Press release

Rectified Spirit Production Cost DPR 2026: Unit Setup, CapEx/OpEx Analysis with Profitability Forecast

As governments across the world accelerate ethanol blending mandates to reduce fossil fuel dependence and carbon emissions, healthcare infrastructure expands across developing nations, and consumer demand for alcohol-based personal care and hygiene products grows, the rectified spirit industry continues to present compelling opportunities for manufacturers and investors seeking long-term profitability in a high-volume, regulation-supported, and diversified end-use chemicals segment. Asia Pacific currently leads the global market, accounting for 39.8% of total market share, reflecting the region's dominant molasses and sugarcane feedstock base, large-scale distillery infrastructure, and the strength of Indian and Southeast Asian government ethanol blending programmes.

Market Overview and Potential Growth:

The global rectified spirit market demonstrates a robust and broad-based growth trajectory driven by multiple high-volume demand segments across alcoholic beverages, pharmaceuticals, chemicals, personal care, and biofuel.

The market is primarily propelled by the extensive utilisation of rectified spirit as a foundational alcohol input across these industries, the global expansion of government-mandated ethanol blending programmes, rising healthcare infrastructure investment in developing nations creating incremental pharmaceutical-grade ethanol demand, and the sustained consumption of ethanol-based sanitisers and disinfectants that gained lasting market traction following the COVID-19 pandemic. According to IMARC Group's comprehensive market analysis, Asia Pacific holds the largest regional share at 39.8%, reflecting the scale and strategic importance of India, China, and Southeast Asian distillery industries within the global rectified spirit supply landscape.

Request Sample: https://www.imarcgroup.com/rectified-spirit-manufacturing-plant-project-report/requestsample

Rectified spirit, also known as neutral spirit, is a highly concentrated and purified ethanol solution containing approximately 95% ethanol by volume. It is produced through multiple rounds of distillation applied to fermented substrates including molasses, sugarcane juice, grains, and other plant-based carbohydrate materials. The resulting product's high purity and chemically neutral character make it indispensable across a broad spectrum of end-use applications. In beverages, it serves as the base alcohol for spirits production and blending. In pharmaceuticals, it meets the stringent purity standards required for medicinal formulations, syrups, and antiseptics. In industry, it functions as a versatile solvent, feedstock for downstream chemical synthesis, and input for personal care and cosmetic formulations. Rectified spirit presents as a colourless, volatile, and flammable liquid, with quality specifications varying according to the regulatory and technical requirements of each application sector.

The market for rectified spirit is growing steadily across all primary demand segments. The global initiative to blend ethanol with transportation fuel, particularly in carbon-reduction-focused regions across Asia, the Americas, and Europe, represents one of the most significant structural demand drivers for the industrial alcohol sector.

Rising alcohol consumption across developing economies in Asia and Africa is driving sustained beverage industry offtake, while the parallel development of healthcare infrastructure in these regions is generating incremental demand for pharmaceutical and medical-grade rectified spirit.

For instance, according to OECD data, average health spending across OECD countries reached approximately USD 6,000 per person in 2024, reflecting the scale of investment in healthcare systems globally and the corresponding demand for high-purity pharmaceutical inputs including rectified spirit for medicinal formulations, surgical antiseptics, and hospital-grade disinfectants. Furthermore, the lasting adoption of ethanol-based sanitisers established during the COVID-19 pandemic has maintained elevated demand for industrial-grade rectified spirit in personal hygiene and institutional sanitation applications well beyond the acute phase of the health crisis.

Plant Capacity and Production Scale:

The proposed rectified spirit production facility is designed with an annual production capacity ranging between 10-30 million Litres, enabling meaningful economies of scale while maintaining the operational flexibility required to serve a multi-sector and geographically diverse customer base. This capacity range positions producers to supply alcoholic beverage manufacturers requiring consistent base spirit volumes, pharmaceutical companies demanding high-purity ethanol grades, chemical industry customers utilising rectified spirit as a synthesis feedstock, personal care and cosmetics producers requiring solvent-grade alcohol, and biofuel blending programmes operated by government or private petroleum sector entities-ensuring diversified and resilient revenue streams across multiple end-use industries that collectively provide strong and sustained demand throughout the business cycle.

