Press release

Styrene Production Plant DPR & Unit Setup - 2026: Machinery Cost, CapEx/OpEx, ROI, Raw Materials

Market Overview and Growth Potential:

The global styrene market demonstrates a strong growth trajectory, valued at USD 62.9 Billion in 2025. According to IMARC Group's comprehensive market analysis, the market is expected to reach USD 94.4 Billion by 2034, exhibiting a CAGR of 4.60% from 2026 to 2034. This sustained expansion is driven by growing demand for polystyrene packaging, construction insulation, automotive lightweight components, and rubber/latex (SBR).

Request for a Sample Report: https://www.imarcgroup.com/styrene-manufacturing-plant-project-report/requestsample

Styrene (C8H8), also called vinylbenzene/phenylethene, is a colorless-to-yellowish aromatic monomer characteristic sweet odor, primarily used as a building block for styrenic polymers. It is a reactive unsaturated hydrocarbon that readily undergoes free-radical polymerization, which is why it is typically stored and transported with polymerization inhibitors. Styrene is commonly manufactured from ethylbenzene via catalytic dehydrogenation and is then purified to polymer-grade quality. Its value is derived from its ability to form materials with a broad range of properties - from rigid foams (EPS) to tough engineering plastics (ABS) and elastomers (SBR).

The growth of the styrene production market is closely linked to expanding demand for packaging materials, particularly food packaging and protective foam solutions. The automotive sector's shift toward lightweight materials to improve fuel efficiency further supports ABS and SBR consumption. Rapid urbanization and infrastructure development drive the need for thermal insulation materials such as expanded polystyrene. Additionally, growth in tire production, especially in emerging economies, sustains demand for styrene-butadiene rubber. Integrated petrochemical complexes benefit from feedstock availability (benzene and ethylene), enabling cost-effective production.

Plant Capacity and Production Scale:

The proposed styrene production facility is designed with an annual production capacity ranging between 100,000 - 500,000 MT, enabling economies of scale while maintaining operational flexibility. This capacity range allows manufacturers to cater to diverse market segments - from construction and packaging, automotive and marine, to renewable energy and consumer goods - ensuring steady demand and consistent revenue streams across multiple industry verticals. The facility is designed to serve both domestic supply chains and export requirements, positioning the plant at the intersection of petrochemical efficiency and downstream polymer value chains.

Speak to Analyst for Customized Report: https://www.imarcgroup.com/request?type=report&id=7605&flag=C

Financial Viability and Profitability Analysis:

The styrene production business demonstrates healthy profitability potential under normal operating conditions. The financial projections reveal:

Gross Profit Margins: 20-30%

Net Profit Margins: 8-15%

These margins are supported by stable demand across construction, packaging, automotive, and synthetic rubber sectors; scale-driven cost competitiveness of large continuous plants; and the critical role of styrene as the backbone monomer for multiple high-volume downstream polymers. The project demonstrates strong return on investment (ROI) potential, making it an attractive proposition for both new entrants and established petrochemical manufacturers looking to integrate downstream into polymer derivatives.

Cost of Setting Up a Styrene Production Plant:

Operating Cost Structure:

Understanding the operating expenditure (OpEx) is crucial for effective financial planning and cost management. The cost structure for a styrene production plant is primarily driven by:

Raw Materials: 80-85% of OpEx

Utilities: 10-15% of OpEx

Other Expenses: Labor, packaging, transportation, maintenance, depreciation, and taxes

Raw materials constitute the largest portion of operating costs, with ethylbenzene being the primary input material - accounting for approximately 80-85% of total operating expenses (OpEx). Steam and catalyst form the secondary input requirements. Establishing long-term contracts with reliable ethylbenzene suppliers helps mitigate price volatility and ensures consistent raw material supply, which is critical given that feedstock price fluctuations represent the most significant cost factor in styrene production.

Capital Investment Requirements:

Setting up a styrene production plant requires substantial capital investment across several critical categories:

Land and Site Development:

Selection of an optimal location with strategic proximity to ethylbenzene, steam, and catalyst suppliers. The location must offer easy access to key raw materials and proximity to target markets to minimize distribution costs. The site must have robust infrastructure, including reliable transportation, utilities, and waste management systems. Compliance with local zoning laws, environmental regulations, and emission standards must also be ensured.

