Press release

Cargo Insurance Explained: Warehouse-to-Warehouse vs. Carrier Liability

When a batch of electronic products departs from a Southeast Asian factory warehouse, transits by sea and land to a distribution warehouse in Europe, and is damaged by rain in the transit yard, the cargo owner often faces a dilemma: should they claim compensation from the carrier or file a claim with the insurance company? In the international logistics chain, "warehouse-to-warehouse" insurance and carrier liability are often confused, and the setting of deductibles is crucial in directly affecting risk costs and the strength of protection. This article will break down these core issues layer by layer, providing a clear practical guide for cross-border freight practitioners.

I. Core Concept Breakdown: Understanding Two "Liability Boundaries"

In the international freight [https://www.brandempowerer.com/fba-ddp-shipping/] risk protection system, "warehouse-to-warehouse" insurance and carrier liability are two independent and complementary dimensions of protection, with fundamental differences in their sources, scope, and nature of liability.

1. Warehouse-to-Warehouse Insurance: Proactive Risk Transfer Covering the Entire Supply Chain

Warehouse-to-Warehouse (W/W) insurance is a core clause in international cargo insurance, widely incorporated into the London Insurance Institute (ICC) terms and the People's Insurance Company of China (CIC) terms. Essentially, it represents a comprehensive liability guarantee agreed upon by the insurer and the insured. Its core definition includes three key dimensions:

- Liability Start and End Points: Liability begins when the insured goods leave the warehouse at the point of origin specified in the policy, covering all normal transshipment stages, including sea, land, inland waterway, and barge transport, until arrival at the consignee's warehouse at the destination. If arrival is delayed, liability is limited to 60 days after the goods are unloaded from the ocean vessel; if transshipment is required, liability terminates at the start of transshipment. For example, once goods in a Chinese factory warehouse are loaded onto a transport vehicle and leave the warehouse, the insurance liability takes effect until the final warehouse in Germany signs for receipt.

- Coverage: Within the scope of the insurance policy (e.g., all risks, free risk), it covers natural disasters (rainstorms, earthquakes), accidents (collisions, fires), losses arising from transportation delays, and even risks during temporary storage of goods in port yards.

- Core Attributes: This is commercial insurance proactively purchased by the cargo owner, serving as a "risk hedging tool." Premiums are directly linked to the cargo value, transportation route, and type of insurance. Compensation is based on the insurance contract, not the transportation contract.

2. Carrier Liability: Legally mandated minimum obligations under the transportation contract

Carrier liability is a legal obligation undertaken by freight companies (e.g., shipping companies, freight forwarders) based on the transportation contract. Its core basis is international conventions such as the Hague-Visby Rules and the Hamburg Rules. Its essence is "performance guarantee" rather than "comprehensive insurance," with the following characteristics:

- Limited Boundaries of Liability: It only covers risks during the period the goods are under the actual control of the carrier, typically from the time the goods are loaded onto the means of transport (ship, plane, truck) until unloading, excluding the period after loading at the port of origin and unloading at the destination warehouse. For example, if goods are damaged due to forklift malfunction during loading at a factory warehouse, the carrier is not liable.

- Numerous exemptions: International conventions explicitly stipulate carrier exemption clauses, including force majeure (war, strikes), inherent defects in the goods (such as spoilage of fresh goods), shipper's fault (improper packaging), and navigational negligence (captain's error). In practice, carriers often refuse compensation on the grounds of "natural disasters" or "problems with the goods themselves."

- Strict compensation limits: Even if the carrier is liable, the compensation amount is limited by conventions, usually calculated based on the weight or number of pieces of goods, far lower than the actual value of the goods. For example, the Hague-Visby Rules stipulate a compensation limit of 100 per piece of cargo. Although modern conventions have increased this limit, it still cannot cover losses of high-value goods.