Speak to an Analyst: https://www.imarcgroup.com/request?type=report&id=8504&flag=C

Financial Viability and Profitability Analysis:

The rectified spirit production business demonstrates healthy profitability potential under normal operating conditions, supported by the product's multi-sector demand profile, the scale efficiencies achievable in large-volume distillery operations, and the diverse revenue opportunities available across beverage, pharmaceutical, industrial, and biofuel market segments. The financial projections reveal gross profit margins in the range of 25-35% and net profit margins of 12-20%, reflecting the cost structure of a feedstock-intensive production process balanced against the pricing premiums achievable across pharmaceutical and high-purity specialty alcohol grades.

• Gross Profit: 25-35%

• Net Profit: 12-20%

These margins are supported by stable and growing multi-sector demand from beverage manufacturers, pharmaceutical formulators, chemical producers, personal care companies, and ethanol blending programme operators; the volume economics of large-scale continuous distillation operations that enable competitive unit production costs through feedstock efficiency, energy recovery, and co-product valorisation; and the critical and non-substitutable role of rectified spirit as the foundational alcohol input across liquor production, medicinal formulations, industrial solvent applications, sanitiser manufacturing, perfumery, and fuel ethanol blending. The project demonstrates strong return on investment potential with comprehensive financial modelling covering phased capital deployment, production capacity ramp-up, multi-year income and expenditure trajectories, and payback period analysis.

Cost of Setting Up a Rectified Spirit Production Plant:

Operating Cost Structure:

Understanding the operating expenditure (OpEx) structure is essential for sound financial planning and investment decision-making for a rectified spirit production facility. The cost structure is dominated by raw material procurement, which accounts for approximately 70-80% of total operating expenses, reflecting the fermentable substrate intensity of the distillation process. Molasses and grain feedstocks represent the primary cost driver, supplemented by yeast and fermentation nutrients, process water, and specialty chemicals for effluent treatment. Utilities represent 10-15% of OpEx, covering the substantial steam, electrical, and cooling water requirements of multi-column continuous distillation operations. The remaining operating cost components encompass labour, packaging and storage, transportation and logistics, routine plant maintenance and repair, depreciation on capital assets, regulatory compliance costs, and applicable taxes and levies.

• Raw Materials: 70-80% of OpEx

• Utilities: 10-15% of OpEx

Raw material costs at 70-80% of OpEx are dominated by molasses or grain feedstocks as the primary fermentable carbohydrate substrate, with yeast and fermentation nutrients comprising the remainder of direct production inputs. The weight of raw material costs in the total OpEx structure underscores the critical importance of feedstock procurement strategy, supplier diversification, proximity to sugarcane or grain production zones, and long-term supply agreement management in protecting operational margin stability. By the fifth year of operations, total operational costs are expected to increase substantially due to inflationary pressures on feedstock and energy input prices, potential fluctuations in molasses availability linked to sugarcane crop cycles, rising labour costs, and increasing environmental compliance expenditure. Long-term supply contracts with reliable and geographically proximate raw material suppliers are essential to cost predictability and production continuity.

Capital Investment Requirements:

Establishing a rectified spirit production plant requires substantial and carefully structured capital investment, with the total programme determined by target production volume, distillation technology configuration, degree of process automation, co-product recovery provisions, and geographic location of the manufacturing site. The capital expenditure programme covers land acquisition, site development and civil construction, procurement and installation of fermentation and distillation plant, utilities infrastructure including boilers, cooling towers, and steam distribution systems, effluent treatment facilities, tankage and product storage infrastructure, quality control laboratory fitment, and initial working capital provisions to cover feedstock stocking and production ramp-up costs.

Land and Site Development: The selected site must provide reliable and cost-competitive access to primary raw materials, principally molasses from nearby sugar mills for cane-based production, or grain from agricultural supply zones for grain-based distilleries. Proximity to the primary feedstock supply source is a critical cost factor given the high weight and volume of fermentable substrate inputs required for large-volume distillery operations. The site must also offer reliable access to large volumes of clean process water for fermentation and cooling applications, stable industrial power supply for continuous distillation column operations, and robust road or rail transportation infrastructure for both feedstock inbound logistics and finished spirit product despatch to beverage, pharmaceutical, chemical, and fuel blending customers. Full compliance with applicable industrial alcohol manufacturing permits, excise duty registration requirements, environmental clearances, and water use authorisations must be secured prior to commencement of construction.