Machinery and Equipment:

The largest portion of capital expenditure (CapEx) covers specialized production equipment essential for styrene manufacturing. Key machinery includes:

Alkylation reactors: for the catalytic reaction of benzene and ethylene to produce ethylbenzene feedstock in integrated production configurations

Dehydrogenation reactors: for catalytic dehydrogenation of ethylbenzene to styrene monomer at high temperature with steam over iron oxide catalysts

Distillation columns: for separation and purification of styrene monomer from ethylbenzene, benzene, toluene, and heavy by-products

Condensation and heat recovery systems: for vapor condensation, energy recovery, and thermal integration across the dehydrogenation and separation units

Steam generation units: for supply of high-pressure steam required for the endothermic dehydrogenation reaction and process heating duties

Purification systems: for removal of inhibitors, impurities, and trace contaminants to achieve polymer-grade styrene purity specifications

Storage tanks: for safe storage of ethylbenzene feedstock, styrene monomer product, and inhibitor systems with appropriate polymerization prevention measures

Civil Works:

Building construction, factory layout optimization, and infrastructure development designed to enhance workflow efficiency, ensure workplace safety, and minimize material handling complexities throughout the production process. The layout should be optimized with separate areas for feedstock receipt and storage, reaction and dehydrogenation area, separation and distillation section, purification unit, quality control laboratory, product storage and dispatch area, utility block, effluent treatment plant, and administrative block.

Other Capital Cost:

Pre-operative expenses, machinery installation costs, regulatory compliance and environmental clearance costs, initial working capital requirements, safety system investments, and contingency provisions for unforeseen circumstances during plant establishment.

Buy Now: https://www.imarcgroup.com/checkout?id=7605&method=2175

Major Applications and Market Segments:

Styrene products find extensive applications across diverse market segments, demonstrating their versatility and critical importance across global industrial and consumer value chains:

Polystyrene Manufacturing: Used for general-purpose polystyrene (GPPS), high-impact polystyrene (HIPS), and expandable polystyrene (EPS) for packaging and insulation. EPS provides lightweight, rigid thermal insulation for building and construction applications, while GPPS and HIPS serve packaging, appliances, and consumer goods sectors.

Acrylonitrile Butadiene Styrene (ABS) Production: Used for automotive components, consumer goods, and electronic housings. ABS provides an optimal combination of rigidity, impact resistance, and processability, making it the material of choice for automotive interior trims, dashboards, and electronic enclosures.

Synthetic Rubber Production: Styrene-butadiene rubber (SBR) is used in tires and industrial rubber products. SBR is the dominant synthetic rubber grade globally, providing abrasion resistance and durability in passenger car, truck, and off-road tire applications.

Unsaturated Polyester Resins: Fiberglass-reinforced plastics used in construction, marine, and automotive applications. Styrene acts as the reactive diluent and cross-linking agent in unsaturated polyester resin systems used for boat hulls, wind turbine blades, and structural composite components.

Why Invest in Styrene Production?

Several compelling factors make styrene production an attractive investment opportunity:

Backbone Monomer for Multiple High-Volume Polymers:

Styrene is the key feedstock for PS, EPS, ABS/SAN, latex, and resins - supporting diverse downstream demand and enabling portfolio flexibility across commodity and engineering polymer applications. This structural indispensability ensures consistent demand spanning all industrial, construction, automotive, and consumer sectors.

Integration Benefits with Refinery/Petrochemical Hubs:

Styrene economics improve when co-located with crackers and refineries due to easier access to benzene and ethylene, shared utilities, and optimized heat integration across aromatic and olefin value chains. Strategic co-location reduces feedstock logistics costs and improves overall plant economics.

Scale-Driven Cost Competitiveness:

Large, continuous plants benefit from economies of scale in reaction, distillation, utilities, and maintenance, reducing per-ton production cost and improving competitiveness in export-oriented regions. Annual production capacity of 100,000 - 500,000 MT enables significant cost advantages over smaller batch operations.

Technology Upgrades Can Materially Improve Efficiency:

New catalyst and process improvements targeting lower steam-to-oil ratios and higher selectivity can reduce energy intensity and operating costs in ethylbenzene dehydrogenation units. For instance, Clariant's StyroMax UL-100 catalyst achieves exceptional performance at steam-to-oil ratios of 0.76 by weight, setting a new industry benchmark in styrene monomer production efficiency.

Strategic Relevance Despite Cyclicality:

Styrene is cyclical, but it remains strategically important to chemical clusters. Producers can hedge via integration into derivatives (PS/EPS/ABS) and by-products management, enabling more stable earnings profiles across commodity price cycles.

