Press release

Australia Plasterboard Market Projected to Reach USD 1,833.9 Million by 2034

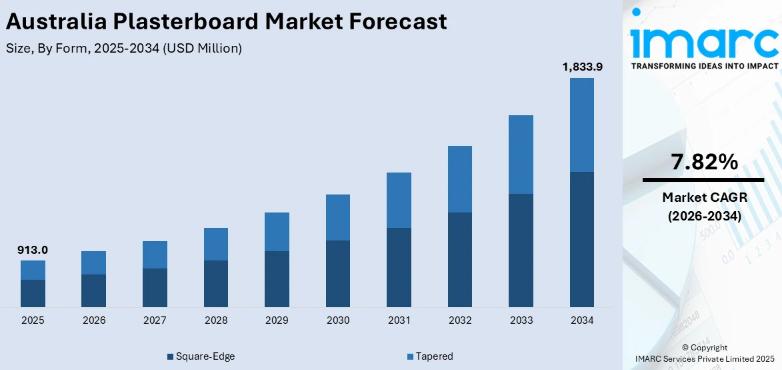

The Australia Plasterboard Market reached a size of USD 913.0 Million in 2025 and is projected to reach USD 1,833.9 Million by 2034, growing at a CAGR of 7.82% during the forecast period of 2026-2034. The market is driven by strong building activity, increased focus on sustainability, technological innovations producing superior products with enhanced fire resistance and sound insulation, and growing demand for environmentally responsible plasterboard products incorporating recycled materials and improved indoor air quality characteristics. Australia's National Housing Accord target of 1.2 million new homes by 2029 - alongside sustained commercial construction activity in healthcare, education, and office refurbishment across Sydney, Melbourne, Brisbane, and Perth - is creating a decade-long pipeline of plasterboard demand at a scale that both domestic and international manufacturers are investing heavily to serve. Etex closed its acquisition of BGC's plasterboard and fibre cement businesses on 1st March 2024, including BGC's 56,000 square metre plasterboard plant in Perth and a network of nine warehouses across Australia and New Zealand - expanding Etex's Australian presence to 24 sites and almost 600 teammates with leading brands including Siniat plasterboards, Promat fire protection, and EQUITONE fibre cement cladding. This acquisition - combined with Etex's existing three gypsum wallboard plants in New South Wales, Queensland and Victoria - positions Etex as Australia's largest plasterboard manufacturer alongside CSR Gyprock (now part of Saint-Gobain following its AUD 4.3 billion acquisition), Knauf, and USG Boral. Australia's bushfire, cyclone, and flood exposure is structurally strengthening demand for fire-resistant, moisture-resistant, and impact-resistant plasterboard types that satisfy progressively tighter building code specifications across high-risk zones. Dwelling commencements increased by 4.6% to 43,247 as of September 2024 - confirming the residential construction recovery that underpins the near-term plasterboard demand pipeline. New South Wales and ACT lead regionally through Sydney's housing density pipeline and commercial construction concentration.

https://www.imarcgroup.com/australia-plasterboard-market

How AI is Reshaping the Future of the Australia Plasterboard Market:

• AI-powered building information modelling (BIM) platforms - used by major Australian construction companies including Lendlease, Multiplex, John Holland, and BESIX Watpac - are using machine learning to optimise plasterboard layout, waste minimisation, and prefabrication sequencing across large commercial projects, generating quantified material savings of 8-15% versus traditional cut-and-fit installation methods and enabling precise pre-ordering that reduces on-site storage requirements and delivery frequency.

• Etex Australia's Opt2Act carbon-neutral program - the only manufacturer of plasterboard and metal systems in Australia to offer an opt-in carbon neutral program for a range of its Siniat products - is supported by AI-powered supply chain carbon accounting tools that calculate the embodied carbon footprint of individual product orders and automatically match the purchase with certified carbon offset projects, enabling builders, developers, and specifiers to meet Green Star and NABERS embodied carbon requirements with verified data that is progressively required under Australia's evolving sustainability reporting standards.

• AI-driven quality control systems deployed at Etex's Siniat manufacturing plants and CSR's Gyprock facilities use computer vision and machine learning to detect surface defects, thickness variations, and edge quality deviations on plasterboard sheets at production line speeds that far exceed the detection capability of human visual inspection - improving the consistency of product quality delivered to Australian building sites and reducing the waste and rework costs generated when substandard boards reach installation stage.