Machinery and Equipment: Machinery and process equipment procurement represents the single largest component of capital expenditure for a rectified spirit facility. Essential process equipment includes raw material receiving, storage, and milling systems for grain-based plants; molasses dilution and clarification systems for cane-based operations; pre-treatment and sterilisation units; large-volume stainless steel fermentation vessels equipped with temperature control, agitation, and yeast dosing systems for controlled alcoholic fermentation; beer still columns for primary distillation of the fermented wash; rectification columns for purification to the target 95% ethanol specification; aldehyde and fuel oil extraction columns for impurity removal in high-purity pharmaceutical grades; plate condensers, heat exchangers, and reflux systems for energy efficiency; large-capacity stainless steel product storage tanks; boilers and steam generation systems; cooling towers and water circulation systems; and comprehensive effluent treatment plant for vinasse and process wastewater management. All equipment must comply with applicable pressure vessel standards, food-grade material requirements for beverage and pharmaceutical applications, and flammable liquid handling safety codes.

Civil Works: Building and civil infrastructure design must optimise process flow efficiency, operational safety, and regulatory compliance across all production stages of this continuous and fire-risk-bearing process. The facility must incorporate clearly designated zones for feedstock receiving and storage, fermentation hall operations, distillation column block, product storage tankage farm, quality control and analytical laboratory, utilities plant including boilers and cooling towers, effluent treatment plant, and administration and control room. Reinforced foundations for large fermentation vessels and distillation columns, fire-rated construction in all alcohol vapour exposure zones, bunded containment areas around spirit tankage, explosion-proof electrical fittings throughout the production area, and appropriate venting and monitoring systems for flammable vapour management must all be incorporated into the civil design. Provision for future fermentation or distillation capacity expansion must be embedded into the initial layout to accommodate production growth without requiring extensive additional civil works.

Buy Report Now: https://www.imarcgroup.com/checkout?id=8504&method=2175

Major Applications and Market Segments:

Rectified spirit serves a uniquely broad and commercially critical range of applications across multiple high-value industries, establishing it as one of the most versatile and strategically important industrial alcohol products in the global chemicals and food processing economy. In the alcoholic beverages industry, rectified spirit serves as the fundamental alcohol base that distillers and blenders use to create a wide range of potable spirits, liqueurs, and alcoholic beverage products. Its high ethanol purity and neutral flavour profile make it the preferred base material for vodka, gin, rum, whisky blending, and fortified wine production, where the absence of congeners and off-flavour compounds is essential to final product quality and consistency.

In the pharmaceutical industry, rectified spirit meeting pharmacopoeial purity specifications serves as a solvent and antiseptic agent in the manufacture of medicinal syrups, tinctures, oral liquid formulations, topical antiseptics, wound care products, and hospital-grade surface disinfectants. Its high ethanol concentration, rapid antimicrobial efficacy, and chemical compatibility with a wide range of active pharmaceutical ingredients make it an indispensable excipient and processing solvent across both traditional and modern pharmaceutical manufacturing operations. In the chemical industry, rectified spirit functions as a primary feedstock to produce acetic acid, ethyl acetate, diethyl ether, acetaldehyde, and numerous other ethanol-derived industrial chemicals, serving as the starting material for a broad chain of downstream chemical synthesis operations.

In the personal care and cosmetics industry, rectified spirit is incorporated into perfumes, colognes, deodorants, hair care products, skin tones, and cosmetic formulations for its solvent properties, rapid evaporation characteristics, and antimicrobial functionality. In the biofuel sector, rectified spirit serves as the primary feedstock for dehydration to anhydrous fuel ethanol at 99.5% or higher purity for blending with petrol under national ethanol blending mandates, representing one of the largest and most policy-driven demand segments for industrial alcohol producers globally. The production process follows a continuous multi-stage sequence of raw material preparation and quality verification, substrate dilution and sterilisation, temperature-controlled batch or continuous fermentation, multi-column distillation and rectification, quality assurance testing, product storage, and despatch to end-use customers across all application sectors.

Why Invest in Rectified Spirit Production?

Several robust and structurally supported factors collectively drive the investment attractiveness of rectified spirit manufacturing for industrial chemicals sector participants, agri-business investors, and strategic capital allocators:

• Rising Demand for Industrial Alcohol: The demand for industrial alcohol is growing consistently across its primary end-use sectors of pharmaceuticals, specialty chemicals, personal care, and institutional sanitation. This multi-sector demand foundation creates a structurally resilient and diversified revenue base for rectified spirit producers that reduces dependence on any single downstream market and supports stable utilisation rates across the business cycle.