Manufacturing Process Excellence:

The styrene production process involves several precision-controlled stages to deliver polymer-grade styrene monomer compliant with international quality specifications:

Ethylbenzene Preparation: Ethylbenzene feedstock is received, quality-checked, and pre-heated prior to introduction into the dehydrogenation reactor system; in integrated facilities, ethylbenzene is produced via catalytic alkylation of benzene with ethylene

Catalytic Dehydrogenation: Ethylbenzene undergoes catalytic dehydrogenation over iron oxide-based catalyst at high temperature with steam, converting ethylbenzene to styrene monomer with hydrogen as a co-product in the endothermic reaction

Condensation and Phase Separation: Reactor effluent vapors are condensed and the organic phase (crude styrene) is separated from the aqueous condensate using condensation and heat recovery systems with energy integration

Distillation and Purification: Crude styrene is purified through a series of distillation columns to remove unreacted ethylbenzene, benzene, toluene, and heavy by-product fractions, yielding polymer-grade styrene monomer

Inhibitor Addition: Polymerization inhibitor (typically 4-tert-butylcatechol or similar) is added to the purified styrene product to prevent premature polymerization during storage and transportation

Quality Inspection: Finished styrene is analyzed for purity, inhibitor content, color (APHA), peroxide content, and other polymer-grade specifications before transfer to product storage tanks

Storage and Dispatch: Polymer-grade styrene monomer is stored in inhibited storage tanks under nitrogen blanket and dispatched via tanker, rail car, or pipeline to downstream polymer manufacturers

Industry Leadership:

The global styrene industry is led by established petrochemical manufacturers with extensive production capacities and diverse application portfolios. Key industry players include:

• INEOS Styrolution

• SABIC

• LyondellBasell Industries

• TotalEnergies

• Shell Chemicals

• Chevron Phillips Chemical

These companies serve diverse end-use sectors including construction, packaging, automotive, marine, renewable energy, and consumer goods, demonstrating the broad market applicability of styrene and its downstream derivatives across global industrial value chains.

Recent Industry Developments:

September 2025: INEOS Styrolution disclosed that the first truckloads of recycled styrene monomer (SM) had arrived at its Antwerp site. The material was supplied by Indaver from its new depolymerisation plant, the first facility in Europe dedicated to polystyrene recycling. This milestone marks a significant step toward circular economy integration within the global styrene supply chain.

April 2025: Clariant announced the launch of StyroMax UL-100, its most advanced ethylbenzene dehydrogenation catalyst to date. This innovative catalyst achieves exceptional performance at unprecedented low steam-to-oil ratios (S/O) of 0.76 by weight, setting a new industry benchmark in styrene monomer production efficiency and energy consumption reduction.

Browse Full Report: https://www.imarcgroup.com/styrene-manufacturing-plant-project-report

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers create a lasting impact. The company excels in understanding its clients' business priorities and delivering tailored solutions that drive meaningful outcomes. IMARC Group provides a comprehensive suite of market entry and expansion services, including market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: (+1-201-971-6302)

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Styrene Production Plant DPR & Unit Setup - 2026: Machinery Cost, CapEx/OpEx, ROI, Raw Materials here

News-ID: 4420340 • Views: …

More Releases from IMARC Group

Tire Market to Surpass USD 272.6 Billion by 2034, At a CAGR of 4.33%

According to IMARC Research, The global tire market has stabilized and is indicating uniform growth. In the long term‚ the global automotive tire market is envisaged to grow continuously due to increasing demand for automobiles‚ constant development of tire-manufacturing technologies‚ and increasing sustainability emphasis. The rapidly growing automotive industry has changed the perception of tires from consumables to a high-performance product that impacts fuel economy‚ safety‚ and driving comfort.

The market…

Canada Robotic Fruit Picker Market Set to Reach USD 12.87 Million by 2034, Drive …

Once defined by seasonal migrant workforces and hand-picked harvests, the Canada Robotic Fruit Picker Market is entering a new era of technology-led transformation. Persistent labor shortages, rising operational costs, and a wave of government investment in agricultural automation are collectively rewriting Canada's fruit harvesting story. After reaching USD 7.40 Million in 2025, the market is on a clear trajectory toward USD 12.87 Million by 2034, reflecting a steady CAGR of…