• Smart building sensor technologies - increasingly embedded within plasterboard systems by manufacturers including Etex and Knauf for commercial fit-out and health facility applications - use IoT sensors integrated into wall cavities to monitor temperature, humidity, and air quality in real time, with AI analytics platforms processing the sensor data to detect early signs of moisture ingress, condensation risk, and indoor air quality deterioration before they cause structural damage or occupant health impacts that require costly remediation.

• CSR Gyprock implemented a 9.8% price increase across its full Gyprock plasterboard range in February 2024 - while Knauf applied a 9.5% increase across all plasterboard and compounds in March 2024 - with AI-powered cost modelling and dynamic pricing analytics enabling plasterboard manufacturers to calibrate price increases against raw material cost movements, competitor positioning, and demand elasticity at the product-category and regional-market level with a precision that manual pricing processes cannot match in an environment of high raw material cost volatility.

Request Industry-Focused Sample with Insights & Forecasts: https://www.imarcgroup.com/australia-plasterboard-market/requestsample

Market Trends and Insights

• Market Consolidation Reshaping Competitive Dynamics: France-based Saint-Gobain submitted a non-binding indicative offer of USD 5.44 billion for building materials producer CSR - which was subsequently accepted - bringing CSR Gyprock, Australia's most recognized plasterboard brand with the highest installed base among Australian plasterers and builders, under Saint-Gobain's global building materials ownership, while Etex's BGC acquisition simultaneously expanded the Belgian manufacturer's Australian footprint to 24 sites, creating a market structure dominated by two major international building materials conglomerates alongside Knauf and USG Boral.

• National Housing Accord Driving Sustained Residential Demand: Australia's National Housing Accord target of 1.2 million new homes by 2029 - with state governments committing funding for social housing, planning reforms to accelerate approvals, and infrastructure investment to unlock greenfield development - creates a seven-year pipeline of residential plasterboard demand that, even at below-target delivery rates, represents a material structural uplift from the pre-Accord residential construction baseline, supporting plasterboard manufacturers' confidence in Australian capacity investment.

• Specialty Plasterboard Capturing Growing Share of Total Market: The accelerating mandatory adoption of fire-resistant, moisture-resistant, and acoustic plasterboard - driven by the National Construction Code's progressive strengthening of performance requirements in response to Australia's natural disaster exposure, apartment densification, and healthcare facility expansion - is shifting Australia's plasterboard mix toward higher-value specialty grades that command price premiums of 15-40% over standard plasterboard and generate superior margins for both manufacturers and trade distributors.

• Sustainability Credentials Becoming Procurement Differentiator: Green Star, NABERS, and the emerging Whole of Life Carbon Disclosure requirements under Australia's updated Sustainability Reporting Standards are creating measurable procurement preference for low-embodied-carbon plasterboard products - with Etex's Opt2Act carbon-neutral Siniat products, recycled-content plasterboard ranges, and Environmental Product Declarations (EPDs) becoming commercially significant procurement criteria for government buildings, commercial developers, and institutional construction clients that must demonstrate embodied carbon management in their project sustainability reporting.

• Price Inflation Reshaping Value Chain Economics: Multiple plasterboard manufacturers implemented significant price increases across 2024 - including CSR Gyprock at 9.8%, Knauf at 9.5%, and Etex Siniat at 5.3% - reflecting gypsum raw material cost pressures, energy cost increases in manufacturing, and freight cost inflation, with the cumulative price escalation over 2022-2024 materially increasing the total plasterboard cost component in residential and commercial construction budgets and driving builder interest in waste minimisation, optimised specification, and value engineering that reduces plasterboard volume without compromising performance.

Standard plasterboard is the dominant type by volume - used for the majority of interior wall and ceiling linings across residential and standard commercial construction - while fire-resistant plasterboard is the fastest-growing type through progressively tightening building code requirements for bushfire attack level compliance, apartment boundary wall separation, and commercial building fire compartmentation. Moisture-resistant plasterboard is a large and growing type driven by the expansion of medium- and high-density residential development where bathroom, kitchen, and laundry wet area specifications require moisture-resistant lining. Sound-resistant plasterboard is growing rapidly through the apartment density trend where acoustic performance between dwellings is a primary National Construction Code compliance requirement and a significant quality-of-life driver for residents. Thermal insulated plasterboard is growing through the energy efficiency requirements of the NCC 2022's Section J energy performance standards. Impact-resistant plasterboard serves healthcare, education, and commercial applications where wall durability is a maintenance cost driver. By form, tapered-edge dominates for jointed wall and ceiling systems while square-edge serves cornice and tile-backing applications. By end-use sector, residential leads by volume while non-residential generates higher revenue per square metre through specialty product specifications. Regionally, New South Wales leads through Sydney's housing density pipeline, with Queensland the fastest-growing regional market through South East Queensland's infrastructure-driven construction boom.