• Government Support for Ethanol Blending: Ethanol blending mandates implemented by governments across India, Brazil, the United States, the European Union, and numerous Southeast Asian and African nations create a powerful, policy-driven, and volume-predictable demand stream for rectified spirit and downstream fuel ethanol production. These blending programmes provide producers with a large, government-backed offtake channel that operates independently of consumer discretionary spending cycles and strengthens the overall demand floor for the industry.

• Diverse End-Use Applications: The unique multi-industry addressability of rectified spirit across beverages, pharmaceuticals, industrial chemicals, personal care, and biofuels means that producers can serve multiple customer segments simultaneously, diversifying revenue concentration risk and enabling production volume optimisation across demand cycles in individual sectors. This application breadth is a defining competitive strength of the rectified spirit business model relative to more narrowly focused specialty chemical production.

• Scalable Production Model: The continuous distillation technology that underpins rectified spirit production enables producers to systematically scale output through additional fermentation vessel capacity, expanded distillation column throughput, and process efficiency improvements without requiring fundamental changes to the core production technology platform. This scalability supports graduated capacity investment aligned with market demand growth, reducing capital risk while preserving upside volume potential.

• Strong Export Potential: The rising global demand for industrial ethanol, pharmaceutical-grade alcohol, and fuel ethanol creates significant cross-border trade opportunities for rectified spirit producers with competitive feedstock access, efficient production operations, and the regulatory compliance frameworks required to serve international pharmaceutical and food-grade alcohol markets. Export revenue diversification reduces domestic market concentration risk and supports higher average unit realisations through access to premium-priced international specialty alcohol segments.

Manufacturing Process Excellence:

Rectified spirit production follows a continuous and carefully engineered multi-stage manufacturing process that transforms fermentable carbohydrate feedstocks into high-purity ethanol through controlled biological fermentation and sequential multi-column distillation. The process commences with receipt and quality verification of incoming feedstocks-principally molasses or grain-to confirm sugar content, microbial load, and pH within acceptable fermentation parameters before transfer to preparation systems. Molasses undergoes dilution to the target sugar concentration with process water and pH adjustment, while grain feedstocks require milling, cooking, and enzymatic liquefaction and saccharification to convert starch to fermentable sugars prior to fermentation.

Prepared fermentation media are transferred to temperature-controlled stainless steel fermentation vessels where selected yeast strains are pitched under controlled conditions to initiate alcoholic fermentation, converting fermentable sugars to ethanol and carbon dioxide over a defined fermentation cycle of typically 30 to 72 hours.

The resulting fermented wash, containing approximately 8-12% ethanol by volume, is then subjected to continuous multi-column distillation beginning with the beer still or analyser column, which strips ethanol and volatile congeners from the fermented substrate. The stripped vapour proceeds through rectification columns operating under controlled reflux ratios to progressively concentrate ethanol to the target 95% rectified spirit specification, while simultaneously separating head fractions including acetaldehyde and ethyl acetate in the aldehyde column, and fuel oil side streams containing higher alcohols, for pharmaceutical and high-purity beverage spirit production.

Finished rectified spirit meeting specification is transferred to stainless steel product storage tanks, sampled for full quality assurance analysis including ethanol strength, residual congener levels, acidity, and colour, and then despatched by road tanker or drum to customer facilities across all end-use sectors. Spent wash and process effluents are treated in the dedicated effluent treatment plant to meet applicable discharge standards before final disposal or co-product recovery as fertiliser.

Industry Leadership:

Leading producers in the global rectified spirit and industrial alcohol industry include a broad range of multinational distillery operators, integrated agri-business conglomerates, and specialised industrial alcohol manufacturers with extensive production footprints and diverse downstream supply relationships across beverages, pharmaceuticals, chemicals, and biofuels. The Asia Pacific region hosts the largest concentration of rectified spirit production capacity globally, with India in particular home to a large and growing number of large-scale distillery operators that together serve domestic beverage, pharmaceutical, and ethanol blending demand while also exporting across South and Southeast Asia.

These established producers maintain competitive advantages through feedstock procurement scale, energy-efficient continuous distillation technology, established regulatory compliance frameworks for excise and pharmaceutical grade production, long-term supply relationships with major beverage and pharmaceutical customers, and integration across the cane or grain agricultural value chain that provides upstream feedstock cost advantages.