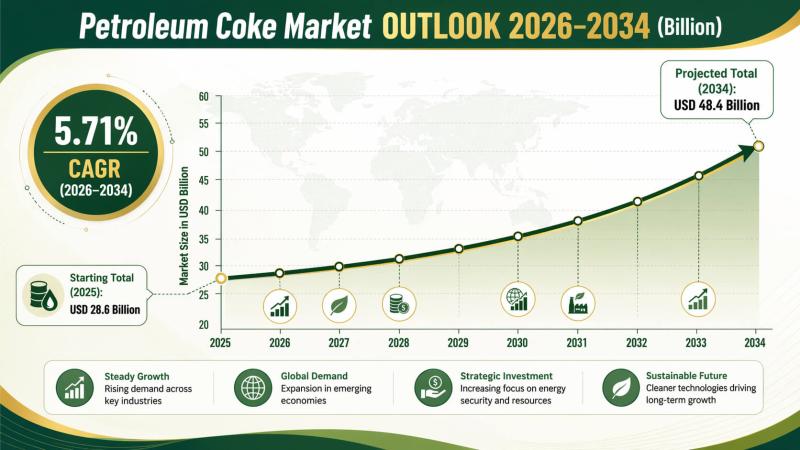

Petroleum Coke Market Size, Share, Trends and Forecast by Type, Application, and …

As per the IMARC group‚ the current market trends for petroleum coke are moderate. The increase in demand in energy intensive industries‚ such as aluminum‚ cement‚ steel‚ and power generation‚ is a major driving force for the market. Further‚ the high carbon content and high calorific value make petroleum coke suitable as an alternative fuel in countries with increasing industrialization and energy demand.

The market was valued at USD 28.6 Billion…

United States e-KYC Market Poised for Strong Growth Through 2033, Driven by Digi …

IMARC Group, a global market research and management consulting firm, has published a comprehensive new report on the United States e-KYC Market. According to the report, the United States e-KYC market is experiencing robust expansion, driven by the rapid growth of digital financial services, stringent regulatory compliance requirements, and accelerating adoption of AI-powered identity verification technologies across the banking, fintech, insurance, and telecom sectors.

Electronic Know Your Customer (e-KYC) refers to…

More Releases for Styrene

Global Styrene Butadiene Styrene (SBS) Market Competitor Analysis Report 2025

"Global Styrene Butadiene Styrene (SBS) Market 2025 by Manufacturers, Regions, Type and Application, Forecast to 2031" is published by Global Info Research. It covers the key influencing factors of the Styrene Butadiene Styrene (SBS) market, including Styrene Butadiene Styrene (SBS) market share, price analysis, competitive landscape, market dynamics, consumer behavior, and technological impact, etc.At the same time, comprehensive data analysis is conducted by national and regional sales, corporate competition rankings,…

Styrene Dynamics: Alpha Methyl Styrene Industry's Evolution 2023-2033

The alpha methyl styrene market is witnessing emerging trends and an optimistic market forecast as the industry uncovers new opportunities. A comprehensive market analysis report delves into the increasing demand for alpha methyl styrene, driven by its versatile applications and unique properties.

Alpha methyl styrene (AMS), a derivative of styrene, finds wide-ranging usage in industries such as plastics, adhesives, and coatings. The report emphasizes the growing need for high-performance materials and…

Styrene-Ethylene-Butadiene-Styrene (SEBS) Market 2022 | Detailed Report

This report provides an informative view about the competitive aspect of the global market. It includes detailed picture of the exhibition of a portion of the essential global players working in the Styrene-Ethylene-Butadiene-Styrene (SEBS) market. The research study also provides historical record with profits predictions and forecasts from 2022 to 2028. Also, the business manufacturing of the notable manufacturers is also emphasized with technical data in the report.

This report is…

Styrene Butadene Styrene (SBS) Market Provides in-depth analysis of the Styrene …

Overview of the Report: Styrene Butadene Styrene (SBS) Market

The market intelligence report on the Styrene Butadene Styrene (SBS) Market includes key segments of the entire market. The main objective of the statistical analysis included in this report is to shed light on the prevalent business models, analyze the market trends, and investigate the different market aspects.

If you are interested in the Styrene Butadene Styrene (SBS) industry or wish to keep…

Styrene Butadene Styrene Market Size, Share, Development by 2024

Global Info Research offers a latest published report on Styrene Butadene Styrene Market Analysis and Forecast 2019-2025 delivering key insights and providing a competitive advantage to clients through a detailed report. This report focuses on the key global Styrene Butadene Styrene players, to define, describe and analyze the value, market share, market competition landscape, SWOT analysis and development plans in next few years.

To analyze the Styrene Butadene Styrene with respect…

Styrene Ethylene Butylene Styrene Market Latest Report with Forecast 2018 – 20 …

Thermoplastic elastomers (TPEs) are a class of copolymers (typically a mixture of rubber and plastic) that contain materials with both elastomeric and thermoplastic properties. There are six generic classes of commercial TPEs, out of which one is styrenic block copolymers (SBC), in which styrene ethylene butylene styrene (SEBS) is categorized. It accounts for a majority share of over 65% of the total SBCs. SEBS polymer is a type of TPE…