Market Growth Drivers

Residential Housing Sector Expansion

Australia's residential housing construction pipeline - anchored by the National Housing Accord's 1.2 million new dwellings target, federal and state social housing investment programs, and the structural undersupply of housing relative to population growth driven by record net overseas migration of 400,000+ annually - is the primary volume driver of plasterboard demand throughout the forecast period of 2026-2034. Dwelling commencements increased by 4.6% to 43,247 as of September 2024 - confirming the recovery trajectory from the 2023 trough - with the ABS recording rising private sector house building approvals that signal a strengthening pipeline of residential projects where plasterboard remains the dominant interior wall and ceiling lining material in Australian residential construction across all dwelling types from detached houses to high-rise apartments. The ongoing urbanization of Sydney, Melbourne, Brisbane, and Perth continues to drive the medium- and high-density apartment development formats that generate proportionally higher plasterboard consumption per project than low-density housing through the specification of fire-rated, acoustic, and moisture-resistant specialty plasterboard required by both the National Construction Code and modern apartment buyer expectations for privacy, amenity, and safety.

Growing Commercial Infrastructure Development

The booming commercial construction sector - encompassing the AUD 60 billion+ health infrastructure pipeline including Sydney's Westmead Health Precinct, Melbourne's Footscray Hospital, and Queensland's new hospitals program, alongside the education infrastructure investment driven by university campus expansions and state government school building programs - is generating sustained demand for specialty plasterboard products including fire-rated, acoustic, and moisture-resistant grades that commercial specifications mandate at levels significantly above residential construction requirements. Major Australian cities including Brisbane, Perth, and Melbourne are experiencing rising investment in commercial property driven by infrastructure spending, urban renewal, and the office refurbishment activity driven by hybrid working's influence on workspace quality expectations - with these projects requiring plasterboard products with enhanced acoustic performance, fire rating compliance, and sustainability credentials to satisfy both tenant requirements and Green Star design objectives. The hospitality and tourism sector recovery - driving hotel refurbishments, resort developments in Queensland and Western Australia, and entertainment facility upgrades - represents an additional commercial plasterboard demand driver that complements the dominant healthcare and education infrastructure construction pipeline.

Impact of Natural Disasters and Regulatory Standards

Australia's escalating natural disaster exposure - with bushfire attack level zoning progressively expanding, cyclone-rated construction requirements extending southward, and flood-resilient building specifications strengthening following the 2022 Queensland and NSW floods - is creating mandatory specification of fire-resistant, impact-resistant, and moisture-resistant plasterboard across an expanding proportion of Australia's total construction geography that was previously served by standard plasterboard. The National Construction Code 2022's strengthened energy efficiency requirements, increased acoustic performance standards for apartment buildings, and expanded moisture management requirements for wet areas are simultaneously raising the minimum plasterboard specification baseline across residential construction - with NCC 2022's full adoption across all states and territories through 2023-2025 creating a permanent structural uplift in specialty plasterboard's share of total market volume. Rebuilding activity following natural disasters - cyclones in Queensland and Western Australia, floods in NSW and Victoria, and bushfire reconstruction in South Australia and Victoria - generates recurring plasterboard demand spikes in affected regions where the heightened awareness of disaster risk drives specification of higher-performance plasterboard products even where not strictly mandated by code.

Market Segmentation

Form Insights:

• Square-Edge

• Tapered

Type Insights:

• Standard Plasterboard

• Fire-Resistant Plasterboard

• Thermal Insulated Plasterboard

• Moisture-Resistant Plasterboard

• Sound-Resistant Plasterboard

• Impact-Resistant Plasterboard

End-Use Sector Insights:

• Residential

• Non-Residential

Regional Insights:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Recent News and Developments

• March 2024: Etex closed its acquisition of BGC's plasterboard and fibre cement businesses, including BGC's 56,000 square metre Perth plasterboard plant and nine warehouses across Australia and New Zealand, expanding Etex's Australian presence to 24 sites and almost 600 employees with leading brands Siniat, Promat, and EQUITONE - with the acquired BGC businesses having reported AUD 155 million in full-year 2023 sales, making this the most significant Australian plasterboard manufacturing acquisition in over a decade.