Browse Full Report: https://www.imarcgroup.com/rectified-spirit-manufacturing-plant-project-report

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company excels in understanding its client's business priorities and delivering tailored solutions that drive meaningful outcomes. We provide a comprehensive suite of market entry and expansion services. Our offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: (+1-201-971-6302)

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Rectified Spirit Production Cost DPR 2026: Unit Setup, CapEx/OpEx Analysis with Profitability Forecast here

News-ID: 4421465 • Views: …

More Releases from IMARC Group

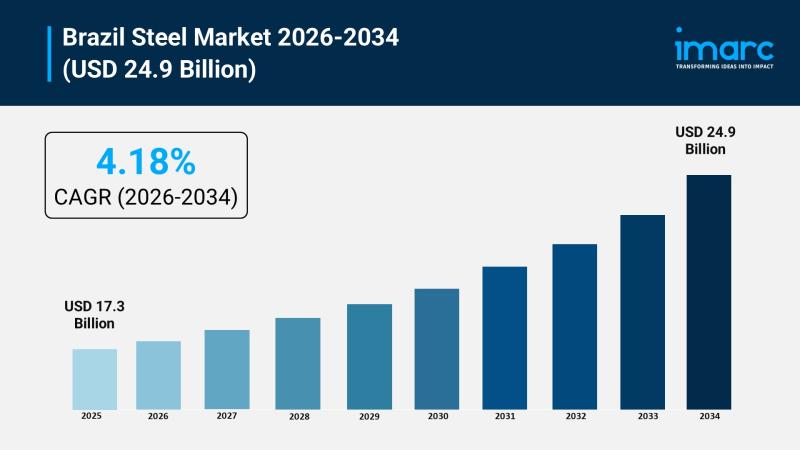

Brazil Steel Market Forecast: Revenue, Production & Demand Outlook Through 2034

Brazil's steel industry sits at the intersection of two powerful forces: a construction and infrastructure boom that shows no signs of slowing, and a global decarbonization push that is reshaping how steel itself gets made. The Brazil steel market, valued at USD 17.3 Billion in 2025, is projected to reach USD 24.9 Billion by 2034, growing at a compound annual rate of 4.18% between 2026 and 2034. That trajectory reflects…

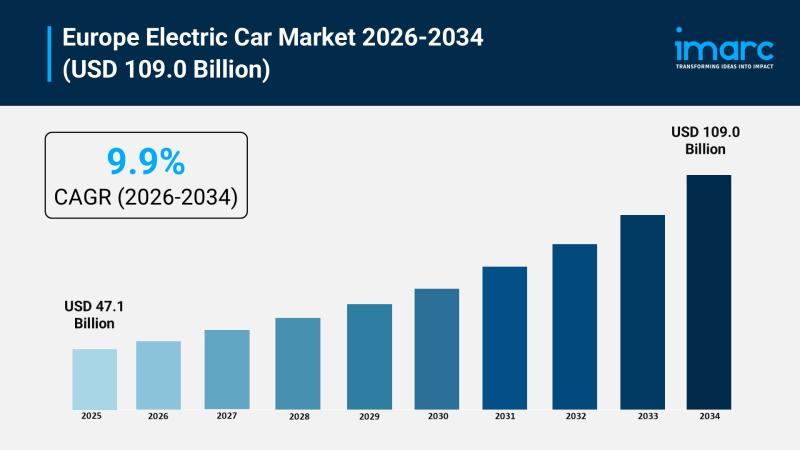

Europe Electric Car Market Report 2026: Revenue, CAGR & Emerging Opportunities B …

Europe's electric car industry is entering a phase where policy, affordability, and infrastructure are finally moving in the same direction at the same time. The Europe electric car market, valued at USD 47.1 Billion in 2025, is projected to reach USD 109.0 Billion by 2034, growing at a compound annual rate of 9.9% between 2026 and 2034. This trajectory reflects more than doubling market value within a decade, driven by…

Mexico Precision Agriculture Market Size Projected to Reach USD 289.5 Million by …

IMARC Group has recently released a new research study titled "Mexico Precision Agriculture Market Report by Technology (GNSS/GPS Systems, GIS, Remote Sensing, Variable Rate Technology (VRT), Others), Type (Automation and Control Systems, Sensing and Monitoring Devices, Farm Management System), Component (Hardware, Software), Application (Mapping, Crop Scouting, Yield Monitoring, Soil Monitoring, Precision Irrigation, Others), and Region 2026-2034," offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive…