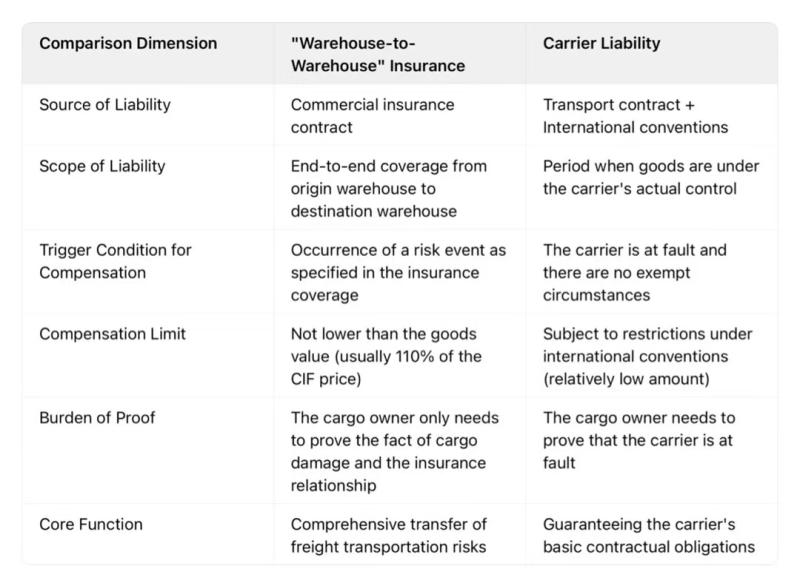

II. Essential Confrontation: A Table to Clarify Core Differences

Many cargo owners mistakenly believe that "finding a reliable carrier means you don't need to buy insurance," which confuses the liability logic of the two. The following comparison highlights the irreplaceable nature of the two insurance products across six key dimensions:

Image: https://ecdn6.globalso.com/upload/p/613/image_other/2025-12/wechatimg5032.jpg

Typical Case: A batch of 3C products was transported from a Shenzhen warehouse to Rotterdam, Netherlands, and was damaged by a port fire during transit in Singapore. When the cargo owner claimed compensation from the shipping company, the shipping company refused to pay, citing "fire as a force majeure event." However, the cargo owner, who had purchased "warehouse-to-warehouse" all-risk insurance, successfully obtained compensation of 110% of the cargo value based on the fire certificate and the insurance policy.

III. Key Practical Points: How to Balance Cost and Protection When Setting Deductibles?

A deductible is the "self-insured amount" stipulated in the insurance contract; that is, when cargo damage occurs, the insurance company only pays for the portion exceeding the deductible. Setting a reasonable deductible can find a balance between reducing premiums and minimizing self-insured losses.

1. Understand the Two Deductible Models

Two common deductible models are found in international cargo insurance, and in practice, the higher of the two is usually chosen:

- Absolute Deductible (Fixed Amount): A minimum self-insured amount for each incident, such as RMB 1000 or USD 200.

- Relative Deductible (Percentage): Calculated as a percentage of the loss amount, such as 10% or 20%.

For example, if the loss amount of a shipment is 8,000 yuan, and the insurance contract stipulates that "the deductible is 1,000 yuan or 20% of the loss amount, whichever is higher," then the deductible is 8,000 times 20% = 1,600 yuan, and the insurance company actually pays 8,000 - 1,600 = 6,400 yuan.

2. Three dimensions determine the setting of the deductible

The deductible and the premium have an "inverse relationship": the higher the deductible, the lower the premium, but the greater the risk borne by the cargo owner. It is necessary to make a comprehensive judgment based on the characteristics of the goods, the transportation scenario, and historical data:

(1) Differentiated setting according to the type of goods

The risk of damage and the repair cost of different goods vary greatly, and the deductible needs to be adjusted accordingly, referring to industry practices:

- High-value precision goods (3C products, medical devices): For these goods, even slight damage can cause significant losses. It is recommended to set a low deductible, such as "500 yuan or 10% of the loss amount, whichever is higher." 4PX Express follows this logic in setting deductibles for 3C products such as mobile phones.

- Fragile items (glassware, ceramics): High risk of breakage. Insurance companies typically set higher deductibles, accepting a "2000 yuan or 20% of the loss" clause, while also using "additional breakage insurance" to reduce risk.

- General goods (textiles, plastic products): Lower risk. A deductible of "1000 yuan or 10% of the loss" can be set to reduce premium expenses.

- Bulk low-value goods (coal, ore): Higher deductibles (such as 5%-8% of the loss) are acceptable, or even partial insurance can be waived, spreading the risk through bulk transportation.