• February 2024: CSR Gyprock implemented a 9.8% price increase across its full plasterboard range including cornice profiles, Supatone and Freshtone tiles, with wet compounds increasing 9.2%, dry compounds 11.2%, and Rigitone and Gyptone ceiling tiles 11% - reflecting the cumulative raw material, energy, and logistics cost pressures that have driven material price increases across the entire Australian building materials supply chain and are incentivising construction industry investment in plasterboard waste reduction technology and optimised specification.

• March 2024: Knauf Plasterboard implemented a 9.5% price increase across all plasterboard, plasterboard tiles, cornice, compounds, stud adhesive, and plasters - alongside a 4% increase on mineral fibre ceiling tiles - confirming the broad-based inflationary pricing environment across Australia's plasterboard supply market that is reshaping builder cost modelling and driving value engineering reviews of plasterboard specification across both residential and commercial construction projects.

• 2024: Saint-Gobain completed its AUD 4.3 billion acquisition of CSR Limited - bringing CSR Gyprock, Australia's most widely distributed plasterboard brand across the Dulux, Bunnings, and trade distribution networks, under Saint-Gobain's global building materials ownership - creating a market structure where the two largest Australian plasterboard manufacturers are now subsidiaries of major European building materials multinationals with deep R&D capability and sustainability investment capacity that will progressively elevate the technical performance bar for Australian plasterboard products.

• 2024: The National Construction Code 2022 achieved full adoption across all Australian states and territories - with strengthened energy efficiency performance requirements under Section J, expanded acoustic standards for apartment boundary walls, and updated moisture management requirements for wet areas - creating a permanent upward shift in specialty plasterboard specification requirements across the total Australian construction market that will sustain premium-grade plasterboard's growing share of total volume through the entire forecast period.

• October 2023: Etex signed the agreement with BGC to acquire its gypsum and fibre cement divisions - including the gypsum wallboard facility in Perth - with Etex CEO Bernard Delvaux stating the deal represented a strategic opportunity to complement the company's gypsum footprint in Australia, targeting long-term market growth driven by an increasing population and strong penetration of plasterboard and fibre cement sidings, providing the strategic rationale for sustained manufacturing investment in Australian production capacity.

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

Ask analyst for your customized sample:

https://www.imarcgroup.com/request?type=report&id=37342&flag=F

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC's offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Plasterboard Market Projected to Reach USD 1,833.9 Million by 2034 here

News-ID: 4431309 • Views: …

More Releases from IMARC Group

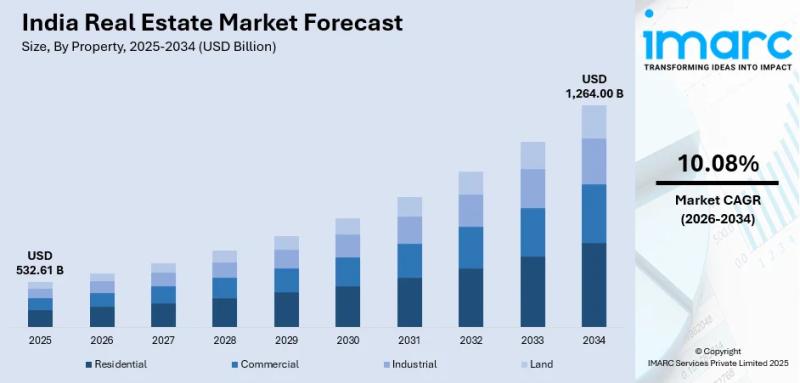

India Real Estate Market to Hit $1,264.00 Bn by 2034 Fueled by Urbanization & In …

How is India Real Estate Market Performing?

India's real estate industry is navigating an exceptionally high-growth and structurally transformative phase, driven by rapid urbanization creating sustained demand for residential and commercial spaces, rising disposable incomes enabling homeownership aspirations across a broadening consumer base, a young demographic fueling unprecedented demand for housing and workspaces, and a regulatory environment that has progressively enhanced transparency and investor confidence across the sector. As India's economy…