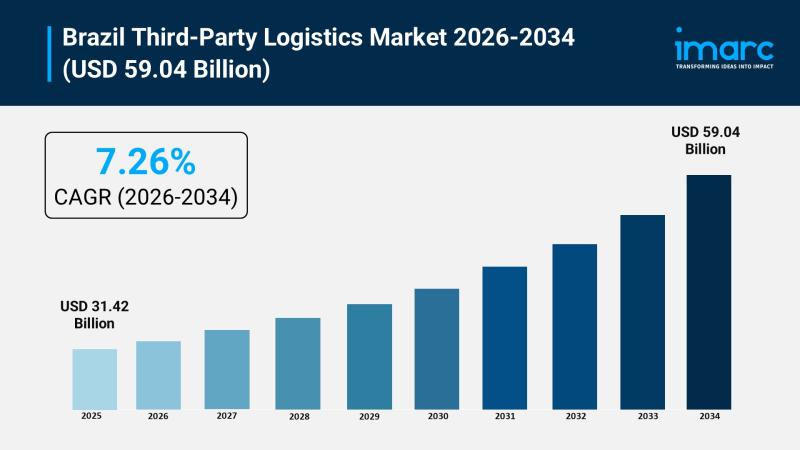

Brazil Third-Party Logistics Market to Reach USD 59.04 Billion by 2034 at 7.26% …

Brazil's outsourced logistics sector is scaling rapidly as e-commerce fulfillment, manufacturing recovery, and government-backed infrastructure investment converge into a single growth narrative. The Brazil third-party logistics market, valued at USD 31.42 Billion in 2025, is projected to reach USD 59.04 Billion by 2034, growing at a compound annual rate of 7.26% between 2026 and 2034, a pace that positions Brazil among Latin America's fastest-expanding logistics economies.

Download a sample copy of…

More Releases for Asia

Asia Private Equity Firm, Asia Private Equity Management, Asia Private Equity Se …

The private equity market in China has been rapidly growing in recent years. Private equity (PE) refers to the purchase of shares in a company that are not publicly traded on a stock exchange. PE firms typically target companies that are undervalued or in need of capital for growth, and aim to improve the company's operations and financial performance before selling it at a higher value.

https://boomingfaucet.com/

Asia Private Equity Consulting

E-mail:nolan@pandacuads.com

In China,…

South East Asia Business Jet Market And Top Key Players are Asia Corporate Jet, …

By 2022, the South East Asia Business Jet Markets estimated to reach US$ XX Mn, up from US$ XX Mn in 2016, growing at a CAGR of XX% during the forecast period. The Global Business Jet Market, currently at 21 million USD, contributes the highest share in the market and is poised to grow at the fastest rate in the future. The three broad categories of business jets are Small,…

LIXIL Asia Presents Asia Pacific Property Awards

Through its power brands GROHE and American Standard, LIXIL Asia signs a three-year deal to become the Headline Sponsor of the Asia Pacific Property Awards from 2019 until 2022.

23rd January 2019: The International Property Awards, first established in 1993, are open to residential and commercial property professionals from around the globe. They celebrate the highest levels of achievement by companies operating within the architecture, interior design, real estate and property…

PEOPLEWAVE WINS ASIA TECH PODCAST PITCHDECK ASIA 2019 AWARDS

15 January 2019, Singapore – Peoplewave, Asia’s leading data-driven HR technology company, won the Asia Tech Podcast (ATP) Pitchdeck Asia 2019 Awards, being awarded “Startup Most Likely to Succeed in 2019".

The 2019 Pitchdeck Asia Awards is an opportunity for the Asian Startup Ecosystem to shine a spotlight on some of its best startups. The awards were decided by a public vote. More than 7,200 votes were cast by registered LinkedIn…

Undersea Defence Technology Asia, UDT Asia 2011

Latest Military Diving Technologies featured in UDT Asia

Equipping Asia’s navies with the latest diving technology for asymmetric warfare and

operations

SINGAPORE, 17 October 2011 - Naval diving and underwater special operations is a field that is

seeing increased attention and investment amongst navies in Asia. Units such as the Indonesian Navy‟s KOPASKA, the Republic of Singapore Navy‟s Naval Diving Unit (NDU), the Royal Malaysian Navy‟s PASKAL are increasingly utilising specialised equipment for conducting…

Asia Diligence – Specialist Investigative Due Diligence for Asia & Beyond

Asia Diligence today announced the opening of its European Customer Services office in the United Kingdom. The office is to be managed by Steve Fowler and will focus on providing services to Asia Diligence’s European customers. Asia Diligence is also planning to open a US office in the near future, which will provide customer service to its US and North American clients.

Asked to comment on the move, Luke Palmer, the…