(2) Adjustments based on transportation routes and methods

- High-risk routes: Such as Southeast Asian rainy season routes (frequent typhoons), and land transportation to war-torn Middle East regions. It is recommended to reduce the deductible and prioritize coverage; even if the premium increases by 10%-15%, significant losses can be avoided. - Multimodal transport scenarios: The more transit links, the higher the risk. The deductible should be controlled within 10% of the loss amount, and insurance coverage for all modes of transport should be confirmed.

- Short-distance transport: Such as land transport within Europe, the risk is lower, and a higher deductible can be set (e.g., a fixed deductible of 2,000 yuan) to save on premiums.

(3) Dynamic optimization based on historical claims data

If a route has no cargo damage claims for 12 consecutive months, the deductible can be increased by 20%-30% to reduce premium costs; if a type of cargo is damaged more than 3 times within 6 months, the deductible should be reduced and problems in packaging and transportation should be investigated, while negotiating with the insurance company to adjust the insurance type.

3. Avoidance guide: Common misconceptions about deductible settings

- Misconception 1: Blindly pursuing "zero deductible": Zero deductible premiums are usually 30%-50% higher than regular deductibles, which is extremely low cost-effectiveness for low-risk goods. Unless it is precision equipment with a unit price exceeding one million, it is not recommended to choose this option. - Misconception 2: Ignoring the impact of "insurance ratio" on deductibles: If the cargo owner only insures 80% of the cargo value, the deductible is still calculated based on the full cargo loss. For example, if the cargo value is 100,000 yuan, the insured amount is 80,000 yuan, the cargo loss is 50,000 yuan, and the deductible is 10,000 yuan (20%), then the insurance company will only pay (50,000-10,000) times 80% = 32,000 yuan. Therefore, it is recommended to insure 100% of the cargo value.

- Misconception 3: Failure to clarify the applicable scenarios for deductibles: Some insurance contracts stipulate that "the deductible is halved for fire and explosion accidents." The cargo owner needs to clarify the deductible rules for special scenarios in the contract to avoid disputes over claims.

IV. Summary: Building a dual protection system of "insurance + carrier"

The risk chain of international freight runs through the entire "warehouse-transportation-warehouse" process. "Warehouse-to-warehouse" insurance is the core protection covering the entire process, while the carrier's liability is only the bottom-line obligation in the "middle segment." The two are not interchangeable. Shippers should first determine their own risk tolerance, and then set deductibles based on cargo characteristics and transportation scenarios: high-risk goods should choose "low deductible + full coverage," while low-risk goods should choose "high deductible + basic coverage," dynamically optimizing the plan based on historical data.

Ultimately, a reasonable risk protection strategy is not about "spending the least amount of money," but about "transferring core risks at an appropriate cost"-this is the true value of international freight insurance.

Media Contact

Company Name: Brand Empowerer

Email:Send Email [https://www.abnewswire.com/email_contact_us.php?pr=cargo-insurance-explained-warehousetowarehouse-vs-carrier-liability]

Phone: +86 17665311168

Address:Room 301, Lijiatang, Beiyuan Street

City: Yiwu

State: Zhejiang

Country: China

Website: https://www.brandempowerer.com/

Legal Disclaimer: Information contained on this page is provided by an independent third-party content provider. ABNewswire makes no warranties or responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you are affiliated with this article or have any complaints or copyright issues related to this article and would like it to be removed, please contact retract@swscontact.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Cargo Insurance Explained: Warehouse-to-Warehouse vs. Carrier Liability here

News-ID: 4319635 • Views: …

More Releases from ABNewswire

Best NYC Business Brokers 2026 Rankings Released by Experts for US Consumers

Learn about the best NYC business brokers of 2026 through IRAEmpire's new and updated rankings for the robust market.

IRAEmpire has released its updated rankings of the best New York Business Brokers of 2026.

Consult the Best Business Selling Brokers in NYC [https://www.iraempire.com/businessbroker]

NYC business brokers help owners value, market, negotiate and sell privately held companies throughout Manhattan, Brooklyn, Queens, the Bronx and Staten Island. The best broker for a New York City…

Best Medical Equipment Financing Companies in the USA 2026 Rankings Released

Learn about the top medical equipment financing companies in the USA based on reviews, rates and more through IRAEmpire's new list.