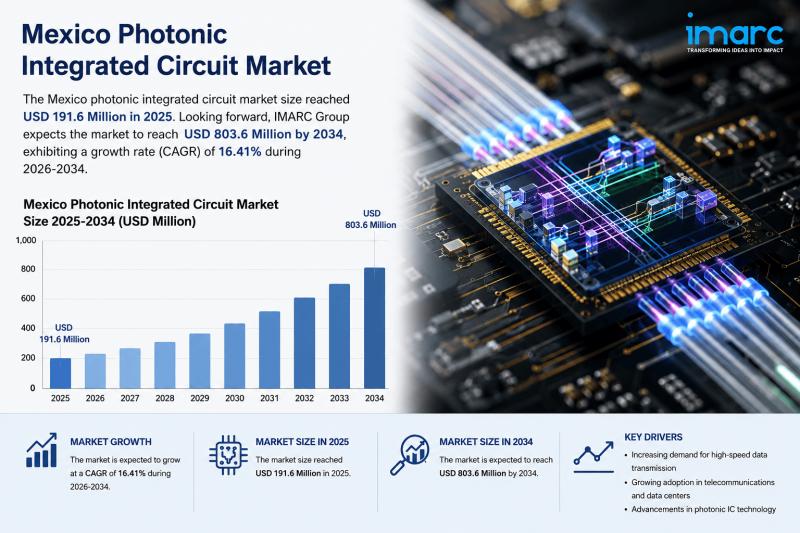

Mexico Photonic Integrated Circuit Market Set to Reach USD 803.6 Million by 2034

The Mexico photonic integrated circuit (PIC) market reached USD 191.6 Million in 2025 and is projected to reach USD 803.6 Million by 2034, growing at a CAGR of 16.41% during 2026-2034, according to IMARC Group. Photonic integrated circuits microchips that use photons rather than electrons as their primary information carrier deliver dramatically higher data transmission speeds, lower energy consumption, and superior bandwidth density compared to conventional electronic circuits, making them…

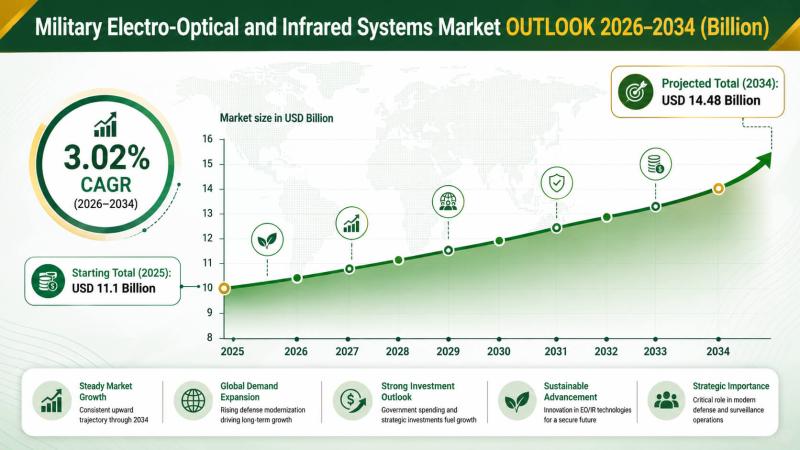

Military Electro-Optical and Infrared Systems Market to Surpass USD 14.48 Billio …

According to a research report by IMARC Group, the global military electro-optical and infrared systems market size was valued at USD 11.1 Billion in 2025. The market is projected to reach USD 14.48 Billion by 2034, exhibiting a growth rate (CAGR) of 3.02% during 2026-2034. North America currently dominates the market, holding a significant market share of 32% in 2025. The market is primarily driven by rising geopolitical tensions, increasing…

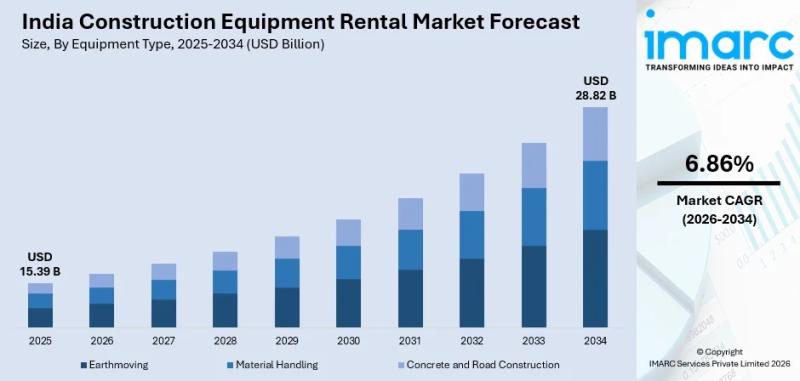

India Construction Equipment Rental Market Report 2026-2034: Size, Demand, Growt …

How Is India's Construction Equipment Rental Market Performing?

India's construction equipment rental market stands as a pivotal enabler of the nation's infrastructure ambitions, supporting rapid urbanization, large-scale project execution, and cost-efficient construction delivery. The market was valued at USD 15.39 Billion in 2025 and is projected to reach USD 28.82 Billion by 2034, growing at a CAGR of 6.86% during 2026-2034.

The growth is driven by rising labor costs compelling contractors to…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…