adoption broadens. Liquid cooling solutions represent an additional high-growth adjacency, as rising power densities at AI-focused facilities increasingly exceed the thermal limits of conventional air-cooled infrastructure.

4. What are the supply-chain and investment implications of the shift toward liquid-cooled AI server infrastructure?

The transition toward liquid cooling is compelling both data center operators and server OEMs to redesign infrastructure procurement strategies - operators are retrofitting or purpose-building liquid-cooled facilities, while manufacturers are developing liquid-cooled product lines optimized for high-density GPU configurations. Suppliers that fail to offer validated liquid-cooled AI server options risk being excluded from the fastest-growing hyperscale procurement cycles over the next several years.

5. How consolidated is the data center AI servers market and what does the competitive landscape mean for new entrants? The market is moderately consolidated, with more than 25 players competing globally on the basis of product portfolio breadth, GPU configuration options, regional manufacturing presence, and ecosystem partnerships. Leading players are reinforcing competitive positions through large-scale acquisitions and technology partnerships - raising the integration complexity and capital requirements that new entrants must match to compete credibly in the hyperscale and enterprise segments.

Related Links:

Hoses Market:

https://payrchat.com/blogs/20480/hoses-market

Resin Flooring Market:

https://heyhey.icu/blogs/567113/Resin-Flooring-Market-Overview-Growth-Trends-and-Future-Opportunities

Uhmwpe Fiber Market:

https://ayema.ng/blogs/243427/Weaving-New-Possibilities-Emerging-Opportunities-in-the-UHMWPE-Fiber-Market

Waterproofing Coatings Market:

https://www.retailandwholesalebuyer.com/read-blog/34908

Wire Rope Market:

https://tiktiktalk.com/blogs/46591/Durability-Meets-Innovation-The-Evolving-Landscape-of-the-Wire-Rope

Facade Anchors Market:

https://www.wowonder.xyz/read-blog/388567

Indian Aerospace Composites Market:

https://ivebo.co.uk/read-blog/138427

Marine Bearings Market:

https://logcla.com/blogs/917552/Marine-Bearings-Market-Ensuring-Reliability-at-Sea

Flash Chromatography Market:

https://thebizbar.com/blogs/104270/Flash-Chromatography-Solutions-Market

Machine Tool Bearings Market:

https://www.retailandwholesalebuyer.com/preview/future-opportunities-in-the-machine-tool-bearings-market

400 Renaissance Center, Suite 2600,

Detroit, Michigan, MI 48243

United States of America

Website: www.stratviewresearch.com

Mail Us: sales@stratviewresearch.com

Press: media@stratviewresearch.com

Stratview Research is a global market research firm that highly specializes in aerospace & defense, chemicals, and a few other industries.

It launches a limited number of reports annually on the above-mentioned specializations. Thorough analysis and accurate forecasts in this report enable the readers to take convincing business decisions.

Stratview Research has been helping companies meet their global and regional growth objectives by offering customized research services. These include market assessment, due diligence, opportunity screening, voice of customer analysis, market entry strategies, and more.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Data Center AI Servers Market to Reach US$ 196.8 Billion by 2032, Says Stratview Research here

News-ID: 4446451 • Views: …

More Releases from Stratview Research

Air-Cooled Heat Exchangers Market to Reach USD 5.1 Billion by 2030, Says Stratvi …

The air-cooled heat exchangers market includes systems that directly cool or condense process fluids using ambient air instead of water. According to Stratview Research, the market is expected to reach USD 5.1 billion by 2030, growing at a CAGR of 5.2% during 2025-2030. A key growth driver is the increasing adoption of water-free industrial cooling systems, as air-cooled heat exchangers help reduce water dependency while supporting demanding power generation, petrochemical,…

Space Launch Vehicle Services Market to Reach USD 18.0 Billion by 2030, Says Str …

The space launch vehicle services market covers the operations and processes required to transport payloads such as satellites, spacecraft, cargo spacecraft, human spacecraft, and scientific instruments into space using launch vehicles or rockets. According to Stratview Research, the space launch vehicle services market was valued at USD 9.6 billion in 2024 and is expected to reach USD 18.0 billion by 2030, growing at a CAGR of 10.6% during 2025-2030. The…

Rail Composites Market to Reach USD 1.64 Billion by 2028, Says Stratview Researc …