IRAEmpire has released a new list of the best medical equipment financing companies in the USA.

Get Equipment Financing from USA's No.1 Ranked Company [https://www.iraempire.com/bl9w]

According to Michael Hunt, Senior Writer at IRAEmpire, "Medical equipment financing allows healthcare practices, laboratories, imaging centers, home healthcare companies, and other medical businesses to acquire essential…

How to Sell A Small Business in Houston, TX: Valuation, Preparation, Best Broker …

Learn how to sell your small business in Houston through IRAEmpire's new and updated guide.

IRAEmpire has published a new guide on how to sell your business in Houston, Texas to help business owners.

Consult the Best Business Selling Brokers in Houston [https://www.iraempire.com/businessbroker]

Selling your small business in Houston can help you convert years of work into retirement income, investment capital, or funding for your next venture. Houston's large population, diverse economy, international…

The ONE Music outlines a practical digital piano selection framework for advanci …

The ONE Music identifies keyboard action, installation format, creative connectivity and long-term practice goals as four central factors in choosing a digital piano.

The ONE Music has organized its digital piano collection around a practical comparison framework for musicians moving beyond entry-level keyboards.

The framework addresses a common challenge in the digital piano market: instruments with the same number of keys can provide substantially different playing experiences. An 88-key layout may indicate…

More Releases for Insurance

Renters Insurance Market Dazzling Worldwide with Major Giants Travelers Insuranc …

According to HTF Market Intelligence, the Global Renters Insurance market to witness a CAGR of xx% during the forecast period (2024-2030). The Latest research study released by HTF MI "Renters Insurance Market with 120+ pages of analysis on business Strategy taken up by key and emerging industry players and delivers know-how of the current market development, landscape, technologies, drivers, opportunities, market viewpoint, and status. Understanding the segments helps in identifying…

Renters Insurance Market to See Competition Rise | Travelers Insurance, Geico In …

HTF MI introduces new research on Renters Insurance covering the micro level of analysis by competitors and key business segments (2023-2029). The Renters Insurance explores a comprehensive study of various segments like opportunities, size, development, innovation, sales, and overall growth of major players. The research is carried out on primary and secondary statistics sources and it consists of both qualitative and quantitative detailing. Some of the major key players profiled…

Insurance Road Assistance Services Market Is Booming Worldwide | Travelers Insur …

Insurance Road Assistance Services Market: The extensive research on Insurance Road Assistance Services Market, by Qurate Research is a clear representation on all the essential factors that are expected to drive the market considerably. Thorough study on Insurance Road Assistance Services Market helps the buyers of the report, customers, the stakeholders, business owners, and stockholders to understand the market in detail. The updated research report comprises key information on the…

Equipment Breakdown Insurance Market Present Scenario And Growth Analysis Till 2 …

The global equipment breakdown market size is growing at a CAGR of 15% over the forecast years 2021-2028. Equipment breakdown insurance is a type of insurance cover that provides all risk cover and protection against any sudden and unforeseen physical loss or damage to the insured machines and equipment. Equipment breakdown insurance is usually triggered when certain machine or equipment undergoes failure leading to breakdown or any further loss. For…

Agriculture Crop Insurance Market Type (MPCI Insurance, Hail Insurance, Livestoc …

Agriculture Crop Insurance market worldwide Agriculture is an important contributor to any economy. The extensive use of crops for direct human consumption and industrial processes has resulted in increasing the pressure on the existing supply demand gap. Increasing need for food security is expected to augment the demand for insurance policies. The two major risks in agricultural sector are price risk, caused due to volatility in prices in the market…

Household Insurance Market By Key Players: Discount Insurance Home Insurance, On …

Household Insurance Industry Overview

The Household Insurance market research study relies upon a combination of primary as well as secondary research. It throws light on the key factors concerned with generating and limiting Household Insurance market growth. In addition, the current mergers and acquisition by key players in the market have been described at length. Additionally, the historical information and current growth of the market have been given in the scope of the research report. The latest trends, product portfolio, demographics, geographical segmentation, and regulatory framework of the Household Insurance market…