The rail composites market includes composite materials used in rail equipment, including train exteriors, interiors, structural elements, and related components. According to Stratview Research, the rail composites market was estimated at USD 1.25 billion in 2022 and is likely to grow at a CAGR of 4.6% during 2023-2028 to reach USD 1.64 billion in 2028. The most important growth driver is the rising use of composites for lightweighting, as composite…

Data Center Networking Equipment Market to Reach USD 74.0 Billion by 2032, Says …

The data center networking equipment market includes devices such as switches, servers, routers & gateways, security appliances, load balancers, cables, and other networking components that enable communication between servers and IT infrastructure inside data centers. According to Stratview Research, the market was valued at USD 24.3 billion in 2024 and is projected to reach USD 74.0 billion by 2032, growing at a CAGR of 14.9% during 2025-2032. The most important…

More Releases for GPU

Ai GPU Rental Strengthens Cloud GPU Rental Access as Global AI Infrastructure De …

Singapore - April 2026 - As artificial intelligence continues to reshape the global digital economy, Ai GPU Rental is expanding access to Cloud GPU Rental and AI Compute services, giving users a more practical and scalable way to participate in the fast-growing infrastructure market.

The value of computing power is rising quickly as demand for AI Infrastructure, GPU Rental, and On-Demand GPU services expands across industries. From machine learning and automation…

Ai GPU Rental Strengthens Cloud GPU Rental Access as Global AI Infrastructure De …

Singapore - April 2026 - As artificial intelligence continues to reshape the global digital economy, Ai GPU Rental is expanding access to Cloud GPU Rental and AI Compute services, giving users a more practical and scalable way to participate in the fast-growing infrastructure market.

The value of computing power is rising quickly as demand for AI Infrastructure, GPU Rental, and On-Demand GPU services expands across industries. From machine learning and automation…

Revolutionizing GPU Cooling: Tone Cooling Technology Co., Ltd Unveils High-Perfo …

Tone Cooling Technology Co., Ltd., a leading innovator in thermal solutions, proudly announces the launch of its next-generation Custom GPU Cold Plates, purpose-built to redefine high-performance computing. These state-of-the-art cooling components deliver unmatched heat dissipation, precision customization, and whisper-quiet operation, positioning Tone Cooling Technology as the go-to China manufacturer for GPU cold plates.

Designed with modern demands, these cold plates offer tailored solutions for gamers, PC builders, and data center professionals…

Borg Media Launches GPUPrices.ai, a Breakout GPU Comparison Tool Showing GPU Pri …

Innovative, detail-rich platform transforms how gamers, PC builders, and tech enthusiasts research and compare graphics cards

PORTLAND, Ore. - February 17, 2025 - Borg Media LLC today announced the launch of GPUPrices.ai [https://gpuprices.ai/]. This innovative, detail-rich GPU comparison tool transforms how gamers, PC builders, and tech enthusiasts research and compare graphics cards by showing GPU prices in real time. The site aggregates data from multiple sources, including top retailers, review sites,…

Nvidia Market Share in AI GPU Chips & Global GPU Market: Growth, Trends, and Fut …

The global 𝐆𝐫𝐚𝐩𝐡𝐢𝐜𝐬 𝐏𝐫𝐨𝐜𝐞𝐬𝐬𝐢𝐧𝐠 𝐔𝐧𝐢𝐭 (𝐆𝐏𝐔) 𝐦𝐚𝐫𝐤𝐞𝐭 has been experiencing significant growth over the past decade, primarily driven by advances in artificial intelligence (AI), machine learning, data science, and high-performance computing (HPC). A major contributor to this surge is Nvidia Corporation, a leader in the production of AI-powered GPUs that dominate the AI and data center segments. Nvidia's innovative AI GPU chips are reshaping industries, from gaming and autonomous vehicles…

Global Graphic Processing Units (GPU) Market linked to Innovations and Developme …

As per a new market research report launched by Inkwood Research, the Global Graphic Processing Units (GPU) Market is anticipated to reach $169.82 billion by 2028, rising with a CAGR of 33.32% over the forecasting years.

Browse 53 market data Tables and 48 Figures spread over 226 Pages, along with in-depth analysis on Global Graphic Processing Units (GPU) Market by Type, Device, End-User Industry, and by Geography

This insightful market research report…